Recent Tribunal Ruling (Sulzer Pumps) on Contract Manufacturing Operations

Recently,Mumbai Tribunal in Sulzer pumps India Pvt. Ltd. [TS-1156-ITAT-2018(Mum)-TP], had the occasion to distinguishbetween a 'contract manufacturer' and 'licensed manufacturer' while highlighting important Transfer Pricing Principles in connection with the same. The facts and decision are discussed below.

Conceptual Background

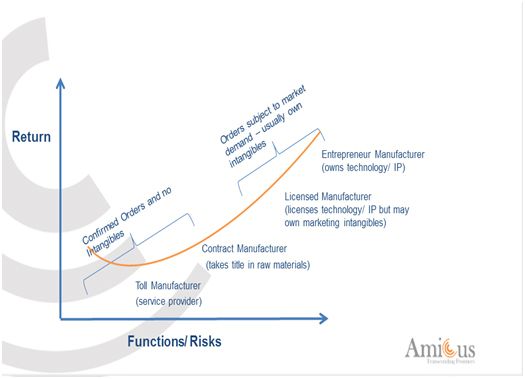

Transfer Pricing documentation and benchmarking is based upon the functional profile of the tested party. Within the broad categories of each functionality – manufacturer, distributor or service provider – there can be various shades of characterization. For example, a manufacturer can be a full-fledged manufacturer or a licensed manufacturer or a limited risk manufacturer such as a contract or toll manufacturer. The monetary return follows the risk – higher the risk, higher the return and vice versa. Below is a diagram illustrating the risk-return relationship for different kinds of manufacturers.

Contract Manufacturer

The manufacturer receives detailed instructions on what to produce, quality and how much to produce. The manufacturer bears low risk with a certainty that goods shall be purchased by the principal.

Licensed Manufacturer

The manufacturer makes multiple copies of product using licensor's technology or know- how. The remuneration to licensor is the license fee or royalty.The manufacturer bears all risks- associated with production such as market risk, price risk, capacity risk, manpower risk, etc.

Facts of the case

Appellant was engaged in the manufacturing and sale of power driven pumps. During the relevant financial year, appellant entered into international transactions for payment of royalty, technical know-how, purchase, sale and commission with Associated Enterprise ['AE'].

TPO

TPO observed that appellant had no exclusive right to sell manufactured goods without prior approval of AE. Hence, the assessee was a contract manufacturer and not a license manufacturer. The royalty payments to AE were therefore, disallowed.

Tribunal Ruling

Tribunal set aside TPO's order characterizing appellant as 'contract manufacturer'. Tribunal noted that the purpose of obtaining approval for sales from its AE was to avoid competition between AE's. Moreover assessee's export included substantial export to non – AE's clearly establishing that it was not a captive but operated in the open market exposed to the entire gamut of risks (price risk, market risk etc.). Therefore, the facts clearly indicated that assessee was not a contract manufacturer.

Amicus Comments

Characterization of the tested party based on its FAR (functions, assets and risks) analysis is the starting point in a Transfer Pricing analysis. Depending upon the extent of functions performed and risks borne.Taxpayers must ensure that their Transfer Pricing documentation (including inter-company agreement) mirrors the substance/ factual reality of their operations and inter – company dealings. Conformity of documentation and benchmarking with the actual taxpayer characterizations is necessary for a robust transfer pricing defense.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.