How bad will it get?

Since our last Executive Report was published, I have worked with clients in the USA, the Middle East, Europe and Asia Pacific. All are, to say the least, worried and many are frightened by the state of the market. I am constantly being asked 'How bad will it get'?

I wish I could answer the question with certainty. What is clear is that 2009 will be considerably worse than 2008 and the global recession may extend well into 2010 and indeed beyond. All of this means that our industry will see unprecedented challenges, and some opportunities. At this time, the only mission, vision and objective is survival. The formulae for survival is remarkably simple in principle but extremely hard to execute. There are four priorities around which everyone in the

business should be aligned:

- Cash flow and debt covenant compliance.

- Risk management.

- Maximising each and every revenue stream.

- Optimising 'cost to serve' to deliver the brand promise.

Most clients we are working with are already on 'Plan B'. Some have 'Plan C' and 'Plan D' ready in anticipation of a worsening market. One thing is clear – the road ahead will be bumpy and there will inevitably be more casualties. There is no time for protracted analysis. Like a film set, one word says it all 'action'.

Alex Kyriakidis

STRONG FOUNDATIONS IN DIFFICULT TIMES

Tourism is both a driver and a beneficiary of economic growth, and nowhere has this been more evident in the past decade than across the Middle East.

According to the United Nations World Tourism Organisation (UNWTO) the region has seen the world's fastest – and most spectacular – growth in tourism since 2000. Some 46 million visitors chose to go there in 2007, a rise of 92% on year 2000 figures, giving the region hotel profitability that other regions could only marvel at.

That year, with strong economies encouraging more than 900 million international tourists to pack their suitcases, was a good one for hoteliers globally, with all major regions seeing an excellent performance in room rates and revenue per available room (revPAR).

By the middle of 2008, however, the credit crisis was making its presence felt, holding annual growth at under 3%, and UNWTO expects the deepening recession to keep this figure below 2% for 2009, possibly even 0%.

After an initial resistance to what was happening elsewhere in the world, the Middle East is now sharing the pain and we are seeing some dramatic discounting – particularly in Dubai, which has been the powerhouse of the Gulf.

However, we consider there are several factors – looked at in more detail here – that will shorten the time it takes the Middle East to recover. We also believe that these fundamentals will help the region emerge as an even stronger contender among the world's top tourist destinations.

Change of image

The accelerated transformation of the Middle East has been remarkable, with massive investment in hotels, airports, attractions, infrastructure and image, as the six nations of the Gulf Cooperation Council (GCC) have diversified from oil-based economies to business hubs and tourism destinations.

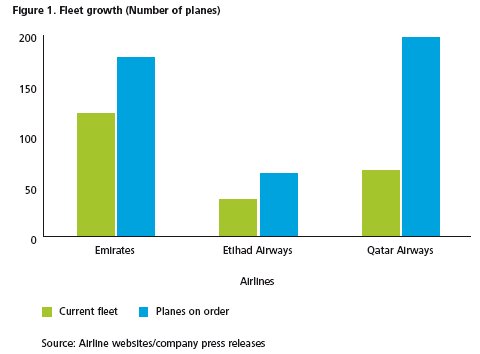

The region is also home to the world's fastest-growing airlines, with hundreds of aircraft set for delivery over the next few years. Emirates has firmly established itself as a global carrier, Etihad Airways and Qatar Airways are catching up (Figure 1), and airport development is underway across the region, including in Abu Dhabi, Doha, Dubai, Kuwait, Saudi Arabia and Egypt.

Several Middle East destinations now appear towards the top of Deloitte's 'top 20' revPAR league table, challenging Europe's traditional dominance. Dubai, of course, has taken much of the limelight in the last couple of years, attracting more than seven million visitors in 2008 (UNWTO), and enjoying some of the highest revPAR rates in the world. But other Gulf destinations, including Doha, Abu Dhabi and Muscat have been steadily moving up the league for both revPAR and occupancy, while other Middle East countries, such as Saudi Arabia and Egypt have been extending their appeal to broader demographic groups.

Some commentators have debated whether the pace of development over the past few years would enable the region to ride through the current economic crisis unharmed, but the dramatic decline in hotel occupancy and rates towards the end of 2008 and early 2009 tell the true story. Occupancy has fallen and continues to, with STR Global reporting a 10% year on year decline in December 2008. January 2009 has seen this continue, with Dubai being hit by a 30% decline in revPAR.

Although the region may have been protected by pre-bookings, high profile launch events and a positive view of business opportunities, the combination of a recession in source markets, pressure on currency exchange rates and an economic slowdown in the Middle East are now making themselves felt.

More rooms – lower rates

Dubai had been accustomed to one of the strongest average room rates in the world and, with occupancy levels of over 84%, the Emirate was used to being top dog. Towards the end of 2008, though, with demand falling away as the economy weakened, we have seen unprecedented 40-60% discounts and a surge in advertising campaigns to entice more visitors. Price has become critical to travellers' decision-making, especially with the changing values of the dollar against sterling and the Euro, yet customers expect the same level of service and five star quality for their reduced rates.

Dubai, like many other holiday destinations, is experiencing cost cutting among its target markets, but there are other contributory factors – mostly expected – that are adding to a drop in profitability. The supply of new hotel rooms, for instance, had been forecast to exceed demand from mid 2008 onwards, having a subsequent hit on both rates and occupancy.

