Valuing a franchise system, or "franchisor", is in many ways very similar to the valuation of any other type of business; it is a function of the forecasted levels of cash flows that the business will generate, and the risk associated with those cash flows. Yet there are some particular factors that make valuing franchisors very tricky. This brief article touches on some of them.

Franchisors – Who are they?

The first point we need to clarify is what we mean when we speak of "franchisors". Broadly speaking, a franchisor is a business that earns its income by granting the privilege to one or more franchisees to do business and offers some form of ongoing assistance and oversight in return for ongoing monetary consideration.

Franchisors operate in a variety of industries. The largest industry sector is in the food services; these businesses made up around 40% of the membership in the Canadian Franchise Association in 2017.1 Tim Hortons', McDonalds, Swiss Chalet – you get the picture. But there are many other types of franchisors in the retail and service industries. Most hotel chains are franchised, as are most automobile dealerships and the guys who promise to remove junk from your house at all hours of the day. These different industries obviously have different valuation characteristics.

There are also different types of business structures for franchisors. Thus:

- Some franchisors are what one might call "pure plays" (i.e. their income derives almost solely from the sale of franchises and the receipt of royalties). On example of this type of franchisor is Dine Brands Global Inc., the franchisor for the "Applebee's" and "IHOP".

- Other franchisors have structured their publicly traded shares as "royalty income funds", which receive a portion of the royalties from the franchisees, while many of the expenses of operating the system are incurred in a separate company. Examples include Keg Royalties Income Fund and Boston Pizza Royalties Income Fund.

- Still other franchisor companies are hybrids, with a significant chunk of their revenue (though not necessarily their profit) coming from corporate-owned stores or from the sale of inventory to franchisees.

In a similar vein, while some franchisors hold a lot of real estate (e.g. McDonalds, Canadian Tire (until recently)), others do not.

What this means is that it is very important to understand the business of the franchisor you are valuing. It may hold several different sources of value: a stream of royalties, one or more actual operating businesses, and real estate. In order to gain a true grasp of the value of the business, you need to disaggregate and understand the different sources of value.

Valuation Approaches

There are three main approaches to valuing a business or asset: the income approach, market approach and asset approach. Of these, only the first two have any real relevance to valuing franchisors.2 Stated very briefly:

- Under the income approach, the business valuator quantifies the present value of future cash flows associated with share ownership. The calculated future cash flows are discounted at a rate of return appropriate for the risks associated with those cash flows.

- Under the market approach, the business valuator determines the fair market value of the company based on comparable public companies and/or transactions involving comparable companies.

Income Approach

The three main drivers of value under the income approach are a) the current level of cash flows, b) projected growth and associated reinvestment, and c) risk. Let's take a look at each one.

Cash Flows

For "pure play" franchisors, this issue can be relatively simple. Operating margins for franchisors are generally high; there is also typically fairly little in the way of capital expenditures. Furthermore, franchisors as a whole tend to carry fairly little debt relative to their equity values (unless they have made acquisitions). They also tend to carry fairly low working capital balances. All of this means that in general, after-tax net income can serve as a reasonable proxy for cash flows.

For franchisors who also earn revenue from other sources (e.g. sale of inventory, operation of corporate stores), the analysis can become more complicated, and it will be necessary to consider things like capital expenditures to upgrade stores, changes in minimum wage legislation and commodity prices, and all of the other complicating factors that go into valuations of businesses in other industries.

Growth

For franchisors, growth can come from two main sources: a) growth in the number of franchisees and b) growth in income per franchisee. In addition, growth can also come from acquisitions.

Growth in the number of franchisees can lead to multiple sources of revenue growth. In additional to new royalty streams, franchisors also typically charge an initial franchise fee that is payable upfront; this can often be substantial and can be a significant source of revenue. Some franchisors also serve as suppliers to their franchisees and earn income from markups on the supplies they sell. Franchisors can also assist their new franchisees manage the build-out of their locations, charging a management fee.

In many businesses, growth is accompanied by significant cash outflows as companies are required to carry additional inventory, carry more accounts receivable and build larger facilities. Franchisors do not have to deal with these issues to nearly the same degree.

That said, franchisors face other issues when it comes to growth. There is a cost associated with finding new franchisees in new territories, and for that reason many franchisors outsource that function to master franchisees. The master franchisee will assist the franchisor in developing franchisees in a given territory, but only in exchange for a significant cut of the new franchisees' franchise fees and royalties.

