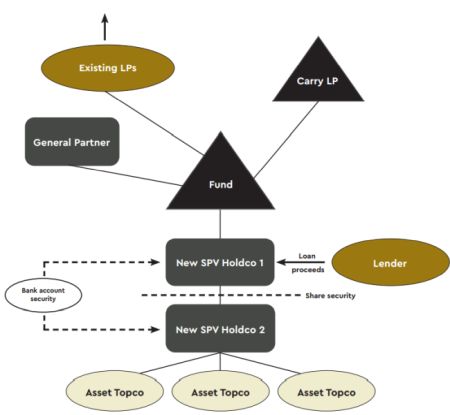

NAV backed leverage involves fund level borrowing against the net asset value of the portfolio

Key points

- Lender provides cash via a NAV facility which is used to satisfy the transaction objectives including providing working capital for the portfolio assets or accelerating liquidity for existing LPs.

- Typically a double newco stack is required/preferable to give the lender a cleanco over which it holds its share security. Otherwise, existing fund structure remains in place.

- Avoids granting direct security over each asset topco which:

- can be complex where there are also management/coinvestors at that level; and

- can be expensive and time consuming where this would require security to be granted in multiple jurisdictions.

- Avoids the Fund being a party to any finance documents which

can avoid:

- triggering any relevant LPA restrictions, leverage caps etc;

- the need for any consents from any subscription line lender at Fund level; and

- triggering strict requirements under the Fund documents for LP/LPAC consents.

- Underlying investment/equity documents to be checked carefully for any relevant transfer restrictions.

- Tax structuring relevant to the transfer of assets and tax treatment of Limited Partners (often Holdcos set up as limited partnerships).

Key economic terms and negotiation points

Economic terms

1. Quantum

- 15-30% of day one LTV typically (depending on asset quality, diversification and asset class).

2. Facility structure

- Single or multi-draw term facility usually. Typically single currency

3. Margin

- Typically 400-700 bps but will depend on asset profile, asset class, diversification, provider and if debt can be rated.

- Customarily subject to an LTV-linked margin ratchet usually with 3-4 steps of 25-50 bps.

4. Fees

- Arrangement/upfront fees - typically 1-2% of total commitment.

- Commitment fee - typically 1-2% of available commitments.

- Prepayment/make-whole - usually make whole for first 1-2 years.

5. Tenor

- Typically 2-5 years, often subject to uncommitted extension option.

6. Cash sweep

- Will depend on modelled exit/distribution profile, but typically will include LTV-linked sweep of distributions received from investments in mandatory prepayment of the Facility.

7. Financial covenants

- LTV (i.e. ratio of financial indebtedness to aggregate Eligible NAV - usually set as 25-35% (depending on opening LTV).

- Value covenant - possibly also included.

- Minimum number of Eligible Investments - possibly also required.

Negotiation points

1. Eligible investments/Eligible NAV

- Range of "Material Investment Events" will

trigger removal of assets from the borrowing base/Eligible NAV

calculation typically including:

- lock-up events;

- material EoDs under asset level debt docs;

- insolvency of underlying Opcos;

- failure to deliver financial statements;

- repudiation/unlawfulness of underlying investment docs; and

- audit qualification in respect of underlying Opcos.

2. Valuations

- Lender right of valuation challenge - use of third party valuations, responsibility for valuation costs, frequency of challenge rights.

3. Sweep mechanics

- Ability to net off fees/costs/expenses and taxes.

- Timing for sweep payments.

- Sweep levels when different number of Eligible Investments held and post EoD/material EoD etc.

4. Covenant breach/LTV triggers

- Consequences of breaching covenanted LTV - typically triggers a grace period during which a Liquidity Plan must be developed to ensure mandatory prepayment below covenanted maintenance LTV level within 3-6 months.

5. Reporting

- Annual and quarterly accounts of Fund, Obligors and Investments plus quarterly reports provided to LPs.

- Notification of Material Investment Events.

- Lender ability to request information on underlying investments.

Our secondaries platform

Travers Smith has extensive experience in complex private markets transactions, with a focus on liquidity solutions across the private markets capital structure with exposure across all asset classes.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.