Even though many projects have been delayed or cancelled recently, we have still seen a staggering increase in the number of rooms coming onto the market.

Even before the credit crunch's global domino effect, hotel industry analysts were expecting occupancy rates to drop to around 60%, with an accompanying fall in room rates. And, given the current situation, Dubai is considering revising its target of 15 million visitors a year by 2015 – almost double last year's total.

Dubai had been accustomed to one of the strongest average room rates in the world ... with occupancy levels of over 84%.

Fundamentals of success

There's no doubt that economic activity in the GCC has slowed. Stock values have plummeted, oil prices are below $40 a barrel, from a peak of $147, property prices have tumbled, and M&A transactions have all but ground to a halt. But there's an emerging consensus that the downturn in the Middle East will be short, thanks to continued investment, tactical government intervention and the amount of private liquidity in the region.

We also believe that the fundamentals for continuing success within the GCC's tourism sector remain unchanged. These include:

- The region's geographical position. Its location, midway between Europe and Asia gives it a competitive advantage when it comes to attracting travellers from both East and West – appealing to both holidaymakers and corporate visitors.

- A diversified mix of source markets, regional and international, contribute to the number of arrivals.

- Although some states and Emirates are now well developed in tourism terms, others are just starting. This means there is still considerable scope for expansion and diversifying into new target markets.

- The region is gaining a worldwide position as an aviation hub. This ambition was led by Emirates and is now supported by other airlines, including several low cost carriers.

- The six nations within the GCC have diversifying economies with secure medium-term wealth and significant budget surpluses.

- Millions of dollars have been invested in infrastructure – hotels, resorts, roads and airports – and investments are continuing.

- Year-round sunshine, which will tempt travellers to shrug off the gloom at home, is an added bonus.

These attributes, which have supported the vision of growth over the last decade, will sustain the next.

The right connections

Despite the current pressure, we believe the flexibility and responsiveness of the GCC nations will see them through. One of the main reasons for this optimism, as we have just highlighted, is the fact that the region's airports are so well connected to Europe and Asia and every Middle East airline is expanding.

While routes are being cut or closed elsewhere to contain costs, Emirates, Qatar, Etihad, Air Arabia and flydubai are all opening up new routes, expanding their airport hubs or increasing flight frequencies. Major European and Asian carriers also see the market as a key destination, and are increasing their schedules to the Middle East. This gives passengers greater availability and choice, which will intensify competition but also promote the region more widely as a preferred destination.

If we add this increased availability of flights to the high quality product on offer, plus the region's easy accessibility, and the year-round sunshine, we would expect demand to retain strength, especially as the price of a room comes down.

Arrivals in 2009 will not match the exceptional growth over the past four years, but few people thought this pattern was sustainable. Tourism organisations will therefore need to widen Dubai's appeal to more leisure travellers, who currently make up around 65% of arrivals, and less expensive rooms should help.

It will be a challenge for hotel owners and operators to maintain the service and quality levels that travellers expect in the Gulf, yet still keep a tighter control on budgets, and it will need a fine balance. A wrong move either way could damage tourism in the region.

However, increased interest from nearby Arab and Asian countries will be a bonus, with demand from India and Iran, for instance, said to be growing at over 10%. Even small increases from new source markets can boost overall profitability.

We expect the realities of a less affluent society to drive new business models, but as the market picks up again, these changes will help the Middle East consolidate and prepare for phase two of its dramatic transformation.

Still enormous potential

This year is not going to dazzle the world in terms of tourism numbers, but the underlying potential within the GCC remains strong. As the regional markets stabilise and confidence returns, there will be plenty of opportunities for serious investments and those who have positioned themselves correctly will be able to capitalise on the attractive valuations we are starting to see.

There will be a change of perspective, with the reliance on real estate to fund tourism and entertainment projects ending, and development across the sector becoming operationally sustainable in its own right.

Governments here, as elsewhere, will need to focus on the long-term value of public spending in the sector, with 2009 budgets among the largest seen in the region. They must also recognise that the wider economic benefits of tourism can only be achieved through a structured, co-ordinated strategy.

Tourism in the Middle East is part of an established plan to deliver future revenues, and the responses we are already seeing from business leaders, investors and Government in the current cash crisis confirms this commitment.

This relatively new industry among GCC nations has been the outstanding success of the last decade, with groundbreaking projects that have captured the imagination as well as the media's attention. We should therefore not be surprised to see the Middle East take a more prominent position in the global tourism, hospitality and leisure landscape of the future.

HITTING STORMY WEATHER

The aviation industry is no stranger to difficult times. In the past decade it has faced multiple challenges in the form of terrorist attacks, war, tighter security, the SARS pandemic, the demise of Concorde, mounting environmental pressures, and the influx of low cost airlines entering an already saturated marketplace.

In recent months these troubled skies have turned darker than ever. The credit crunch, wildly fluctuating fuel prices and exchange rates, together with the deepening global economic downturn are combining to turn a difficult market into one of extreme turbulence.

In this article we take a look at some of the key problems faced by the UK and European aviation industry and assess the prospects for the months ahead.

The urge to merge

2008 was a year of airline failure. The prediction that tens of airlines would go bust made at the beginning of the year by British Airways plc boss Willie Walsh proved correct. By the end of September at least 30 carriers had failed globally, including Silverjet, Zoom Airlines and XL Airways in the UK market.

