We represent domestic and well known international brands providing IP support at the Cyprus Trademarks Registry, (CTR), EUIPO and WIPO. We are geared to gaining maximum protection for our clients' intellectual property rights. Our experienced IP team act aggressively against trademark abuse, passing off, counterfeit and IP fraud protecting our clients' rights both in the courts of the Republic of Cyprus and at the CTR.

Part of our work involves advising on developments on the IP tax regime of the Republic of Cyprus. The Cyprus IP Box regime aims to attract IP intensive companies and those engaging research and development by affording them highly attractive tax incentives and advantages.

The current Cyprus IP tax legislation was amended in October 2016 so as to be compliant with Action 5 of the OECD's Base Erosion and Profit Shifting (BEPS) project.The amendments apply retroactively, as from 1 July 2016.The revised legislation includes certain transitional provisions for IP assets that have already qualified under the existing IP box regime. In such cases, taxpayers will continue to benefit from the existing IP regime for a maximum of five years, after which date the new IP tax regime shall apply.

Under the new IP regime, the nexus approach is taken and for an intangible asset to qualify for the new tax benefits there must be a direct link between the qualifying income and the 'qualifying' expense contributing to the income. An amount equal to 80% of the qualifying profits earned from the qualifying intangible assets will be allowed as a tax deductible expense.

What is a qualifying intangible asset?

The provisions of the new IP box regime apply only to patents and patent equivalents, copyrighted software, utility models and other IP assets that are non-obvious, useful and novel. This means that any marketing related IP assets such as trademarks, logos or brands will not be treated as qualifying assets. The regulations provide that IP assets must be certified by a relevant authority either in Cyprus or abroad. Other IP assets which may legally qualify are:

- Intellectual property assets which provide protection to plants and genetic material, Utility models, orphan drug designations and extensions of patent protection

- Other novel IP assets but share features of patents (novel, useful and non-obvious) and are certified by a competent governmental agency in Cyprus or abroad.

The qualifying intangible asset is defined as an asset which was acquired, developed or exploited by a person (corporate or individual) as part of a business and it represents intellectual property which is the result of research and development.

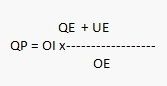

Qualifying Profit (QP)

Qualifying profit (QP) is defined as the proportion of the overall income (OI) derived from the qualifying asset, corresponding to the fraction of the qualifying expenditure (QE) plus the uplift expenditure (UE) over the overall expenditure (OE) incurred for the qualifying intangible asset.

Overall Income (OI)

Overall income is defined as the gross income earned from qualifying intangible assets during the tax year, minus any direct costs incurred for generating the income.

Overall Income (OI) includes, but is not limited to:

- royalties or other amounts resulting from the use of qualifying intangible assets

- license income from the exploitation of qualifying intangible assets

- any amount received from insurance or as compensation in relation to qualifying intangible assets

- proceeds from the disposal of qualifying intangible assets, excluding profits of a capital nature

- embedded income of qualifying intangible assets arising from the sale of products or services, or from the use of procedures that are directly related to the assets

For the purpose of calculating OI direct costs include:

- all direct and indirect costs incurred wholly and exclusively for the purpose of earning the income from qualifying intangible assets

- notional interest on equity contributed to finance the development of the assets

- the amortization on the cost of acquisition or development of the assets

Qualifying Expenditure (QE)

Qualifying expenditure for qualifying intangible assets is defined as the sum of all research and development costs incurred during any given tax year wholly and exclusively for the development, improvement or creation of Qualifying Intangible Assets. These costs must be directly related to such assets. Qualifying expenditure includes, but is not limited to:

- costs associated with R&D that has been outsourced to non-related persons

- general expenses relating to installations used for R&D

- commission expenses associated with R&D activities

- wages and salaries

- direct costs

Qualifying Expenditure does not include:

- costs for acquisition of intangible assets

- interest paid or payable

- costs for acquisition or construction of immovable property

- amounts paid or payable directly or indirectly to a related person to conduct R&D activities, regardless of whether such amounts relate to cost sharing agreements

- costs which cannot be proved directly connected to a specific qualifying intangible asset

It is noted that any expenditure for R&D that has been outsourced to non-related parties, as well as any expenses of a general nature for R&D, which cannot be allocated to the qualifying expenditure of a specific qualifying intangible asset, can be apportioned pro rata to the qualifying intangible assets.

Uplift Expenditure (UE)

An up-lift expenditure will be added to the Qualifying Expenditure, equal to the lower of:

- 30% of the qualifying expenditure,and

- the total cost of acquisition of the qualifying intangible assets, plus the cost of outsourcing to related parties of any research and development activities in relation to such assets.

How the IP Box regime works:

Tax benefit

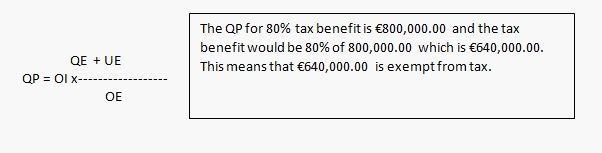

For the calculation of the taxable profit, 80% of the qualifying profit derived from the qualifying intangible assets is treated as a deductible expense. For each tax year the tax payer may choose to waive the allowance, either in part or in whole.

How it works using nexus ratio

The overall qualifying income generated from qualifying intangibles is multiplied by the Nexus Ratio and the resulting sum is eligible to an 80% exemption in tax. However a taxpayer that acquires the IP asset or outsources its development to a related party would have a much smaller ratio, thus a much lower tax benefit.

Below we set out an example of how the 80% notional reduction in tax would be applied.

Overall Income from Qualifying IP --€800,000.00

Overall Expenditure (OE) in the form of research and development of the IP product-€200,000.00

Qualifying Expenditure (QE) which is the internal research and development of the company not outsourced is €200,000.00

Uplift Expenditure (UE) being the lower of:

30% of the Qualifying Expenditure: €60,000.00 and total cost of acquisition plus costs of outsourcing research and development to related parties which in this scenario is zero.

Applying the above figures in the below formula

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.