Introduction

This is the second in my series of articles on venture capital companies. In this article I look at the conditions relating to the investors. In particular, I look at the way the investors are permitted to hold their investments in the venture capital company ('VCC') in order to qualify for the tax concessions available to them.

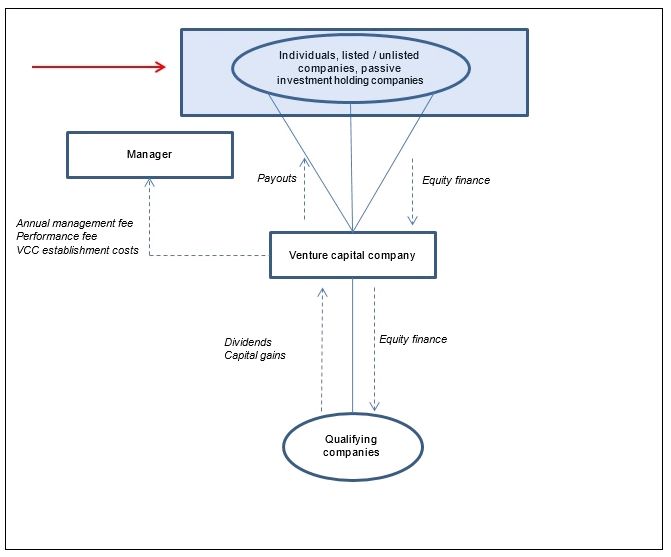

Venture capital companies – the investment process

The tax treatment of the investors

Who are the investors?

Investors in VCCs may be individuals or corporate entities. Under certain circumstances, individuals who subscribe for shares in VCCs may consider that investment as part of their retirement planning, particularly in the light of forthcoming retirement funding restrictions. Individuals may choose to invest directly in VCCs or through intermediate passive investment holding companies which will benefit from the dividends tax exemption and in certain cases lower rates of corporate income tax at 28% compared to individuals where the highest rate of personal income tax is 40%. However, companies suffer higher rates of capital gains tax compared to individuals: 18.6% compared to 13.3% respectively.

Operating companies which invest in VCCs should consider, apart from the tax benefits, whether such investment qualifies for enterprise and social development points in terms of the broad based black economic empowerment codes.

Upfront income tax relief

VCC investors enjoy an immediate tax deduction equal to 100% of the amount invested with no annual limit or lifetime limit (section 12J of the Income Tax Act, 1962 ('ITA 1962')). The tax relief is available provided that the VCC investor subscribes for equity shares, as opposed to buying them second hand from other VCC investors.

The VCC scheme only applies to VCC shares acquired on or before 30 June 2021. The VCC investor must support its claim for a tax deduction with a certificate issued by the VCC stating the amounts invested in the VCC and that the Commissioner approved that VCC.

The table below compares the effect of the upfront income tax relief on an individual, trust or company VCC investor. It assumes that the investor subscribes for shares in the VCC in an amount of R100,000. Although individuals are taxed at progressive rates of income tax I assumed for the purpose of this example that the individual is in the 40% income tax bracket.

Table 1. The effect of the upfront income tax relief

|

Individual / Trust investor |

Company investor |

|

|

Cost of the VCC investment |

||

|

Subscription in VCC shares |

R100,000 |

R100,000 |

|

Income tax rate |

40% |

28% |

|

(Less) tax relief |

(R40,000) |

(R28,000) |

|

Net cost of the investment |

R60,000 |

R72,000 |

|

Initial value of the VCC investment |

||

|

Gross subscription by the investor |

R100,000 |

R100,000 |

|

Issue costs (say 5%) |

R5,000 |

R5,000 |

|

Initial net asset value |

R95,000 |

R95,000 |

|

Initial uplift: (Rand) |

R35,000 |

R23,000 |

|

Initial uplift (Percentage) |

58% |

32% |

Taxable recoupment

The ITA 1962 specifically makes taxable any recoupment or recovery of an amount which was allowed to be deducted under the provisions of section 12J. According to the Taxation Laws Amendment Bill 2014 there will be no claw back of the upfront income tax relief if the VCC shares are held by the VCC investor for 5 years.

VCC shares are not listed

Unlike shares in real estate investment trusts there is no statutory requirement for VCC shares to be listed. Thus, VCC shares tend to be highly illiquid.