Consolidation is increasingly likely. Although M&A activity has almost dried up in most other industry sectors, the huge fixed cost base of airlines makes this an attractive option in difficult times. Mergers enable operators to significantly reduce their overheads and increase their buying power.

Numerous airlines, including some high profile 'flag carriers', are now in a precarious position and are looking to larger competitors to take them over. The CEO of Ryanair, Michael O'Leary, has predicted that once the dust has settled only four major European airlines will remain: Air France-KLM, Lufthansa, British Airways (BA) and Ryanair.

Key concern

This prediction may have some foundation. Recent months have seen a surge towards consolidation with speculation surrounding Alitalia, Olympic Airlines and SAS Scandinavian Airlines, the proposed merger of BA with American Airlines and lberia Airlines, the continued attempts of Ryanair to acquire Aer Lingus, Lufthansa's acquisition of bmi and its purchase of significant stakes in Brussels Airlines and Austrian Airlines.

The coming months are likely to see further failures and acquisitions. It remains to be seen whether takeovers of troubled airlines will occur prior to their failure or whether potential buyers will wait until their collapse in order to achieve a better deal with the administrator. The key concern for the boards of the acquiring airlines will always be how they can gain control of the airport slots. Many will conclude that they cannot afford to wait, but questions remain over whether they will have the cash to do the deal.

Protective instinct

The drive to consolidate is occurring within Europe and the US, although ownership restrictions prevent airlines from one political jurisdiction taking a controlling interest in those from another. Recent speculation has surrounded the possible takeover of troubled European carriers by airlines based in the Middle East or Russia, but in reality these potential acquirers are prevented from taking a controlling interest in EU based airlines.

The next phase of the bilateral Open Skies agreement between the US and EU calls for the liberalisation of ownership rules from 2010. However, it is highly unlikely that US Congress will agree to this and President Obama is thought to be opposed to the foreign ownership of US airlines. In theory this could also lead to the EU revoking the first stage of the Open Skies agreement, which came into effect on 30 March 2008, although many industry commentators do not believe that the EU will take such a step.

Open Skies agreements are needed to provide a true level playing field in the international aviation industry and to prevent Governments from propping up airlines that are clearly not viable as standalone businesses, such as Alitalia. However many Governments still view their flag carriers as essential national assets and take a protectionist stance.

Low cost death?

Rising fuel prices and the slide into recession during 2008 have led a number of industry commentators to predict the 'death of low cost air travel'.

Many airlines only achieve wafer thin margins even in favourable economic times, and in the current climate a number of low cost and business class only carriers have failed. Nevertheless it is still too early to write the obituary of budget air travel. Ryanair and easyJet have been quick to implement innovative ways to cut costs and raise ancillary revenues from services that customers once took for granted. These additional revenue streams enable budget operators to offer lower fares than the flag carriers. Michael O'Leary has stated that his company will not deviate from its core business proposition of offering the lowest fares.

The additional fees imposed by low cost carriers, referred to as 'a la carte' pricing within the industry, continue to attract complaints of 'stealth charging'. However, by breaking down prices into their component parts, low cost airlines do offer consumers the choice to reduce the fares they pay.

Budget advantage

For example a passenger making a booking online, paying by debit card, checking in online and carrying just hand luggage will pay considerably less than a customer choosing to pay by credit card, checking in at the airport and putting extra baggage in the hold.

When customers check in online and take only hand luggage this allows the airline to avoid payments to the ground handling company at the airport. Hand luggage also weighs less and therefore makes for more fuel efficient aircraft.

Being able to implement such measures gives the low cost carriers an advantage over the flag carriers whose customers expect these services to be provided as part and parcel of the fare. A move to introduce these optional charges by flag carriers could be detrimental to their customers' perception of the airline.

Demand still strong

Turbulent times have clearly taken their toll on low cost airline profits with Ryanair's recent 3rd quarter results showing a loss of €102 million, a swing of €147 million compared to 2007, and easyJet's year-end results down 45% to £110 million. Nevertheless passenger numbers for both carriers have continued to increase and load factors have remained above 80%, demonstrating that customer demand is still strong. Holidays in the sun appear to be the luxury the British consumer is most reluctant to sacrifice.

In the wake of a number of failures affecting smaller low cost airlines consumers may be less driven by price alone than they were in the past. Yet in these difficult economic times both leisure and business passengers are still seeking clear value. Given the strong cash positions of both Ryanair and easyJet and the recent fall in fuel prices there is still plenty of life in the low cost model.

First class exodus

Despite the squeeze on low cost margins both Ryanair and easyJet have still performed better than BA whose 3rd quarter unaudited results showed a loss before tax of £70 million, compared to £816 million the prior year comparative. There are forecasts that their overall loss will be £150 million for the year to 2009. The British flag carrier has been hit by the slump in premium and business travel, coupled with the steep rise in fuel prices. Recent results from both SAS and Air France-KLM also reflect these issues.

Many flag carriers are struggling to cope with the decline in passenger numbers, with the impact felt most sharply at the front end of the aircraft. The days seem long gone when these carriers were guaranteed high margins from filling the business and first class sections on their transatlantic routes.

