Outlook at a glance

As economies continue to rebalance, we encourage investors to position their portfolios to risk manage and exploit economic and policy differentiation. In our Global Investments Outlook report, we explore the macro outlook for the major economies across the globe, including the U.S., Europe, China, Japan, Australia, and Canada, the portfolio priorities that asset owners should look to adopt, and identify key investment opportunities.

For 2024 and 2025, we prefer a balanced portfolio, with a higher weight to government bonds, equity alpha and other uncorrelated diversifying alphas. This is because risks around our growth outlook are tilted slightly to the downside. We also expect interest rate volatility and government bond yields to fall. Finally, stock concentration, valuation and dispersion support active equities.

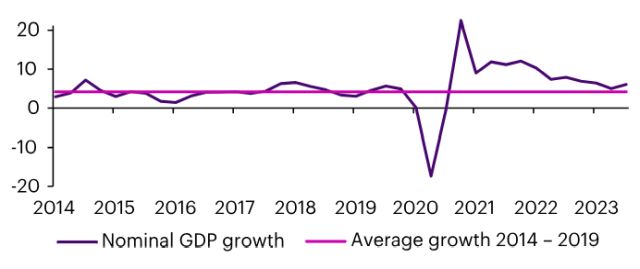

Nominal GDP growth is returning to a normal range

US nominal GDP growth, six-month chg. Annualised, % (regular)

Bond markets are pricing policy rates to fall in 2024 - we agree

Policy rates and market implied path, % (regular)

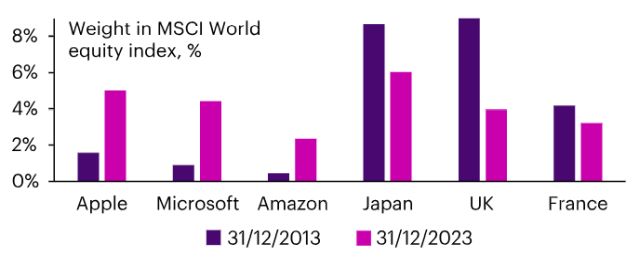

The size of three stocks in a global index almost equals all of the stocks in three major economies

Key economies

The U.S.

The Federal Reserve flagged important shifts in view in December. They are confident core inflation will hit target levels by December 2024. It expects to cut policy rates materially this year. It sees an economic soft-landing as the more likely outcome. We think there are two additional pathways in 2024 that deserve attention:

- Core inflation not falling as quickly as expected driving macro volatility.

- The Fed keeping policy too restrictive driving a minor recession.

Our portfolio strategy views take most account of the likelihood of a soft-landing or minor recession outcome.

Europe

The European Central Bank (ECB) could be the first to pivot to policy cuts, with Euro area GDP growth likely to remain relatively weak in 2024. Reductions in government spending will negatively impact growth. Manufacturing output should pick-up but subdued external demand and high gas costs will likely limit any rebound in activity.

UK macro volatility is likely to continue in 2024/25 but interest rate cuts are expected. We expect continued weak growth and a gradual slowing in core inflation. Weak growth is likely to support earlier and several interest rate cuts.

Japan

Japan has entered a self-reinforcing cycle of wage and price growth. We expect a pivot to tighter monetary policy in 2024, which is unique amongst the major advanced economies. Strong economic growth, company profit growth and indications of good future wage rises suggest inflation in Japan is sustainable. It also supports good return prospects for Japan equities in our view. The Bank of Japan is likely to tighten policy in response to good conditions – by allowing bond yields to rise, then interest rate hikes.

China

A challenging longer-run growth outlook drives GDP volatility for China. Industrial output growth has been slowing relative to its pre-COVID trend in 2022/23. Consumer confidence and spending has been volatile and slow to recover from successive pandemic lockdowns. Property weakness is also likely weighing on household wealth and consumption. Although, high savings rates offer some scope for higher spending.

Portfolio priorities

Diversify

For 2024/25, we prefer a balanced portfolio, with a higher weight to government bonds, equity alpha and other uncorrelated diversifying alphas.

- Interest rate volatility and correlations between equities and fixed income are high. We expect them to fall in 2024, supporting bond returns and improving the return benefits of diversifying alpha.

- Lower policy rates should support a move from cash to financial assets in 2024.

- All-in yields on fixed income are high, especially government bond yields. We think selective opportunities in private debt offer a good additional return pick up.

Downside risk hedging at the right price

Downside risk hedging is the process of analysing which tail events you would like to immunise your portfolio against and adding exposures – at the right price – that will provide a payoff if such a tail event occurs.

- Understanding the attractiveness of market pricing of downside risk hedging

- We expect nominal and real yields to fall over 2024, as central banks cut policy rates as inflation falls and/or if downside growth risks rise.

- US and selective other advanced economy government bond markets currently offer an attractive payoff and distribution of returns.

Opportunities for alpha

- Equities: use high quality active management to exploit likely greater variation in industry and stock returns.

- Private debt: exploit the full breadth of markets and flex capital towards areas with the most attractive risk-adjusted returns.

- Real assets: we emphasise the value in niche opportunities.

- Hedge funds: focus on uncorrelated diversifying alpha sources.

- Dynamic asset allocation: allocate capital to relative value, e.g., long UK government bonds vs. US bonds, rather than taking large directional positions.

Complete the form on the right, or below on a mobile device to download our 2024 Global Investments Outlook report.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.