This year we have witnessed a significant rise in interest rates to levels not seen since 2009. This is being perceived as a tailwind for private debt funds as they lend at floating rates and, therefore, benefit from higher interest payments when rates rise. In turn, the appropriateness of current hurdle rates is under question as investors view them as "too achievable".

The first part of this two-article series will provide the background on hurdles and explore the arguments for and against increasing them. The second edition (to be published late September) will cover potential alternatives that can help align GP and LP interests, such as floating hurdles and catchups.

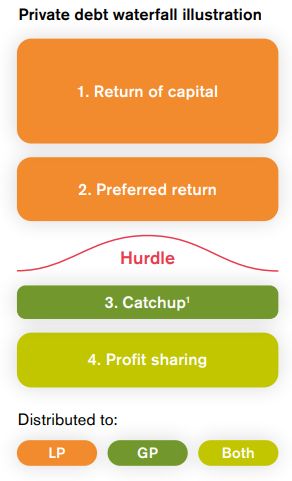

The importance of hurdles

Hurdle rates, often referred to as preferred returns, set the minimum return required before GPs can start sharing in the profits with LPs. For example, if a fund has a 6% hurdle the GP will only receive any carry if the fund's returns exceed this value i.e., after the LP has received its preferred return. Hurdles are an essential tool in aligning GP and LP interests as they prevent GPs from setting unrealistic return expectations and provide a layer of protection to LPs when profits are underwhelming.

Hurdle rates are a standard feature in almost all buyout and private debt funds, although they are less common in venture capital. The chosen rates vary according to the asset class and the individual strategy of the fund. Funds with a higher risk-return profile will typically have a higher hurdle. Broadly speaking, the target return should inform the hurdle rate so that the GP is incentivised to achieve the advertised return.

If a fund has a "hard" hurdle, also called "true" preferred return, the GP's carry will be calculated solely on the profits that exceed the hurdle. On the other hand, "soft" hurdles allow the GP to receive carry on the entirety of the profits (if the hurdle is met). Soft hurdles are more common within private equity and private debt funds, these funds often use catchups to allow GPs to reach the agreed profit-split.

Note on catchups

The catch-up period starts after returns reach the defined hurdle rate. The GP then enters a catch-up period, in which it receives a higher percentage of the profits until the profit split determined by the carried interest agreement is reached. The impact of catchups on GP incentives is that it requires a higher rate of return for the GP to get to full carry. Catchups will be discussed in greater depth in the next edition of this mini-series.

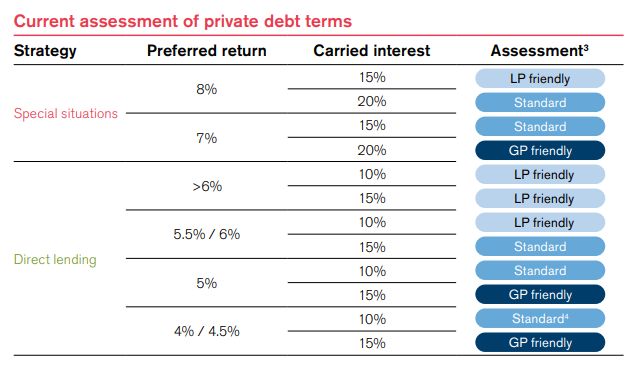

Typical hurdle rates for private debt funds

The table below illustrates the typical hurdle rates our private capital practice currently sees across senior direct lending and special situations funds.

Due to the lower return profile, hurdle rates for direct lending are more nuanced than those for special situations with differences in the range of 50 basis points being common. Typically, hurdles for direct lending are in the 5% to 6% range.

The arguments for increasing hurdles

For the past ten years up until 2022, interest rates in the UK and particularly in Europe have been close to 0%. During this period, European private debt, in particular direct lending, grew substantially and found its way into the target asset allocations of many of the world's largest institutional investors. Consequently, most direct lending funds active today have never operated in a high interest rate environment and fund terms, including hurdles, have not been stress tested.

Given the rise in interest rates - currently at 5.25% for the Bank of England and 4.25% for the European Central Bank - some LPs are exerting pressure on fund managers to adapt fund terms to reflect these market changes. Two key tailwinds are often mentioned:

- Increased interest returns: Direct lending

investments typically have floating rate coupons with interest

rates normally quoted as a spread above a reference rate, such as

SOFR2. As reference rates increase, private debt funds

should receive higher interest payments.

- Increased negotiation power: As capital is becoming more limited, the market has tipped in the lenders' favour. There are opportunities for strong riskadjusted returns with lower leverage and documentation that is more lender-friendly.

The arguments against increasing hurdles

Given the long-term nature of private debt funds (seven to ten years) it can be argued that, during the lifetime of a fund, fund managers will experience a variety of conditions with some years being more favourable than others. This view would suggest that hurdles should only be affected by systematic market changes, not by temporary ones. Uncertainty regarding interest rate behaviour in the long term creates a risk whereby if rates come down further than expected, managers will face hurdles that are too high, which may incentivise excessive risk taking.