The pendulum swings

With the fall in overall global passenger numbers since August 2008, the pendulum of power in the industry seems to be swinging away from the airports towards the airlines, particularly at the regional UK airports.

We have seen some sizeable hikes in the pricing of landing charges in recent times, mainly driven by excess demand at many of the key European airports. However, as airports become slightly more dependent on airlines for their business this is likely to strengthen the hand of carriers in their negotiations over charges.

This is further good news for the low cost airlines in their battle with airport authorities over landing charges. Given Michael O'Leary's well publicised views on the charges levied by BAA it is no surprise that Stansted, a BAA airport, has borne the brunt of Ryanair's winter groundings as it attempts to cut costs.

Heathrow threat

Frequent travellers are only too familiar with problems at Heathrow and will be keenly aware of the UK's lack of investment in infrastructure when compared to other European airports. There is a serious risk over the next few years that Heathrow could lose its dominance as a key hub for the European market.

We are also seeing great interest in the fight for ownership of Gatwick Airport with several consortia throwing their hats into the ring. Several of these are being supported by the local airline community and it remains to be seen who will claim this rich prize. Whatever the outcome most industry analysts believe it can only be good for the airlines as well as for the consumer.

Green agenda

With the industry already struggling to cope with fluctuating fuel prices, weakening customer demand and an even more competitive market, the EU also announced in October 2008 that it will include the aviation sector within its proposed Carbon Emissions Trading Scheme. The timing of this announcement could not have been worse as this will put European based airlines at a competitive disadvantage when compared to rivals based elsewhere.

The Sustainable Aviation Fuel Users Group (composed of nine airlines), the World Wildlife Fund, the Natural Resources Defence Council, Boeing and Universal Oil Products drew up a charter during 2008 to help improve the impact that aviation has on the environment. This charter remains only a proposal and is not yet a legally binding agreement to ensure a global level playing field for any green agenda imposed on airlines.

However, the current financial crisis is helping to improve the industry's green credentials by encouraging airlines to use the most fuel efficient aircraft. New aircraft, such as the Boeing 787 Dreamliner and Airbus A380, are far more fuel efficient than the models they replace. Already airlines such as easyJet and Flybe have made significant investments in their fleets to ensure their aircraft use less fuel, improving their profitability as well as their green credibility.

Survival of the fittest

Although the reduction in fuel prices will provide a small respite for airlines this winter, the next six to twelve months are likely to see further significant changes, losses and failures within the industry.

Capacity and routes are likely to be cut further as business travel continues to fall. Some of the new routes launched from Heathrow as a result of Open Skies have already been withdrawn. Meanwhile, it remains to be seen how much the collapse in consumer confidence will affect leisure bookings in 2009.

Winter is traditionally the period when airlines, in the Northern hemisphere at least, burn cash rather than fuel. Those which are already in financial difficulties may struggle to survive a winter that promises to be longer than usual, especially with the troubled banking industry restricting credit or imposing more onerous terms on facilities already in place.

The International Air Transport Association has forecast that the global airline industry will post losses of US$5 billion in 2008 and $2.5 billion for 2009. To put this in perspective, in 2001 and 2002 industry losses amounted to a massive US$25 billion in the aftermath of the September 11th terrorist attacks. The current crisis has not yet reached that scale but there are certainly turbulent times ahead for the sector.

ECONOMIC WOES THREATEN HOTEL PERFORMANCE

Given the global financial crisis, unprecedented levels of Government borrowing, and daily reports of job cuts, it's not surprising that consumer and business confidence wilted during 2008. Weakening currencies – with the pound falling to a record low against the Euro – and rising inflation in many regions put the damper on spending, even though some Governments insist this is the best way to kick-start their economies.

Analysis by Deloitte, shows that – not surprisingly – hoteliers found it harder to fill rooms towards the end of 2008. Many of the big cities reported drops in occupancy levels, as both tourists and corporate travellers tightened their belts. With the demise of several airlines and demands for seats falling, some operators decided to cut routes out of their schedules, and, of course, declining passenger arrivals meant fewer people looking for a bed for the night.

As tourists started to think twice about trips away, there was a significant slowdown in revenue per available room (revPAR) in most world regions, particularly in the final quarter, as data from STR Global highlights. North America ended the year with a 1.6% decline, while Asia Pacific and Europe saw growth of less than 2%, in US dollars. Central and South America and the Middle East however, went on to turn in double-digit revPAR growth, up 14.5% and 18.3%, confirming that, even though the market is difficult, it is not uniformly grim around the world. As we head further into the new year, the economic situation is changing constantly, making it hard to predict what will happen across the hotel sector even a few weeks in advance. It's likely that revPAR, the critical barometer of hotel performance, will face increasing pressure.

While Dubai has had to put the brakes on, the Middle East was still way ahead in terms of revPAR growth, which soared 18.3% to US$148. The region also had the highest occupancy rates in the world, 68.8% – up 1.2% on the previous year. Average room rates rose 17.0% to US$215.

Most cities across the Middle East posted double-digit revPAR growth in 2008, apart from Dubai, where revPAR rose just 0.8% to US$237. However, as Dubai has enjoyed exceptional growth over the last five years, with occupancy nudging 80% and average room rates of US$300, analysts expected the upward trend to level off.

