Singles' Day, or Double 11, will soon celebrate its 15th year as China's marquee shopping event. Double 11 2023 is especially crucial—with consumption metrics a leading indicator of Chinese economic rebound as the country faces post-pandemic economic uncertainty.

In recent years, shoppers showed less enthusiasm to spend on Singles' Day, evidenced by a declining year-over-year growth rate in our annual AlixPartners Singles' Day Survey. 12% YoY growth from 2020 to 2021 slowed to 5% from 2021 to 2022, largely driven by the fiscal climate and once-hot marketing tactics losing momentum. So, how will consumers respond in times of economic constraint? What purchasing behaviors will emerge amongst this year's most active customer groups? And what can businesses do to make the very most of this global retail phenomenon?

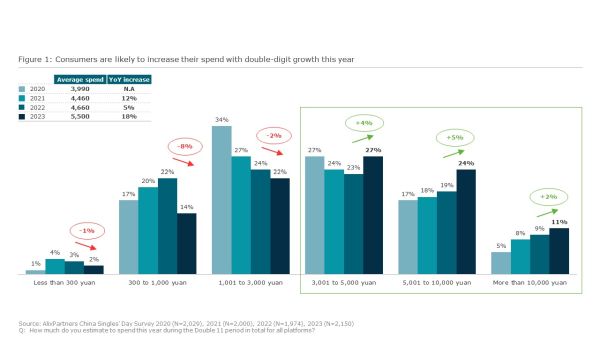

Total spend will exceed that of 2022

According to our 2023 survey, consumer sentiment is picking back up and, shoppers will once again turn out in large numbers to take advantage of Double 11's famous discounts. Results indicate an 18% increase in total spend compared to that of 2022, nearly four times the uplift seen between 2021 and 2022. 46% of respondents also say they'll increase their spending this year compared to last, while only 7% plan to decrease. 62% say they'll spend at least 3,000 yuan this year, up 11 percentage points from 2022.

Shoppers to rally around "Rational consumption"

Consumers taking part in Singles' Day this year will display traits reflective of "rational consumption"—where shoppers are prompted to carefully research across retailers and channels to identify the best value for money before making a purchase decision.

This year our data indicates that shoppers plan to use increased

product knowledge to make thoughtful, value-based buys. Promotional

efforts such as livestreaming will likely continue to influence

consumers to make impulsive or emotionally driven purchases, but

this may be diminishing, reflected by only 22% calling

livestreaming out as a key reason for purchase, versus 32% in

2021.

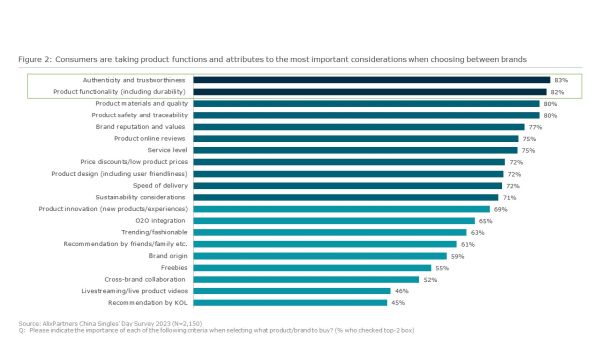

For retailers, emphasizing product functionality, quality,

and safety—along with overall brand trustworthiness,

authenticity, and reputation—will best connect with the

"rational shopper". Carefully targeting

marketing tactics at specific audience segments, through the right

channels and with the right content, will yield the greatest

returns.

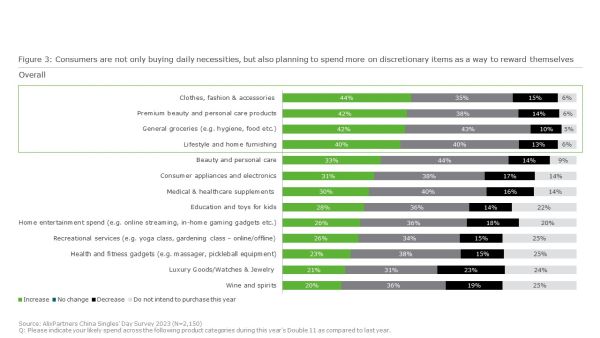

Discretionary spend remains prominent, beyond spend on daily necessities

Luxury goods and aspirational items like watches, jewelry, wine, and spirits see the largest decrease in purchase intent this year compared to last. Meanwhile, consumers across age groups plan to increase spend on practical, everyday items; categories such as clothing and accessories, beauty and personal care products, lifestyle and home furnishings, and food and hygiene displayed the highest increases in purchase intent for 2023. Consumers are still willing to reward themselves with discretionary purchases, too, but these will be prudent as opposed to extravagant or indulgent gifts.

