"Stakeholders would be buoyed by the consistent release of detailed and targeted FPMs, as this shows FGN's willingness to respond to changes in the economy."

Introduction

The Federal Government of Nigeria (FGN) has approved and ordered the implementation of the 2019 Fiscal Policy Measure (2019 FPM), effective 1 July 2019. 2019 FPM replaces 2018 FPM, which had been in force since 27 July 2018. An in-depth analysis of the 2019 FPM reveals that FGN remains committed to its plan to encourage investment in industries deemed critical to its economic growth agenda; as well as discourage importation and consumption of certain items.

Highlights of 2019 FPM are summarized below:

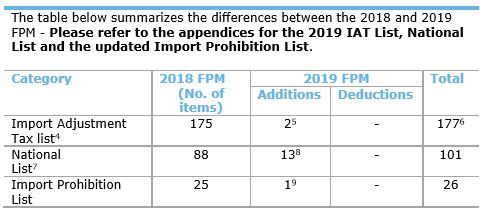

Addition of two items to the Import Adjustment Tax List

- Import tariff on sauces and preparations has been raised by 150% (i.e. from 20% in 2018 to 50% in 2019). This is a move that aims to curb importation of items like mayonnaise whose consumption has been on the increase;

- 75% increment in import tariff on anionic organic surface-active agents (i.e. from 20% in 2018 to 35% in 2019). This move is in line with the plan to localize production of items like Linear Alkyl Benzene Sulfonic acid, a synthetic surfactant used in the manufacture of detergents.

Application of duty rebates on certain tariff lines

- 50% reduction in import tariff on mixtures of odoriferous substances used in the perfume industry, (i.e. from 10% in 2018 to 5% in 2019);

- 71% tariff reduction on soap and organic surface active products and preparations, in other forms; 75% tariff reduction on mutilated rags and chemical inputs used in the production of agrochemicals1. A key highlight here is the elimination of tariffs on chemical inputs for production of agrochemicals;

- Elimination of import tariff on chemical inputs2 for the production of petrochemicals like hydraulic fluids, brake fluids, lubricating oils etc.;

- Elimination of import tariff on chemical inputs2 for the production of petrochemicals like hydraulic fluids, brake fluids, lubricating oils etc.;

- 50% reduction on hide powder, which is an attempt to reduce the cost of local leather production;

- 75% tariff reduction on non-wovens, a constituent material for producing baby diapers and sanitary towels. Importation of these products is said to cost the nation circa ₦4bn3 annually. Reducing the duties of non-wovens should help incentivize local manufacturers of baby diapers and sanitary towels – who have continued to expand their local manufacturing capabilities;

- Import tariff reduction of 50% on head-bands, linings, covers, hat foundations and frames; 75% reduction on worked vegetable or mineral carving material and articles thereof;

- 75% tariff reduction on collapsible tubular containers to incentivize manufacturers of glue, toothpaste and other tubular products;

Expansion of Import Prohibition List

- Mineral or chemical fertilizers containing two or three of the fertilizing elements nitrogen, phosphorus and potassium (NPK 15-15-15) falling under tariff codes from 3105.10.00.00 to 3105.90.00.00 have been added to the Import Prohibition List. This is a deliberate move to localize the production of fertilizers used in agricultural production. It is argued that local manufacturers can meet the local demand.

Conclusion

A critical review of the 2019 FPM reveals that FGN is responding directly to key sectors who have indicated a need for protection, a term that is increasingly becoming popular in today's macroeconomic discourse.

Specially impacted by this year's FPM is the petrochemical, textile, leather and agro-chemical industries, whose production costs should now become lower with the tariff reductions.

For consumers of mayonnaise, product prices are likely to increase significantly, as mayonnaise in most grocery stores are imported. Perhaps this opens the door for increased local production of the product, especially with mayonnaise consumption now on the increase.

Stakeholders would be buoyed by the consistent release of detailed and targeted FPMs, as this shows FGN's willingness to respond to the changes in the economy.

However, as we approach the end of the transitional period for the Common External Tariff for the Economic

Footnotes

1 Due to the propensity for abuse, these reductions would only be granted after traders have obtained approval from the FMF

2 Petroleum Oils containing PCBs, PCTs and PBBs (H.S Code 2710.91.00.00); Antiknock preparations, oxidation inhibitors, gum inhibitors and other additives for mineral oils - Containing petroleum oils or oils obtained from bituminous minerals Base Oil additives (H.S Code 3811.21.00.00)

Source: The Guardian

4 These are items that have been levied additional taxes in addition to the duties prescribed by the ECOWAS Common External Tariffs (CET)

5 CET reference: 2103.90.99.00; 3402.11.90.00

6 A detailed of review of the IAT List shows that only 177 items were affected

7 These are items that have been granted duty rebates relative to CET

8 Additions are: Petroleum oils containing PCBs, PCTs and PBBs, mixture of odoriferous substances of the kind used in perfumery, soap, paper and paper popular board of a kind used in writing: Medical paper, Nonwovens – Back sheet, mutilated rags, head gears, collapsible tubular containers, worked vegetable or mineral carving material and articles of these materials, Chemical inputs for the production of agro-chemicals, Medical grade polyethylene

9 CET Reference: Mineral or chemicals fertilizers containing two or three of the fertilizing elements nitrogen, phosphorus and potassium (NPK 15-15-15), excluding organic fertilizer HS Code 3105.10.00.00 - 3105.90.00.00

Community of West African States (ECOWAS) (in which case countries in the ECOWAS region can no longer unilaterally vary their tariffs), it would be interesting to know if FGN believes the Nigerian economy has properly adjusted to the incoming single tariff schedule.

If FGN (and perhaps other ECOWAS countries) is of the opinion that the Nigerian economy is not ready for an aligned ECOWAS schedule, we expect that the transitional period for alignment would be extended.

This notwithstanding, businesses must begin preparing for this eventuality. Businesses would do well to evaluate their current customs supply chains, to determine the impact of the 2019 FPM, as well as the transition to a single regional tariff schedule.

To read the full article click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.