Retractable or Mandatorily Redeemable Shares Issued in a Tax Planning Arrangement

In December 2018, the Accounting Standards Board concluded its project to re-examine the special treatment1 for preferred shares issued in a tax planning arrangement provided by Section 3856, Financial Instruments, by issuing final amendments to paragraph 3856.23. The amendments apply to annual financial statements relating to fiscal years beginning on or after January 1, 2020. Earlier application is permitted.

Prior to the effective date of the amendments, an enterprise issuing preferred shares in a specified tax planning arrangement2 presents the shares at par, stated or assigned value as a separate line item in the equity section of the balance sheet, with a suitable description indicating that the preferred shares are redeemable at the option of the holder. These preferred shares remain in equity until such a time that redemption is demanded. Upon redemption being demanded, these preferred shares are reclassified to liabilities and measured at the redemption amount with any adjustment recognized in retained earnings.

What are the main changes?

The amendments to paragraph 3856.23 continue to provide, if certain criteria are met, an exception to financial liability classification for Retractable or Mandatorily Redeemable Shares ("ROMRS") issued in a tax planning arrangement. Moreover, the amendments to paragraph 3856.23 no longer make reference to "preferred" shares, nor are the specific tax planning arrangements defined. The amendments specify that an enterprise that issues ROMRS in a tax planning arrangement may choose to present those shares at par, stated or assigned value as a separate line item in the equity section of the balance sheet only when all three of the following conditions are met:

- Control3 of the enterprise issuing the ROMRS in a tax planning arrangement is retained by the shareholder receiving the shares in the arrangement;

- In the arrangement, either:

- 1 No consideration is received by the enterprise issuing the ROMRS; or

- 2 Only shares of the enterprise issuing the ROMRS are exchanged; and

- No other written or oral arrangement exists (e.g., a redemption schedule), that gives the holder of the shares the contractual right to require the enterprise to redeem the shares on a fixed or determinable date or within a fixed or determinable period.

If any of the above conditions are not met, the shares are required to be classified as a financial liability, separately presented on the balance sheet and measured at the redemption amount.

As indicated above, ROMRS issued in a tax planning arrangement that meet all three of the above conditions may be presented at par, stated or assigned value. Even when all three criteria above are met, an enterprise may choose to present the ROMRS issued in a tax planning arrangement as a financial liability.

Reclassification of ROMRS issued in a tax planning arrangement classified as equity would be required if an event or transaction occurs that may indicate that any of the three criteria above are no longer met. ROMRS issued in a tax planning arrangement that are initially classified as a liability are not subsequently reclassified.

What are the potential impacts of the amendments?

For some enterprises, the amendments to paragraph 3856.23 will be negligible or limited to disclosure (e.g., a description of the arrangement that gave rise to the shares). For others, there may be a profound impact on the financial statements.

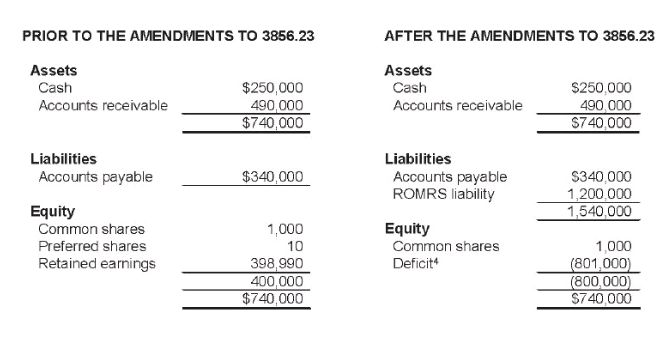

To demonstrate the impact on an enterprise's balance sheet of the amendments, consider ROMRS issued in a tax planning arrangement that do not meet the retention of control criteria in amended paragraph 3856.23. Assume that the stated amount of the shares is $10 and that they have a redemption amount of $1,200,000.

As a result of the amendments to paragraph 3856.23, the enterprise's financial position differs as the ROMRS would now be required to be measured at their redemption amount (i.e., $1,200,000) and presented separately on the balance sheet. Consequently, the financial ratios of the enterprise are impacted including, but not limited to, the enterprise's current ratio and debt-to-equity ratio. Moreover, any dividends declared on the ROMRS would now be presented as an interest expense in the income statement in accordance with paragraph 3856.15 and not directly in equity. This may impact bonus calculations and profit-sharing arrangements that are based on net income.

The Take-away?

It is important for an enterprise that has previously issued preferred shares in a tax planning arrangement or intends to issue ROMRS in a tax planning arrangement to fully understand the impact of the amendments to paragraph 3856.23. While there are certain transitional provisions available to enterprises that have previously issued preferred shares in a tax planning arrangement, the amendments to paragraph 3856.23 could still impact financial ratios or covenants that are relevant to the users of the financial statements. Financial statement preparers should proactively identify contracts and other relevant agreements that may be impacted by the amendments to paragraph 3856.23 to ensure that there are no unintended consequences as a result of these changes. If there is a significant impact (e.g., anticipated covenant breaches) of the amendments to paragraph 3856.23, financial statement preparers should work diligently with users to mitigate the impact (e.g., amend the covenants).

Footnotes

1 To permit equity classification despite meeting the definition of a liability as set out in Financial Statement Concepts, Section 1000.

2 Under Sections 51, 85, 85.1, 86, 87 or 88 of the Income Tax Act (Canada).

3 As set out in Subsidiaries, Section 1591.

4 For purposes of this example the adjustment has been recorded in deficit. Enterprises have an option to present the adjustment in a separate component of equity.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.