In neighbouring Abu Dhabi, which has injected millions of dollars into Dubai's economy recently, revPAR shot up 46.0% to US$230. Occupancy reached 81.5% and US$71 went onto average room rates, taking the figure to US$281.

Boost for Beirut

The best growth across the Middle East, however, was in Beirut, where the country has started to pick up after years of political turmoil. The city, once one of the most popular destinations in the region, reported exceptional revPAR growth of 101.1% to US$95. Business travellers and tourists are now feeling more confident about visiting Beirut, and occupancy rose to 55.2%, a great improvement on 36.0% last year, when the city's turbulent politics deterred tourists.

In Central and South America, revPAR was up 14.5% in 2008, to US$77. This growth was mostly due to a 13.4% increase in average room rates, taking it up to US$116. The weak US dollar, which kept US travellers closer to home, made the region more popular with American tourists, and in Sao Paulo revPAR was up 21.2% to US$60. This was primarily driven by a 17.3% boost in average room rates, up by US$14 on last year to US$92. Santiago and Buenos Aires also reported double-digit revPAR growth for the year, up 25.4% and 10.6% respectively.

Hotels across Europe did better when measured in US dollars than in their own currencies, as revPAR was up 1.8% in US dollar terms, with an absolute revPAR of US$104, but down by 5.1% in Euros. Average room rates across Europe ended the year at US$159 while occupancy fell 3.7% to 65.7%.

Within the Euro zone, Brussels reported strong performance during 2008, up 12.2% to US$117. This was mostly due to average room rates, which were up by 14.4% to US$168 compared to 2007.

Demand remains high in Brussels, where hotel rooms are generally less expensive than Europe's other capital cities, so occupancy remains high at 69.7%.

Corporate business, due to European Commission conferences, also helped fill rooms and demand would have been even higher if French President Nicolas Sarkozy had not decided to re-locate some meetings to Paris.

Feeling the cold

The complex chain of events that caused the world's economic crisis blew a particularly chilly wind across Iceland. The collapse of the country's banks hit savers and institutions in many other countries, and Icelandic tourism also took a dive.

Iceland's capital city Reykjavik saw one of the largest drops in revPAR during 2008, falling 21.5% to US$85. Occupancy fell to 61.7% while average room rates tumbled by US$27 to stand at US$138. Due to exchange rates though, the performance measured in local currency, rather than the US dollar, is more positive and shows a 6.4% increase.

In Asia Pacific, hotels reported a 1.8% growth in revPAR during 2008 to US$91. Average room rates were responsible for this rise – up 9.7% to US$139. Occupancy counterbalanced this however, and fell 7.2% to 65.5%. Across the region, Bali had the highest growth in revPAR, up 27.2% as it steadily re-builds its tourism business after the terrorist bombings in 2005.

Another of the region's success stories was Beijing, which hosted the 2008 Beijing Olympic and Paralympic Games. As China welcomed the world's media, and millions of visitors poured into the city, average room rates soared 450% and occupancy ranged from 88% to 92%. The 2008 Beijing Olympics helped lift revPAR in the city 8.5% to US$83, thanks to a staggering 36.0% increase in average room rates, taking the final figure for 2008 to US$151. Occupancy, though, was down by more than 20% to 55.3%, a combination of extra capacity coming into the market for the Games and the usual lull in visitors after the Games, as experienced by previous host cities.

Sport also boosted hotel business in Singapore, when the city hosted the inaugural Formula1 SingTel Singapore Grand Prix in September. RevPAR here rose 16.9% to US$164 as a result of average room rates rising US$46 year-on-year.

The most sluggish hotel performance in 2008 was in North America. This is not surprising, given the severity of the economic crisis. RevPAR was down 1.6% to US$65 and, although average room rates rose 2.5% to US$108, occupancy was down at 60.6%.

The only city to see double-digit growth was New Orleans, where revPAR was up 10.1% and occupancy rose 8.6% to 62.6%. Average room rates in the city also grew US$1 to US$118, as the city regains the tourism business it lost so dramatically in the wake of the hurricane. To increase its appeal among British tourists and investors, New Orleans' football team re-located one of its 'home' games to London during 2008. As part of this week-long promotional campaign, the organisers staged a mini-Mardi Gras, giving Londoners a taste of New Orleans' culture.

Hold the rate?

Looking back over 2008, there were many positive stories across the tourism, hospitality and leisure sector. However, growth in most regions started to slow towards the end of the year, as Governments and commerce struggled to cope with the worst financial turmoil for decades, and we can expect revPAR to suffer further in 2009.

Few market segments will escape the downturn as both consumers and businesses scrutinise spending more closely, particularly on 'luxury' items such as travel. We are therefore likely to see many more operators offering special deals and two-for one packages, while potential customers sharpen their negotiating skills.

The real dilemma for hotel businesses will be whether to discount average room rates heavily now, to attract more customers, or whether to hold steady so that the business recovers quickly when demand picks up again.

UNCERTAIN TIMES CALL FOR A SHARPER FOCUS

Few people were able to predict the speed and scale of the economic fallout that has followed the credit crunch.

A complete shake up of the global banking system, household names going into administration or being taken over, unprecedented bail outs by Government and thousands of redundancies have kept business news on the front pages for months, while falling house prices and rising inflation have pushed anxiety levels even higher.