Keeping consumption closer to home

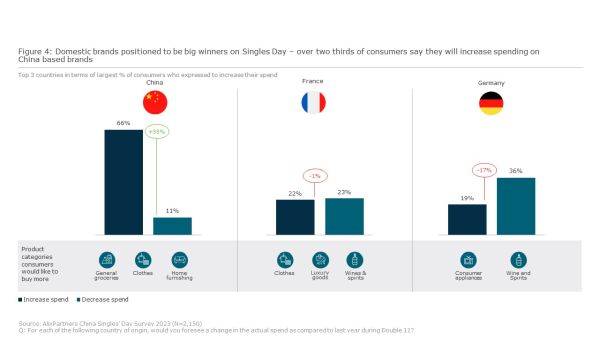

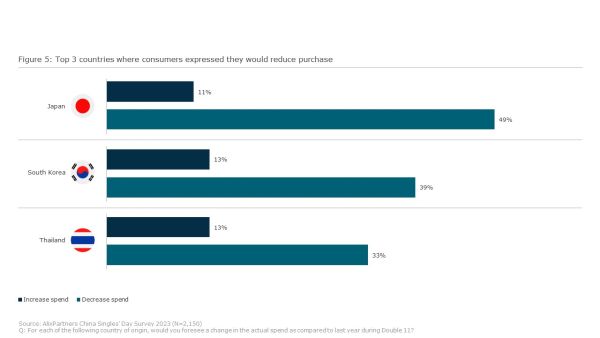

Shoppers want to buy local this Double 11, with 66% planning to increase spend on Chinese brands, as indicated in Figure 4 below. We collected this data across 13 countries; products originating from the other 12 saw a net decrease in purchase intent. In previous years, our survey indicated that rising levels of national loyalty drove domestic purchases. This year, we attribute the increase to a growing perception that Chinese brands are catching foreign brands in terms of product quality and safety. A more knowledgeable consumer base is actively looking to lower-cost, viable alternatives to foreign brands, and local options are closing the gap when it comes to "premium" associations.

For example, Chinese clothing brands now have an emerging "coolness" factor that has younger consumers choosing local fashion at the expense of foreign labels. Current trending examples those boasting outstanding craftsmanship and scrupulous attention to detail, while others factor sustainability into every design and production decision, from sourcing local materials and fabrics to minimizing waste from production.

With that said, consumers are more inclined to choose foreign brands over mass brands within certain product categories. This is particularly true of French beauty products, fashion, wine, spirits, and luxury goods, along with German consumer appliances and electronics. Given the reputational rise of Chinese products, it is no longer enough to simply be a foreign brand in a particular category. Each will need to display its key product advantages to best attract consumers, offering differentiators that match price premiums. For example, foreign cosmetics brands are beginning to hire vertical-specific expert Key Opinion Leaders (KOLs) in addition to "mega KOLs" to engage consumers differently through tailored, targeted content messaging instead of purely brand building.

A growing silver economy boosts the impact of its shoppers

China is now home to the largest population of shoppers over 60 in the world. This segment is China's fastest-growing generational group and is already digitally enabled—making this a prime segment for retailers and platforms other than focus on most marketing spend on younger and middle-aged consumers. As this demographic may fuel the future growth of Double 11, retailers must tap into the silver economy's shopping preferences.

We see two broad types of buying motives for silver economy consumers: those who shop on Singles' Day searching for bargains, and those spending on items to improve their quality of life and make their later years more enjoyable.

For the bargain hunters, general groceries are the primary product category—only 1% of surveyed consumers older than 56 do not intend to purchase groceries this Singles' Day. Those looking to improve quality of life are likely to shop for premium beauty products, as well as medical and healthcare supplements.

We see the latter segment growing over time, as a rising Chinese middle class will lead to a larger percentage of older shoppers with disposable income. Knowing your audience and which groups are worth targeting for a given product or campaign will be key.

