The single tax measure introduced in the 2018 fall economic update was accelerated capital cost allowance for eligible property.

What is capital cost allowance?

Depreciable property is not allowed to be deducted as a current expense. Instead, the capital cost of the depreciable property is added to a capital cost allowance class and deducted over several years based on the CCA rate of that class. This annual deduction is called capital cost allowance (CCA for short) and is analogous to depreciation.

The CCA allowed in the first year that a taxpayer's capital property is available for use is generally limited to half the amount that would otherwise be available in respect of that property (the "half-year rule"). This rule applies to the net addition to the class for the year (i.e., the amount by which acquisitions exceed dispositions).

Accelerated capital cost allowance

The accelerated capital cost allowance is available in three separate categories:

- Accelerated Investment Incentive (increase in first year allowance),

- Manufacturing and processing machinery and equipment (full expensing), and

- Clean energy equipment (full expensing)

Accelerated Investment Incentive (increase in first year allowance)

The Accelerated Investment Incentive will provide an enhanced first-year allowance for capital property that is subject to the CCA rules. This first-year enhanced allowance does not include capital property included in categories 2 or 3. The first-year enhanced allowance is also subject to legislation contained in the Income Tax Act and Income Tax Regulations that will restrict the CCA deduction for specific situations such as: limited partners, specified leasing properties, specified energy properties and rental properties.

The enhanced allowance is equal to the following:

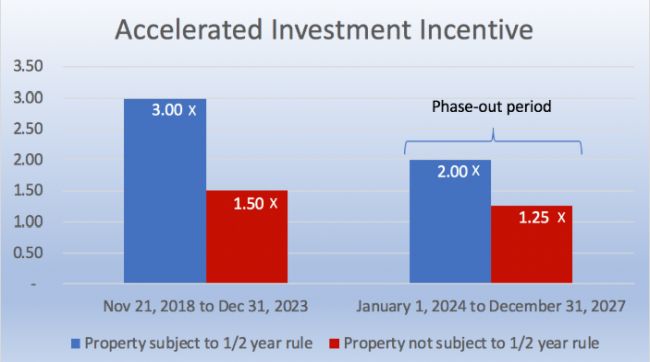

- Property currently subject to the half-year rule will qualify for an enhanced CCA equal to three times the normal first-year allowance,

- Property not currently subject to the half-year rule will qualify for an enhanced CCA equal to one and a half times the normal first year allowance.

Here is an example provided by Department of Finance:

Prior to the introduction of the Accelerated Investment Incentive, a property in Class 8, which has a prescribed rate of 20 per cent, would be eligible for CCA of 10 per cent of the cost of the property in the year it becomes available for use, due to the half-year rule. Under the Accelerated Investment Incentive, the taxpayer will be eligible for CCA of 30 per cent of the cost of the property—that is one-and-a-half times the CCA calculated using the prescribed rate of 20 per cent or three times the 10-per-cent CCA that could otherwise be claimed in the first year.

The total amount of depreciation (CCA) that can be taken over the useful life of the eligible property does not change with the accelerated investment incentive. The only change is the timing of the CCA, resulting in a higher amount of CCA taken in the first-year, reducing the overall CCA available to be taken in subsequent years.

Application and phase-out

The Accelerated Investment Incentive is available for a limited time only. It applies to eligible property that is acquired after November 20, 2018 and that becomes available for use before 2028, subject to a phase-out for property that becomes available for use after 2023.

The phase-out period for acquisitions that become available for use after 2023 but before 2028 results in a reduced enhanced first-year allowance as follows (see chart below):

- Property currently subject to the half-year rule will qualify for an enhanced CCA equal to two times the normal first-year allowance,

- Property not currently subject to the half-year rule will qualify for an enhanced CCA equal to one and a quarter times the normal first year allowance

Manufacturing and processing machinery and equipment (full expensing)

Machinery and equipment used in Canada primarily in the manufacturing or processing of goods for sale or lease already have a temporary accelerated CCA rate of 50 per cent under Class 53. This temporary provision applies to acquisitions after 2015 and put into use before 2026. Without this temporary measure, the machinery and equipment would be included in Class 43 and qualify for a CCA rate of 30 per cent.

This new measure allows the same machinery and equipment to have an enhanced first-year allowance equal to 100 per cent (full deduction in year available for use). This enhanced first-year allowance applies to property acquired after November 20, 2018 and becomes available for use before 2028.

Clean energy equipment (full expensing)

Specified clean energy equipment already has two temporary accelerated CCA rates. 30 per cent under Class 43.1 for acquisitions after February 21, 1994 and 50 per cent under class 43.2 for acquisitions after February 22, 2005 and before 2025. Many of these assets would normally be depreciated at lower rates of 4, 8 or 20 per cent, but can be depreciated at either 30 or 50 per cent if they qualify as clean energy equipment defined in the Income Tax Regulations.

This new measure allows the same clean energy equipment to have an enhanced first-year allowance equal to 100 per cent (full deduction in year available for use). This enhanced first-year allowance applies to property acquired after November 20, 2018 and becomes available for use before 2028.

These enhanced allowances for manufacturing and processing and clean energy will be phased-out after 2023 with full elimination after 2027 (see chart below):

Certain additional restrictions will be placed on property that is eligible for the Accelerated Investment Incentive. Property that has been used (or acquired for use) for any purpose before it is acquired by the taxpayer will be eligible for the Accelerated Investment Incentive only if both of the following conditions are met:

- neither the taxpayer nor a non-arm's-length person previously owned the property; and

- the property has not been transferred to the taxpayer on a tax-deferred "rollover" basis.

As 2018 is quickly narrowing to a close, it would be prudent to review your capital asset acquisition plan with the possible intention of accelerating the purchase of eligible assets and gain access to additional current deductions through enhanced CCA. Remember that the acquired property must be available for use before the end of the current fiscal period in order to gain access to CCA in the same period.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.