Other views against increasing hurdles are that the tailwinds mentioned above are offset by other market conditions that create challenges for fund managers, namely the following:

- Expected increase in defaults: In May 2023,

Fitch Ratings increased the highyield (HY) bond default rate by

1.5%. The HY default rate in Europe is expected to continue to

increase in the coming years creating a scenario where interest

rates will start to decline whilst defaults increase. Pre-existing

loans are expected to have a higher risk of default than newly

issued ones, still, new issuances will also be impacted by

worsening macroeconomic conditions.

- Deal volume: Current market conditions have seen global PE/VC deal volume decrease by 49%5. Simultaneously, the rising cost of debt has led private equity firms to reduce leverage in buyouts. As most private debt deals are backed by PE sponsors, this adds complexity to deal sourcing and impacts management fees both due to the increased operational complexity and the fact that management fees for private debt funds are usually paid on invested capital rather than on committed capital.

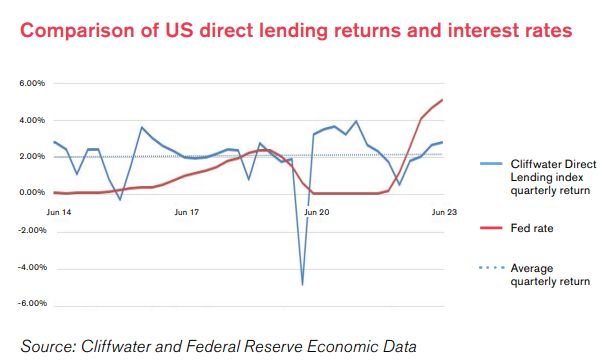

Another consideration is the actual return in direct lending and its correlation to higher interest rates over the past ten years. For this analysis, the US is a useful data source, as it has experienced higher interest rate variations in this period. The graph below shows a comparison of the US FED rate against the quarterly performance of the Cliffwater Direct Lending Index (CDLI)6, which provides performance data on direct lending loans originated by Business Development Companies (BDCs). This comparison suggests that, over the period analysed, there was no significant correlation between these two indicators. A potential explanation is that middle-market direct lending loans are neutral to duration risk (due to their floating rate) and are mostly impacted by their exposure to credit risk.

Additionally, if a linear relationship between private debt hurdles and interest rates existed, that would presuppose that hurdles in the US should be higher than those in Europe as both currently and during the 2017 to 2020 period, US interest rates were up to 2% higher than those in Europe. However, there has been no significant difference in hurdle rates between US and European funds with similar strategies.

Note: the CDLI tracks loans originated by both unlisted and exchange-traded BDCs which are close-ended funds often used to give retail investors access to private markets. As such, the CDLI is expected to have a higher correlation to the broader stock market than private debt funds.

What we see in practice

When analysing funds launching in 2023, we see little variation in hurdles within the same fund series. Mostly, we find that discussions on alignment of interests and manager compensation should be considered holistically. For example, considering other factors such as carried interest and catch-ups. Below are our observations from funds raising in 2023.

- Some managers have already raised their hurdles in 2023 -

mostly those with higher carried interest terms.

- Several direct lending fund managers launching funds in 2023,

including those by new fund managers with potentially less

bargaining power, are still opting for a typical hurdle rate of

5%.

- A slower catchup is being used by some fund managers as an

alternative to increasing preferred returns.

- For funds launching in the second half of 2023 and 2024 we expect to see more managers increasing their hurdles. Where managers are raising hurdles, these are usually up by no more than 50 to 100 basis points.

Key takeaways

- The relationship between interest rates and private debt

returns is not linear. The current interest rate environment

presents tailwinds for lenders such as higher credit spreads, lower

leverage, and stronger documentation. However, these are also

offset by headwinds such as a potential increase in technical and

actual defaults and more limited deal flow.

- Although there is some pressure from investors to increase

hurdles, so far, only a few managers have opted for this

approach.

- Hurdles should not be analysed in a silo, but rather in combination with other waterfall features such as carried interest and catchup. Managers should see if their terms as a whole are too GP-friendly. If so, they can expect to face more pressure from LPs to increase hurdle rates.

Footnotes

1. Illustrates a 100% catchup.

2. Secured Overnight Financing Rate.

3. This is a simplified assessment; the suitability of preferred returns and carry rates should also be compared against a fund's target return.

4. This model is becoming less common in current vintages.

5. From Q1 2022 to Q1 2023 according to S&P Global.

6. The CDLI covers approximately 13,000 directly originated middle market loans totalling $276bn as of 31 March 2023. The index seeks to measure the unlevered, gross of fee performance of US middle market corporate loans, as represented by the asset-weighted performance of the underlying assets of Business Development Companies that satisfy certain eligibility criteria.

7. Corporate default rate forecast according to Fitch Ratings on December 2022.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.