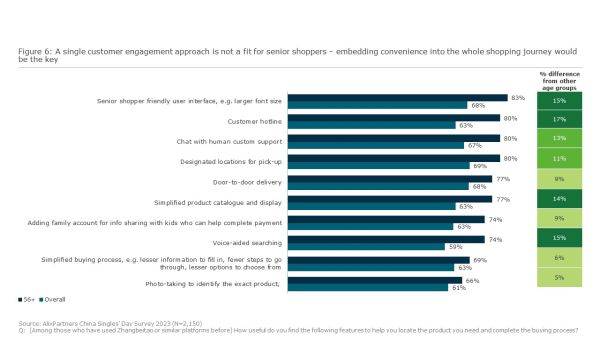

To build connection and loyalty, retailers will need to cater offerings to a different life stage. The ease of the purchase process matters greatly to senior shoppers, to offset potential vision and mobility limitations. Certain e-commerce companies have rolled out customized platforms with larger font sizes and simplified product information as a result, such as Taobao with Zhangbeitao. Additional elderly-oriented functions to improve convenience—such as voice-aided search or a customer service hotline—will further drive adoption among seniors. These apps also must implement strong data security practices around payments and ads to protect the more vulnerable.

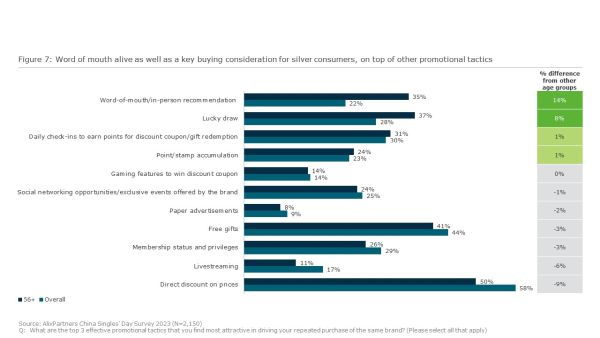

Nearly three-quarters of senior shoppers are heavily influenced by family and peer recommendations when choosing which products and brands to buy. Looking at promotional tactics, while younger demographics clearly favor direct discounts and gifts, senior shoppers are attracted to a wider variety. They display a higher preference for more traditional marketing methods such as word-of-mouth and in-person recommendation (14 percentage points above the overall population) and lucky draw (8 percentage points above). This should act as a reminder to brands to carefully tailor their promotions to more senior consumers, in light of these differences.

Based on the above characteristics, we believe retailers can best grow share with this influential segment by:

- Tailoring product design to older shoppers during R&D, to establish age-centric considerations from the start.

- Embedding convenience into the end-to-end shopping journey—from initial product search and product descriptions to delivery and aftersales services.

- Adapting marketing tactics and messaging to older shoppers vs. younger audiences, with a focus on generating strong word-of-mouth.

- Building a brand image that effectively inspires and influences an aging Chinese population, to ensure your current consumer base remains loyal with time.

Conclusion

Chinese consumers are not letting a gloomy economic outlook

affect their participation in Singles' Day 2023. It continues

to grow as the world's largest online shopping festival, but

for retailers to make the most of the opportunity this year, they

must adjust to rapidly evolving market dynamics and navigate the

competitive landscape to meet consumer needs.

Rational consumption habits will lead consumers to make more

knowledgeable, discerning choices to ensure the greatest value. The

product is the main factor in their decision—retailers must

emphasize functionality, quality, and advantages over rival

options. This goes for both foreign and domestic brands, which now

sit on a level playing field. To win, brands can either compete on

price or compete on product differentiation. Highlighting your key

value proposition and benefits in marketing will be key to entice

consumers—quality of ingredients or a responsive aftersales

service, for example.

As the Chinese population structurally shifts, the rising silver

economy has become too large to ignore. Retailers must embrace

senior shoppers and their unique preferences to meet a different

set of needs and behaviors. A curated strategy targeted at this

segment (especially to those soon to reach this segment too)

through their preferred channels and promotional tactics—with

focus on ease of the shopping journey and product use—will

set retailers up to grow their share of this crucial market.

Nail the above, and you will outshine the competition during

Singles' Day 2023 and beyond.

For more in-depth analysis and recommendations, make sure to read our comprehensive 2023 Singles' Day Report releasing October 31.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.