With some senior banking figures admitting they did not see this downturn coming, it is not surprising that many business leaders – despite some early warning signs – were also wrong footed by the rapid dive into recession, especially as the global economy had been enjoying an period of unprecedented growth over the past seven years.

While Governments debate tactical solutions to get things moving again, senior managers recognise they only have a short time in which to reposition their businesses if they want to remain profitable. In this article, we highlight the best ways to drive down costs while pushing up efficiency. Our proven methodology will not only sharpen up the business now, it will ensure organisations in the tourism, hospitality and leisure sectors are in the best possible shape to take advantage of a resurgent economy.

Management basics

When business is good, as it has been across most sectors for the past few years, inefficiencies are either not seen or are simply tolerated by management. While going for growth, many organisations will have overlooked the basics of sound management.

A typical example is in recruitment. With sustained demand for products or services – whether that is hotel rooms, flights, or business conferences – recruiting extra staff to reduce pressure on existing employees is an obvious step. However, if newcomers are brought into the organisation at a frenetic pace, roles and responsibilities can become vague and may often overlap.

As a result, the company becomes unstructured, reporting lines become blurred, marginal staff become less and less effective and there is no time for management to step away from their day-to-day workload and assess the organisational structure holistically. They rarely have the time to ensure the right people are in the right teams, or that employees' incentive packages are a proper reflection of their worth to the company.

Similarly, business processes – which may have been defined when the working environment was quite different – become increasingly inefficient when the business is growing and evolving. New employees, insufficiently trained in how the company operates, may create their own processes or amend traditional ones to suit their own preferences. When this happens, managers often seek to increase their spans of control by creating additional approval steps. In both cases, overall efficiency declines.

Technology, which can be a great enabler of business, often becomes more complex than it needs to be when an organisation is expanding or moving into new markets. There are several reasons for this. Sometimes, a department will develop a 'need for speed' scenario, and new applications, hardware or software will be brought in to maximise potential new business opportunities. These costly bespoke solutions may not fit with the legacy infrastructure, and may increase maintenance and software licence costs for years to come.

Alternatively, an eager divisional executive – keen to expand customer services – may say the company simply cannot wait for the IT department to respond, and so an application is bought directly from the vendor, and implemented without any in-house technical support. Both steps not only complicate the organisation's technology base and make it more expensive to operate, but they can in addition fracture the existing data management system.

This means that executives wanting the latest sales figures, revenue per available room performance or occupancy rates, for example, may find themselves looking at conflicting reports. The fact that there are 'many versions of the truth' available prevents management information from being the most timely and accurate. Subsequently, business decisions are taken without access to reliable data. Equally, management find it increasingly difficult to make decisions as they do not know which sets of data to believe.

Another scenario is when marginal initiatives are approved without normal rigorous checking procedures. These classic symptoms are related to 'general' inefficiency rather than one specific cause. Managers will be familiar with many of them and may include projects being late and over budget, decisions on straightforward tasks such as booking travel and approving expenses taking far too long, and high numbers of frustrated employees leaving the company because they cannot perform their jobs properly.

This leads to an internal culture of blame, with staff citing other departments – often people in Finance – for problems within the business. A system of 'route one' approval develops, with employees circumventing the least senior departments and going straight to the top to get immediate decisions. Naturally, all these internal logjams and irritations will become visible to clients and business partners, who may start to question the overall quality of the organisation they are dealing with.

Costs down, efficiency up

The first thing to do when these classic symptoms appear is to drive focus and direction back into the organisation. A structured approach is the only workable solution and it underpins the Target Operating Model (TOM) (Figure 1), developed by Deloitte and already helping several major clients in the hotel and leisure industry. To achieve the twin goals of reduced costs and improved business efficiency, this model looks at each organisation in nine inter-linked layers, as shown.

The model uses an organisation's strategic direction – or business objectives – as its reference point, defining what the organisation needs to achieve in the next year or two. This approach makes the methodology useful to divisions or large departments as well as to the entire enterprise, and applies the reference point to each of the nine layers. This will ensure every aspect of the company is aligned with the overall strategy, with the organisation focused on its core markets and most valuable customers, offering them the most profitable products and services in the most cost-efficient ways.

It will fine tune the company to check that:

- data is structured to avoid duplication;

- the right systems are in place to support efficient processes;

- the structure supports these processes and delivers correct accountabilities;

- employee numbers and skill sets are right for the business; and " operations and people are based in the right locations.

The TOM model is flexible enough to select the most appropriate layers for each organisation and to vary the depth of analysis to suit particular situations. Experience has shown us, however, that the core layers demanding most attention are: organisation, people, processes, data and technology.

Take five layers

It may seem obvious, but the most critical step is to define the capabilities an organisation needs to deliver its strategy. These can cover Marketing, Corporate Planning and Residential Operations for instance, forming the basis of the functional design whereby capabilities are grouped together and organised in a logical way.

Here, organisations need to consider issues such as separating strategic functions from operational functions and the potential deployment of a shared services model. From this functional design – and still based on the business strategy – the next step is to create the organisation design, which models the organisation structure through departments down to individual role levels. At this point, it will become clear which roles, and at what level, will be required to delivery the strategy, although this does not yet relate to full time heads.

With the ideal organisational structure defined, current staff have to be matched to these roles. Capability matching will help management have the right people in the right roles, check that individuals are not overloaded with conflicting demands on their time, and identify capability gaps that need to be filled by new hires. Learning and development needs can also be defined at this stage, and staff who do not possess capabilities for any role need to be managed out of the business.

