China's Special Customs Supervision Zones (SCSZs) are the best-suited locations for foreign investors engaged in export-oriented trade and production.

China Briefing introduces the different types of SCSZs and analyzes their functions, preferential policies, and the broader policy trends affecting them.

Special Customs Supervision Zones (SCSZs) are a type of economic development zone in China, which were first set up in the 1990s as the country opened up to foreign investment and bonded processing trade.

Bonded processing trade is the business activity of importing raw and auxiliary materials and re-exporting the finished products after processing – the materials and finished products can be exempted from import-export duties and taxes when taking place in specially regulated areas.

Upon approval by the State Council, China's cabinet, SCSZs are set up under the supervision of customs authorities.

They are usually surrounded by an iron mesh enclosure, making them segregated areas. Thus, while the SCSZ is in the territory of China, enterprises in the SCSZs are treated as "overseas".

Goods entering SCSZs from abroad are not categorized as imports and enjoy preferential bonded policies. Similarly, goods from domestic out-zone areas entering some SCSZs may enjoy export rebates.

SCSZs, therefore, tend to be the best-suited locations for foreign investors engaged in export-oriented trade and production in China. In fact, while SCSZs occupy only 1/20,000th of China's land, they generated around one-sixth of the country's total foreign trade in 2018.

In this article, we introduce the different types of SCSZs in China and highlight the preferential policies and functions of Comprehensive Bonded Zones (CBZs), which could become the dominant type of SCSZ in the future due to current policy trends.

Types of SCSZs in China

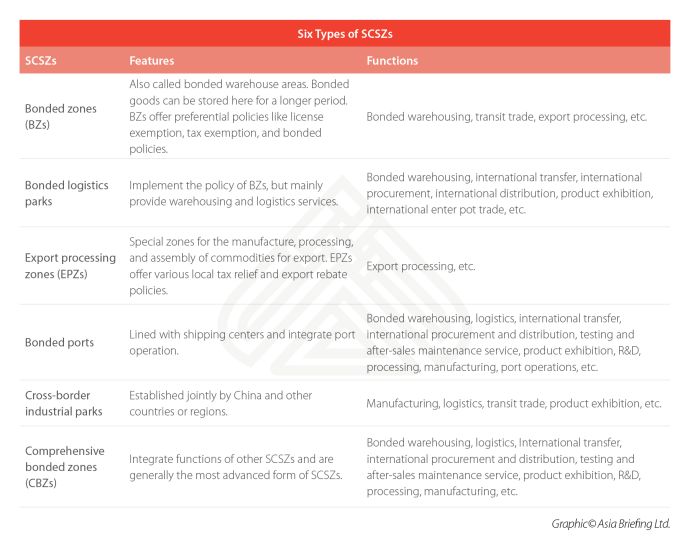

Currently, there are six types of SCSZs existing in China – Bonded Zones (BZs), Bonded Logistics Parks, Bonded Ports, Export Processing Zones (EPZs), Cross-Border Industrial Parks, and Comprehensive Bonded Zones (CBZs).

The respective types of SCSZs have different but partially overlapping functions.

But, as proposed in the Plan to Speed Up the Integration and Optimization of SCSZs Scheme issued in 2015, all existing SCSZs will be integrated into two types in the future: Bonded Zones (BZs) and Comprehensive Bonded Zones (CBZs). Further, except for some BZs, many SCSZs will transition or are currently transitioning into becoming CBZs.

In Shanghai, for example, there are 10 SCSZs that have received approval from the State Council on their integration and optimization plans to become CBZs.

In May 2019, the Caohejing and Fengxian EPZs were just upgraded to CBZs.

The reason why CBZs are so favored is because they integrate the functions of other SCSZs and provide the widest variety of services. They also offer businesses the most preferential policies and more convenient customs clearance procedures, which is conducive to attracting more foreign investment. China is now promoting CBZs as the most advanced form of SCSZs.

Basic policies in CBZs

TheGuidelines on Projects Suitable for Entry into CBZs, issued by the General Administration of Customs China (GACC) in April 2019, offers a list of preferential policies in CBZs, the categories of enterprises highly encouraged to do business in CBZs, and sample cases of entry projects for reference for potential investors.

Here, we summarize the basic policies of CBZs.

Preferential tax policy

- Goods entering CBZs from abroad are bonded in the zone;

- Goods from Chinese non-zone areas entering CBZs can enjoy export rebates;

- In-zone goods sold to domestic markets can be declared to customs, according to the relevant provisions on the import of goods, and be taxed, according to the actual state of the goods;

- Goods transactions between in-zone enterprises are exempted from value added tax (VAT) and consumption tax;

- Imported materials and equipment of capital construction will be exempted from tariffs and import-related taxes; and

- Other approved or authorized tax policies.

Trade control policy

No import and export quota or license administration shall be required for goods entering or leaving the country, unless specifically required.

Bonded supervision policy

- No storage period for bonded goods stored in the area; and

- Bonded goods can be transferred freely among enterprises in the zone.

Foreign exchange policy

Goods entering or leaving the zone (within the territory and outside the zone) may be settled in foreign currency or RMB.

Enterprises that are encouraged to do business in CBZs may include bonded processing enterprises, bonded logistics enterprises, and bonded service enterprises. A more detailed guidance on the enterprise categories can also be found here.

Policy trends in CBZs

In January 2019, the State Council issued the Opinions on Promoting High-level Opening and High-quality Development of CBZs, aiming to promote CBZs to become "five centers" – processing and manufacturing centers, R&D centers, logistics distribution centers, testing and maintenance centers, and sales and service centers.

The opinion announced 21 measures to facilitate in-zone enterprises to expand their business scope. The 21 measures include:

- Granting qualified in-zone enterprises the status of general VAT payers to better expand two markets;

- Allowing in-zone enterprises to import machinery and equipment for their own use and meanwhile allowing the imported machinery and equipment to enjoy related tax exemption in advance;

- Allowing in-zone enterprises to undertake domestic commissioned processing business;

- Exempting the automatic import licenses for mobile phones, auto parts, and other products for domestic sales;

- Simplifying customs approval procedures; and

- Others.

As of January 2019, China has a total of 140 SCSZs and 96 CBZs.

SCSZs rank the first among all kinds of economic development zones in China in terms of the intensity of investment per unit area and the industrial output, according to the GACC.

With further optimization expected as a result of the latest policies, SCSZs are poised to continue to play an important role in promoting foreign trade, coordinating regional economic development, and expanding employment.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.