Moreover, growth within a territory can result in friction with existing franchisees. The addition of a new location within proximity to a franchisee can lead to great overall system sales (and thus more royalties and other payments to the franchisor); but this comes at a cost to the existing franchisee, who in some sense becomes a competitor to the newcomer and will likely see a reduction in income. If the reduction is too great, the existing franchisee may go out of business.

Risk

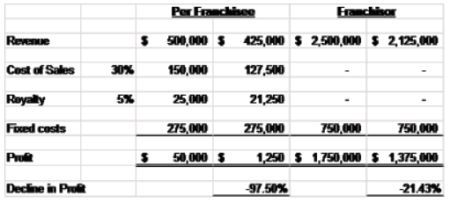

Established franchisors are relatively immune from macro-level trends. To understand why this is the case, consider the difference between a franchisor and a franchisee of a restaurant chain. Assume that each of a chain's 100 franchisees earns an average of $500,000 in revenue per year, that the costs of sales equals 30% of sales, the royalty is 5%, and fixed costs (labour, rent, utilities) equals 55% of sales, giving it a profit margin of 10%, or $50,000 per year. The franchisor makes $25,000 in royalties (5% of $500,000) per franchisee, and $2.5M overall from the 100 franchisees.

If the market shifts and the franchisees sales decline by 15%, the franchisor's profit from the restaurant will also drop by around 21%;3 however, the franchisees' profits will drop by almost 98%.

The fact that a franchisor's profits are less subject to large swings based on small changes in revenue is an advantage and lowers the riskiness of an investment in a franchisor.

On the other hand, there are also risk factors that are significantly higher for franchisors than for other businesses. Many of these are legal in nature. Franchisors can be susceptible to class actions of various types, although the success rate for these so far in Canada has been poor.4Franchisors are also subject to a rigorous disclosure regime in many Canadian provinces; the failure to provide a proper Franchise Disclosure Document ("FDD") can be severe, with franchisees potentially eligible to rescind their agreements and recover all of their costs and losses within the first two years of signing the franchise agreement. In my experience dealing with quantifying such claims, the average bill to a franchisor is somewhere in the $300,000 to $500,000 range, plus legal costs.

Market Approach

As we discussed above, franchise systems derive their value from many different sources. That can make the market approach difficult to apply; it is difficult to speak of a standard valuation multiple based on revenue in the franchising industry. Thus:

While royalty income funds (e.g. Boston Pizza Royalties Income Fund, Keg Royalties Income Fund) have tended to trade at multiples of over 10 times revenue, other hybrid franchisor public companies (e.g. Imvescor Restaurant Group Inc.) have traded at around five times revenue. Multiples of revenue are therefore generally not a good approach to use.

As described above, franchisors who derive most of their revenue from franchising (as opposed to corporate stores) generally are less subject to volatile changes in their profits. Royalty income funds are even less volatile, since their costs are minimal.

Differences in growth rates can also affect multipliers; firms that are expected to grow rapidly will attract higher multipliers.

In summary, the market approach is a difficult approach to apply for franchisors.

Conclusion

Conceptually, valuing a franchise system is in many ways no different than valuing any other business: it requires an understanding of the industry and the business, and the assessment of cash flows and risk. Executing on these concepts can pose a challenge.

Footnotes

1. 2018 CFA Accomplishment Report

2. The asset approach is generally one that is more applicable to companies whose main value derives from their individual asset holdings (e.g. real estate holding companies).

3. I have assumed a level of fixed costs for the franchisor similar to Dine Equity, a "pure play" franchisor.

4. Several notable examples include:

- Fairview Donut Inc. v. The TDL Group Corp., 2012 ONSC 1252 (brought by Tim Horton's franchisees over the introduction of a breakfast menu). Certification denied.

- 1250264 Ontario Inc. v. Pet Valu Canada Inc., 2016 ONCA 24 (brought by Pet Valu franchisees over the alleged failure of the franchisor to share volume rebates with franchisees). Certification denied.

- 2038724 Ontario Ltd. v. Quizno's Canada Restaurant Corporation, 2014 ONSC 5812 (brought by Quizno's franchisees over allegations of price fixing). Certification granted, but later settled for a small amount.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.