Re-engineering the core business processes works in three stages. First, the current processes are documented; second, detailed analysis and comparison with best practice and the new organisational structure takes place; and third, processes are then re-engineered where necessary. This not only streamlines processes and makes them more efficient, it ensures they are aligned with the new organisational structure.

Most data is stored on large databases and manipulated through the company's IT systems, so it makes sense that these two layers are analysed together. The current data model and application architecture therefore needs to be documented to identify disparate, unsynchronised and duplicated data sources, and standalone or overlapping applications. An analysis enables the company to highlight areas that can be improved.

The need for change

Using the TOM approach with a leading Middle East hotels and resorts organisation recently, we were able to completely re-focus the company, so that real estate development and real estate operations, that were once combined, were restructured to become separate business units to give clarity between these two differing business activities.

The organisational structure was redesigned, business processes streamlined, existing technology was utilised more effectively to support the core business requirements, and gaps in essential skills were identified. Through these important changes, the company is expecting to save tens of millions of dollars on future development plans and reduce its payroll bill by around 20% per year.

We found that, as in many organisations that have developed rapidly in an expanding market, executives had been so busy keeping pace with the business that they had not recognised the need for change until some of the classic symptoms mentioned earlier came to the surface. Developments were late and over budget, staff were becoming increasingly frustrated by how long it took to make any headway, the company structure was just too complex and the technology was under utilised. Executives realised their business model would come under strain in a normal market and the deepening economic downturn forced them to sharpen up their strategic focus.

Of course, surviving the current financial turmoil will call for more than a properly structured organisation, with skilled employees and efficient processes – but making sure all these basics are in place, and that there is a relentless focus on the core business, will go a long way to keeping a company successful.

EXPLORING SOVERIEGN TERRITORY

Sovereign wealth funds (SWFs) have made headlines with high profile capital injections into western banks, investing more than $80 billion over the past two years.

But how relevant are these funds for the tourism, hospitality and leisure industry and, given the dramatic changes in the economic environment, how relevant will they continue to be?

To both questions the answer is very, although the impact of the changing global economy is likely to change the focus and direction of their investments. SWFs will continue to invest in the industry, but are likely to prioritise those investments that are most value-generative for their local economies. It is therefore imperative for our industry to understand who SWFs are, what they invest in, what their investment criteria are, and how they are likely to act in the future.

The 'Super 7'

SWFs are typically established by nations that, as a result of their current account surpluses, have accumulated more reserves than they need for their immediate purposes. As a result these countries establish a sovereign fund in order to manage those 'extra' resources.

The funds have existed since the 1950s but until recently have attracted little attention. The past three to five years have seen them rise from relative obscurity to one of the most hotly discussed topics in financial, political, economic and business circles. This sudden interest has been driven not only by their dramatic increase in size, but also by their changing strategy and growing appetite for risk and high profile investments.

SWFs grew from an estimated $500 billion in 1990 to almost $3 trillion by the beginning of 2008. To put this in context, they are approximately two and a half times the size of the world's private equity funds or twice the size of the world's hedge funds.

This growth is expected to continue with their assets under management (AUM) projected to reach $10 trillion by 2015, even taking into account paper losses of 25%-35% during 2008 and reduced oil prices.

Although more than 20 countries currently have such funds and half a dozen more have expressed an interest in establishing them, SWF holdings remain quite concentrated. The 'Super 7' funds (those managing assets of over $150 billion each) account for more than 70% of total assets.

Beyond the seven

Despite this high level of concentration, $150 billion is a high benchmark and it would be amiss not to look beyond this group. Funds like the Qatari Investment Authority ($65 billion), Investment Corporation of Dubai ($81 billion), Bahrain Mumtalakat Holding Company ($13 billion) and Mubadala Development Company ($10 billion) also have significant wealth at their disposal and have made many high profile investments.

It is also a mistake to think that SWFs face the market as a single entity. For example, the world's largest fund, the Abu Dhabi Investment Authority (ADIA), makes use of many different, relatively autonomous subsidiaries, each with its own investment strategy, pool of capital, management and reporting structure.

In short, SWFs are clearly big enough to warrant our full attention and they are only going to get bigger. So other than their much publicised recent foray into financial services, what do these institutions actually invest in?

Some more transparent than others

One of the most debated aspects of SWFs is a lack of transparency. Most have little or no publicly available information on their investment strategy, financial performance and source of funds. The level of transparency differs greatly between funds, and wide spread generalisations are not appropriate. For example, although some funds in the Middle East disclose very little information, the Bahrain Mumtalakat Holding Company has won international acclaim for their open and transparent disclosure of their holdings and investment strategy.

Diverse scale and scope

Knowing who you are dealing with is of the utmost importance because, although funds might seem alike at first glance, their investment scale and scope differ significantly.

For example, the Norway Government Pension Fund is highly risk averse as it invests only in bond and equities markets and never acquires more than a 3% stake in any company. This probably explains why few people have heard of it even though it is the world's second largest fund.

Asian funds have tended to show an appetite for higher risk and have invested in assets beyond their country's borders to enhance the purchasing power of their reserves. Their most significant recent investments have been focussed on propping up the world's failing financial institutions but in reality their investment range is far more diverse.

