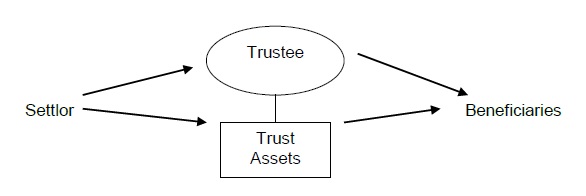

A trust is an arrangement whereby a person ("the Settlor") transfers assets to another person ("the Trustee") so that they can be used to benefit other persons ("the Beneficiaries"). Trusts established in certain low tax jurisdictions can provide a number of tax planning and other benefits.

A Settlor establishes a trust by appointing Trustees and transferring the legal ownership of assets to those Trustees. The Trustees are responsible for managing the assets for the benefit of the Beneficiaries. The details of this arrangement are recorded in a formal document ("the Trust Deed").

The Settlor may give the Trustees specific instructions as to how to deal with and distribute the trust assets (a "fixed" trust). Alternatively, the Settlor may give the Trustees discretion as to how to share the assets between the Beneficiaries and when to make any distributions (a "discretionary" trust). If the trust is discretionary, the Settlor cannot insist that the Trustees act in certain way. However, the Settlor may give the Trustees guidance as to how he would wish them to act in a "Letter of Wishes". The Trustees should always consider the terms of the Letter of Wishes in making any decision in relation to the trust or its assets.

Although the trust assets are legally owned by the Trustees, trust assets are kept completely separate from any other property owned by the Trustees. The Trustees have a legal obligation to manage the trust assets in accordance with the Trust Deed and to ensure that the rights of the Beneficiaries are protected.

Trust Solutions and Opportunities

- Tax planning

Tax advantages can arise from the fact that once a trust is established, neither the Settlor nor the Beneficiaries are the legal owners of the trust assets. Income and capital gains in respect of the trust assets belong to the Trustees. A trust based in a low tax jurisdiction can earn income and capital gains free of taxation in that location. Income and gains may be deemed to accrue to Settlors and Beneficiaries dependent on the individual tax position of the Settlors and Beneficiaries.

- Protection of family property

A trust can provide an effective arrangement for the orderly distribution of assets to family members or other Beneficiaries. An individual can ensure that dependants are provided for in the future by establishing an appropriate trust. Family property which is held in trust is not controlled by individual family members and cannot therefore be sold or "squandered" by them. In addition, as the Trustees own the property, it is protected from "forced heirship" legislation and claims from any creditors of the Settlor or Beneficiaries.

- Centralisation of assets

A diverse portfolio of world-wide assets can be managed centrally through a suitable trust arrangement. This can provide significant benefits for individuals who are internationally mobile. In addition, individuals who own a number of companies in different jurisdictions could benefit from establishing a trust as a tax-free holding structure for these companies.

- Employee benefits

Trusts can be used as a tax efficient vehicle for employee share schemes and employee profit-sharing arrangements.

- Anonymity

In many jurisdictions, there is no requirement to register the creation of a trust. Details of the Settlor, Beneficiaries and the terms of the trust are not therefore publicly available. Where confidentiality is important a trust provides substantial advantages over a company.

Types of Trusts

Trust structures are very flexible and can be tailored to meet the precise requirements of the Settlor. Trusts may be either "fixed" or "discretionary".

- Fixed trust

With a fixed trust, the Settlor will identify the Beneficiaries and specify the way in which the assets are to be distributed in the trust deed. A fixed trust is often a suitable arrangement to enable a widow to receive income from family property during her lifetime whilst ensuring that the property will be distributed on her death to children or other family members.

- Discretionary trust

Typically, a discretionary trust will define a class of Beneficiaries but give the Trustees discretion over the amount and timing of payments to the Beneficiaries. The Settlor may give the Trustees guidance as to how to exercise their discretion in a letter of wishes.

This type of trust may provide tax planning advantages as the Beneficiaries have no right to receive income or assets as the Trustees have complete discretion over any distributions. All income and gains therefore accrue to the trust. Furthermore, assets held by a discretionary trust are protected from any "forced heirship" legislation or claims from the creditor of the Beneficiaries.

A discretionary trust can also be a flexible way of enabling a Settlor to make financial provision for dependants (typically children or minors). For example, the Trustees may pay income for the benefit of children who have no right to receive the trust assets until they reach a specified age.

Where should a trust be established?

Verfides can advise on the establishment of trusts in the UK, New Zealand, Hong Kong, Isle of Man and other jurisdictions. The particular advantages of each jurisdiction are summarised below. Further details are available on request.

- UK Trusts

The UK can provide an ideal and respected location for an "onshore" trust which also has the tax benefits normally associated with tax-haven locations. English law offers legal certainty and protection of the English legal system and, of course, trusts are well known to and recognised by the English judicial system. A UK trust should be considered by non-UK residents who wish to establish a trust comprising primarily assets situated outside the UK, although under certain circumstances there are no tax liabilities in respect of even UK-source income. A separate fact sheet is available with further information.

- New Zealand Trusts

For Settlors in Asia, Australasia or even Europe who are seeking an "onshore" trust with the benefits normally associated with tax haven locations, the New Zealand trust may be the ideal solution. Provided the Settlor, Beneficiaries and Assets have no connection with New Zealand, the New Zealand resident trustee will not be taxed on the trustfs income or capital gains. The New Zealand courts are experienced in dealing with trust matters. A New Zealand trust offers confidentiality and anonymity as there is no requirement to register a trust or disclose the details of the Settlor or Beneficiaries to any regulatory or other authority.

- Hong Kong Trusts

A Hong Kong trust offers the same "onshore" benefits as a New Zealand trust with no taxation providing no income arises in Hong Kong. They are particularly useful for settlors in Asia. A Hong Kong trust offers confidentiality and anonymity.

- Isle of Man Trusts

The Isle of Man ("IOM") provides an excellent tax-free jurisdiction for the formation and management of trusts. IOM trust legislation is well developed and the IOM is a well regulated international financial centre with "AAA" stability rating. IOM trusts can accumulate income and capital gains free of tax provided the Beneficiaries are outside the IOM.

Summary

Establishing a trust can provide significant taxation and other benefits for high net worth individuals. In addition, corporate clients can obtain benefits from using a trust structure to hold assets or benefit employees.

Trusts are highly flexible structures which can be tailored to the precise requirements of the client. Although legal title to the assets is transferred to the Trustees, clients can be confident that those assets will be safeguarded and will be managed in accordance with their intentions.