No capital gains tax ('CGT') relief

The investor does not enjoy any VCC-specific CGT exemption on the disposal of the VCC shares. Accordingly, CGT is payable upon the sale of the VCC shares. For individuals the maximum rate of CGT is 13.3%; for companies, 18.6%, and for trusts, 26.6%. Where a VCC investor claims the section 12J tax deduction on the subscription price for the VCC shares then the base cost of the VCC shares will be reduced to zero. As a result the investor will not have any base cost in the VCC shares to shield the subsequent proceeds from CGT. An exemption from CGT on the disposal of the VCC shares is needed.

Dividends tax

Investors will seek to make a return on their VCC investments either through dividends arising from dividends paid by the underlying companies to the VCC or dividends arising from the VCC disposing of the shares in the underlying companies.

Dividends received by the VCC investors in respect of their VCC shares are subject to the 15% dividends tax unless the investor qualifies for an existing dividend tax exemption. SA resident company VCC investors will enjoy the company-to-company dividend tax exemption. However, individual VCC investors remain subject to the 15% dividends tax.

No CGT reinvestment relief

It is not possible for an investor to defer the gain on another investment by applying the sale proceeds to subscribe for VCC shares. Thus, investors that sell their, say, Sasol or MTN shares in order to reinvest the proceeds in VCC shares will be subject to CGT on the sale of the Sasol or MTN shares. The after-tax proceeds from the sale of those shares will be invested in VCC shares.

No capital loss relief against income

Losses of a revenue nature can usually be set off against both income and capital gains, while capital losses may only be set off against capital gains. An investor in VCC shares that derives a capital loss will not be able to set off that capital loss against its income gains.

The investment in the VCC must take the form of equity shares

Equity shares are defined more restrictively than shares

The section 12J deduction is limited to a subset of shares defined as 'equity shares'. The terms 'shares' and 'equity shares' are used frequently throughout the ITA 1962. The 'equity share' incorporates the 'share' definition (equity share means any share) with an important exclusion. Equity shares exclude so-called fixed rate shares. Thus, where a share entitles an investor to a fixed rate dividend it is excluded from the definition of equity share.

Debt instruments ineligible

Since the tax relief is limited to 'equity shares' it follows that VCC investors will not qualify for the section 12J tax deduction if they subscribe for debt instruments in the VCC.

Hybrid equity instruments and third party backed shares ineligible

The VCC scheme also excludes hybrid equity instruments and third-party backed shares as these types of instruments have features in common with debt instruments and are therefore considered safer forms of investment.

Can a VCC investor borrow to fund its investment?

Although there is no prohibition on VCC investors borrowing funds to acquire VCC shares, the calculation of the section 12J deductible amount is subject to a number of requirements and limiting factors. There are two basic requirements:

- the first requirement: has the taxpayer used any loan or credit

for the payment or financing of the whole or any portion of the VCC

shares?

- The second requirement: does the taxpayer owe any portion of the loan or credit at the end of the tax year?

If the answers to both requirements are 'yes', then the taxpayer has cleared the first hurdle.

The second hurdle is a limiting factor. The amount which may be taken into account as expenditure that qualifies for a deduction must be limited to the amount for which the taxpayer is deemed to be 'at risk' on the last day of the relevant tax year.

A taxpayer is deemed to be at risk to the extent that the incurral of the expenditure to acquire the VCC shares (or the repayment of the loan or credit used by the taxpayer for the payment or the financing of the expenditure to acquire the VCC shares) result in an economic loss to the taxpayer were no income to be received by or accrue to the taxpayer in future years from the disposal of any VCC shares.

A taxpayer is not deemed to be at risk to the extent that the loan or credit is not repayable within a period of 5 years from the date on which the loan or credit was advanced to the taxpayer.

A taxpayer is also not deemed to be at risk to the extent that the loan or credit is granted directly or indirectly to the taxpayer by the VCC itself.

The exit mechanisms

Unlike a real estate investment trust (regulated by section 25BB, ITA 1962) the VCC shares do not have to be listed. This means that there is no ready market for the secondary trade in these VCC shares. It also means that existing investors cannot exit their investments by placing them for sale on the JSE.