For example the Government of Singapore Investment Corporation (GIC) has long been an investor in real estate and is thought to be one of the top 10 investors in property worldwide. However Asian funds tend to be strictly joint venture or minority investors and tend not to take overall control of operations.

Middle Eastern funds have shown an even greater appetite for risk, seeking to acquire assets and brands that will continue to generate wealth when the oil has run out. They too have made high profile minority investments in financial institutions and other large listed companies – examples include DaimlerChrysler, EADS and General Electric. In contrast with most Asian funds they have also been willing go to the next level and gain control either through private equity style deals or leveraged buyouts. Acquisitions of $1 billion or more include the Doncasters Group (UK), Mauser (Germany), Alliance Medical (UK), as well as trophy assets like The Chrysler Building, The Rockefeller Center, 280 Park Avenue, and the W Hotel – all in New York.

Tourism, hospitality and leisure targets

Most SWFs have diversified investment strategies. Within the tourism, hospitality and leisure (THL) sector, businesses and their underlying real estate assets have both proved to be attractive targets. Middle Eastern funds have focused their attention on acquiring brands with the aim of rolling them out globally and regionally. Examples include Cirque du Soleil, UK budget hotel operator Travelodge and The Tussauds group.

GIC has also long been an investor in hotel real estate, and involved in the acquisition of more than $3 billion in hotel assets over the past three years, from the 73 UK hotels sold by InterContinental in 2005, to the Hotel Arts Barcelona and the InterContinental Paris.

The long-term investment characteristics of THL businesses and their underlying real estate are a good match with the requirements of certain SWFs. Nonetheless, THL assets still represent a relatively small proportion of SWF portfolios. There is clearly scope for significant growth, both through minority investments and majority acquisitions.

It's not who you know it's who knows you

Thinking of SWFs as 'easy money' is far from the truth. Increasingly sophisticated, they will not commit to an investment unless it makes compelling sense. This is particularly so given current market conditions, although highly-focused due diligence, and discretion, are key characteristics that SWFs expect of any deal.

These funds are highly sought after. Any business seeking to attract capital from a SWF must convince them that their opportunity will generate greater longterm value than the hundred other opportunities the SWF is likely to see that week.

Decisions are typically made by a few very senior principals within the organisations and having connections with the right people is of the utmost importance. This means relationship-building is fundamental to success. It also means trust takes time to build, but perseverance will be rewarded.

Available equity

Working with SWFs does have some very significant advantages. Firstly, they are one of the few players that have readily available equity in the current market. However, do not imagine they do not use debt. SWFs make use of leverage to get more 'bang for their buck' just like everyone else, however they still have a competitive advantage over other investors as they are able to make use of lower gearing levels.

Secondly, SWFs are patient pools of capital with longterm horizons and, unlike private equity or hedge funds, are not looking to exit investments in the short-term. This enables them to 'ignore' short-term paper losses and focus on long-term value generation.

Strategic partnerships

A third and very important advantage for the THL sector is that SWFs, particularly those in the Middle East, have the ability to act as a strategic partner for the roll out of brands in the region. In these partnerships SWFs take a stake in the equity of the business and then assist in growing the brands in the region by funding new developments. Dubai World's investments in Kerzner International, followed by their joint venture to develop the recently opened $1.5 billion Atlantis, The Palm, Dubai is an example of such a partnership.

Future prospects

SWFs have become a major force over the past three years, but will this continue? Among the challenges they are likely to face are the implications of increased regulation and the threat of protectionism in the wake of the global credit crunch. There is little doubt that banks, private equity and hedge funds will all face stronger regulation and requirements for greater transparency and it seems unlikely that SWFs will escape similar attention.

A further result of the global economic crisis will be that SWFs will increase their focus on investments 'at home'. This has started in the banking sector with the Kuwait Investment Authority pumping $418 million into the Gulf Bank in January 2009, and is likely to extend to other sectors.

Long-term view

Despite these challenges SWFs are likely to grow more influential still, driven by three overriding factors. Firstly, although the growth of funds available to them may decrease in the short-term as a consequence of the current economic environment, these factors are largely cyclical and when the global economy begins to grow again so will their reserves. Secondly, even though funds have had their fingers burnt by large losses as a result of entering the market too soon, they are unlikely to change their preference for equities over bonds. Their underlying motivations have not changed and are embedded within their DNA. SWFs were created for investment diversification and long-term value generation and a few bad years will not change this, especially in the Middle East where their conversion of oil wealth to diversified financial wealth will certainly continue.

Thirdly, and most importantly, SWFs are able to take a long-term view of their investments. Combined with their superior liquidity this will allow them to seize opportunities that private or institutional investors may not have the funding to access. In coming years they will be able to use their built up reserves to capitalise on assets trading at significant discounts due to current market conditions.

Sovereign wealth funds are here to stay and are likely to become increasingly powerful players. However, their focus will tend towards domestic investments while the economic downturn remains a threat to their national investments. Nonetheless, they will still be ready to quickly capitalise on sound international opportunities. The THL sector ultimately remains a global business with tremendous potential both abroad and at home. SWFs will continue to invest.

Although some states and Emirates are now well developed in tourism terms, others are just starting. This means there is still considerable scope for expansion and diversifying into new target markets.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.