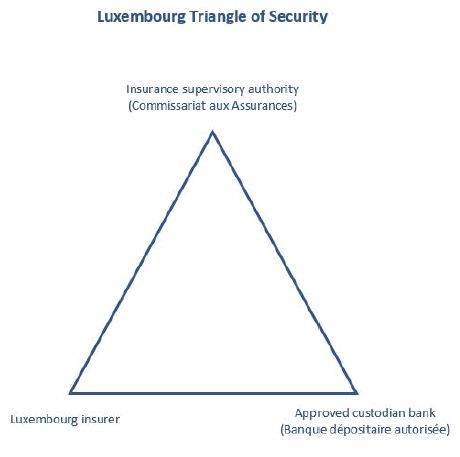

DEFINITION

Luxembourg has established a strict regulatory framework designed to provide the most beneficial protection for interests of individual investors using Luxembourg life insurance contract as an investment tool.

OBJECTIVE, PURPOSE

Luxembourg life insurance is an investment which combines the following within the framework of a long term investment approach:

- Various financial vehicles;

- A specific legal framework;

- A preferential tax framework.

When Luxembourg life insurance contract is used as an investment vehicle, it allows investors to combine financial and patrimonial objectives. In the past life insurance has gradually opened up to investment funds and thus to stock markets. Similarly, its legal framework is simple and legal means of ensuring transfer of constituted assets on good terms and sometimes with the benefit of advantageous fiscal measures are in place.

Investors may use the Luxembourg life insurance contract to invest their savings in one or more investment funds (collective investment fund, i.e. unit trust, or investment trust) in order to receive revenues. The Luxembourg life insurance contract may invest in several investment funds at a time and is therefore said to use a "unit-linked policy". In addition investors can access guaranteed rate monetary products.

ADVANTAGES OF INVESTING THROUGH INVESTMENT FUNDS

First, due to its pooling characteristics private insurance companies can invest in a vast number of investment funds thus allowing investors a dispersion of their capital and a limitation of risks through various styles of management, different strategies and different categories of assets. Such diversification provides greater protection from market risks.

Second, an investment fund comprises various stocks and shares offered by various issuers. This broad diversification of the underlying assets is an important additional factor which reduces investment risks. Such type of risk reduction is not possible within the management framework based on directly purchased shares or bonds.

Finally, investment funds are managed by financial management professionals who possess know-how, expertise and knowledge of financial markets, which is a necessity to secure good performance of investment funds.

ASSET TRANSFER TOOL

Under the terms of the Luxembourg life insurance contract the insurer promises the policyholder, in return for premium(s) payment , to pay to the beneficiary designated by such policyholder, a sum of money in the event of death of the insured, the value of which or the method of valorisation of which is established by a contract.

The parties to the life insurance contract are the policyholder, the insured and the beneficiary.

The insurance company bears the risk and undertakes to pay the sum due to the beneficiary in the event of death of the insured.

The payment on the basis of the contract is linked to an uncertain event, which is a hazard lying within the sphere of the insured.

ADVANTAGES OF A LIFE INSURANCE CONTRACT

In most European countries life insurance contracts are not transferred to heirs of policy holders. The capital paid to the beneficiary by the insurer in the event of death of the insured person is not included in its estate. The contract and assets therein cannot be seized by creditors of a policy holder. The legal heir can decline the estate while at the same time accepting the benefit of the contract.

Beneficiary clause, included in the Luxembourg life insurance contract, enables the insurer to determine the beneficiaries of the insurance contract in the event of his/ her death. He/she can give preference to an heir or a third party subject to the laws of the policyholder's country of residence can designate multiple or successive beneficiaries, can designate a non-profit organization and can also designate unborn children. Please note that the policy holder may amend this clause at any time.

FURTHER CHARACTERISTICS

Luxembourg life insurance contract is considered to be a unit-linked product with free investment. After the initial investment investors may increase their savings by making additional deposits.

Sums of deposited money and assets are generally available to investors at all times due to an option to partially or fully redeem the investments made under the latter and this is the case throughout the entire duration of the term of the contract.

The Luxembourg life insurance contract can be used as security/collateral when applying for a loan.

Very often such contracts can be subscribed by several policyholders and with several insured persons. Joint applications can therefore be made by a husband and wife in order to ensure the payment of a sum to a surviving spouse in the event of death of either.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.