The absence of a secondary market for the trade in VCC shares makes it difficult to understand how the proposal in the 2014 National Budget Review (proposing transferability of tax benefits when investors dispose of their holdings) would have been practically implemented. In reality, VCC shares will be illiquid. The VCC will have to offer the investors an exit route. Existing investors will in all likelihood realise value for their investments through:

- trade sale of investments by the VCC followed by a distribution

of cash to the investors;

- a repurchase of the investors' VCC shares by the VCC;

or

- a consolidation and listing of underlying investments and distribution of shares as dividends in specie to the investors.

Trade sale of investments by the VCC followed by a distribution of cash to the investors

In a trade sale the VCC sells all of its shares in an investee company to a trade buyer, i.e. a third party often operating in the same industry as the company itself. This method provides a complete and immediate exit from the investment.

The VCC will be subject to capital gains tax at the rate of 18.6% on the sale of the shares in the investee companies to the trade buyers. The VCC may distribute the after-CGT cash proceeds it derives from the trade sale to the VCC investors. These distributions may constitute a dividend or a return of capital or a combination of the two. Dividends distributed by the VCC to the VCC investors generally attract dividends tax at the rate of 15%. Certain VCC investors such as companies are exempt from dividends tax.

Return of capital payments fall under a different system of tax compared to tax on dividends. Return of capital payments are subject to capital gains tax. The main distinction between a dividend versus a return of capital distribution is based on whether the distribution comes from contributed tax capital ('CTC'). Distributions drawn from CTC qualify as a return of capital while distributions from other sources qualify as dividends.

Repurchase of the investors' VCC shares by the VCC

The investors will be subject to either dividends tax or capital gains tax or a combination of the two on the repurchase of their VCC shares. SA resident corporate investors will enjoy the dividends tax exemption. Thus, only individual investors will be subject to the dividends tax. One method for individual investors to defer the dividends tax is to hold their VCC shares through a passive investment holding company. The dividends paid by the VCC to the passive investment holding company will be exempt from dividends tax. However, the eventual distribution of cash flow from the passive investment holding company to the individual investor will be subject to dividends tax. This structure allows the individual investor to defer - not avoid - dividends tax. On the negative side the passive investment holding company is subject to 18.6% capital gains tax whereas the individual investor is subject to 13.3% capital gains tax.

There is no capital gains tax exemption at the investor level on the disposal of VCC shares. The VCC investor – whether an individual or juristic entity – will be subject to capital gains tax on the repurchase of their shares by the VCC.

There is nothing in the present set of rules that prevents a VCC investor selling its shares back to the VCC and using the proceeds to subscribe for another shareholding in the VCC. Although there are no rules that prevent the aforementioned repurchase-followed-by-resubscription scenario there are two rules that lessen the tax benefit for the VCC investors.

The first is that the VCC legislation contains a rule that an investor that becomes a 'connected person' in relation to the VCC after the subscription for the VCC shares is not allowed the upfront income tax deduction. However, a corporate investor only becomes a connected person in relation to the VCC if it forms part of the same group of companies as the VCC or if it holds at least 20% of the equity shares or voting rights in the VCC and no other shareholder holds the majority voting rights in the VCC. If a corporate investor keeps its shareholding below these limits and avoids the connected person classification then it may be able to benefit from this arrangement.

The second is that there is presently no capital gains tax exemption for the VCC investor when it disposes of the VCC shares. The VCC investor will have to reduce the base cost of the VCC shares by the amount claimed as an income tax deduction in terms of section 12J. Thus, a VCC investor which subscribes for VCC shares for R100,000 and claims that amount as a section 12J tax deduction has a base cost of zero.

Consolidation and listing of underlying investments and distribution of shares as dividends in specie to the investors

A distribution by the VCC that results in the disposal of shares

in the investee companies generates a capital gain or loss for the

VCC at market value as if the shares distributed to the VCC

investors were sold to the VCC investors at market value. This rule

exists as a matter of tax parity within the corporate tax system

– a straight asset distribution should have the same tax

impact as the VCC selling the shares in the investee companies

followed by a distribution of after-tax cash proceeds. The tax

considerations should accordingly be similar to the tax

consequences of the trade sale of investments by the VCC followed

by a distribution of cash to the investors which is discussed

above.

Please click here to view venture capital companies: an overview - part 1

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.