Builders' merchants and DIY retailers across Europe face ongoing market turbulence, as unstable demand, inflation and overstocks create a challenging outlook for the sector. As inflation and the lockdown-induced demand surge have eased, many merchants and retailers have been left with a need to address underlying volume decline, inventory hangovers and weakening profitability.

The complexity of operating within the market continues to intensify. Alongside inflationary pressures – including increased materials, labour, utilities and product costs over the past 18 months – deflation is emerging in some categories, including in Chinese manufacturing. Shipping rates, meanwhile, remain volatile. Following a period of extreme inflation and then deflation, the Red Sea shipping crisis has now driven rates from Asia to North Europe to a 14-month high.

Fluctuating demand remains a challenge for the sector. Cost inflation had – until now – helped retain market value and offset volume declines, but now lower levels of inflation, and emerging deflation in some areas, have led to market value decline.

Consumer demand for housebuilding and renovations weakened throughout 2023, heavily affected by the pressure on consumer finances and the impact of interest rates. UK residential transactions were down 18% YoY at the end of 2023, although the outlook now appears somewhat more positive, as a growing sentiment that interest rates have peaked has resulted in UK mortgage rates easing in recent weeks. Revised inflation outlooks in early January suggest that the Consumer Price Index (CPI) will fall below 2% within 4 months, and may trigger earlier interest rate cuts, with a projected year-end position down 1% to 4.25%.

In parallel, major infrastructure delays and cancellations, including HS2 delays in the UK, have greatly disrupted capacity levels in some heavy materials markets such as cement – the impacts of which are still playing out.

What does this mean for builders' merchants and DIY retailers?

While there may be a short-term improvement in inflation and interest rates, rates overall remain higher than in recent history, and consumer finances are stretched. Big ticket and discretionary spend will therefore continue to be subdued, and DIY share will remain firm vs Do-It-For-Me (DIFM). Consumers will remain value-driven, and competition will be high, so both value perception and reality will be critical in pricing and promotional strategies.

Merchants will require supply chain agility, to manage a more complex demand mix and establish greater control of inventories. Profitability will remain a challenge, and increasingly sophisticated, data-driven approaches will be necessary to ensure that every margin opportunity can be captured.

What practical steps can merchants and retailers take?

Retailers should begin by asking some key questions:

- Is our product range clearly aligned to our latest business strategy and the evolving needs of our customers? Are we presenting a differentiated and profitable product and service proposition?

- How can we balance the competing challenges of sales and share growth, margin growth, inventory and cash generation? Which is most important?

- What are the real drivers of true net margin? Which productivity and margin levers will provide the greatest return, mindful of unstable demand?

- How well-aligned is our supply base to our strategy? Have we revisited supplier terms, and do we have an accurate view of what we should now be paying?

Based on our work with leading companies, we recommend four pillars for transforming profitability through commercial strategy, margin optimisation, and sourcing.

1. Build strong foundations through productive ranges

Realign category strategies to shifts in business

strategy

Consider how customer needs have changed, and what relevant trends

mean for your product or service offer. Government schemes like the

UK Boiler Upgrade Scheme continue to drive demand across renewable

energy categories, while the continued focus on sustainability is

driving longer-term demand for greener products and construction

methods, such as in timber-based construction.

Identify which categories are forecast to grow and how well positioned you are to win. Define the subset of categories that require the most focus and investment (e.g., in innovation, range, store or branch presence, online or service proposition) to build share and sustain profits, and where you should now reduce, or exit.

Create a true net margin view of profitability at SKU

level

Calculating true net margin requires a SKU-level allocation of all

significant costs, creating an end-to-end view of profitability

drivers along all key dimensions, including brand, supplier, store

cluster, and customer segment. Relying on gross margin is not

sufficient, given the varying impacts of drivers such as customer

discounting, supplier terms, handling costs, return rates, and

quality.

Build accessible data insights to diagnose the

opportunity

Present granular insights in user-friendly, customisable

dashboards to enable decision-makers to answer key questions. For

example:

- What is driving category performance and order or basket performance, and how does this vary by customer segment?

- How are customer shopping patterns changing, including frequency, basket size, and cross-shop? Are new versus existing customer metrics healthy?

- Where is customer discounting undermining profitability, and where is this working effectively?

- What is driving net margin growth versus dilution, at category, sub-category, supplier, or item level? Which customer, channel, demand- and supply-side levers will drive the next wave of margin improvement?

- How have inflation and re-pricing impacted the business over time? In the B2B market especially, we see that price increases in commoditised markets often do not land fully with customers, creating margin dilution over time.

Challenge breadth of range and fulfilment

models

Many builders' merchants and DIY retailers have pursued a

strategy of bold range expansion, to extend into white space and

deliver against unmet customer needs. All too often, however, we

find that core disciplines in range design have been lost. Coupled

with the increased organisational complexity and recent inventory

gluts, a holistic review of range breadth is now advisable, and

rationalising ranges may be justified. This includes validating all

required assortment areas (e.g., stocked, extended, and

marketplace), and conducting an in-depth review of the customer

benefits and net margin, given varying cost-to-serve for each

fulfilment model.

2. Re-establish pricing and discounting discipline

A broad product mix, and a blend of trade and retail customers, create a challenging pricing dynamic in DIY and building markets. Maintaining rigorous pricing processes has a strong payback on the bottom line and on customer perception. Common pitfalls quickly undermine net returns, particularly when there is weaker data and dispersed accountability, including:

- Price-setting without an understanding of how price-sensitive the customer is, or without an up-to-date view of competitor pricing

- Weak control of discounting and markdowns in branches, driving a disconnect between customer value and the discount given

- Sales in branch lacking focus on maximising customer value and share of wallet

- Limited reporting of promotional effectiveness, to measure return on investment

- A lack of margin transparency at the customer or SKU level, both vitally underpinning the commercial process

- Surcharges not applied or enforced in branch when applicable

- Sub-optimal freight cost recovery for delivered products

By introducing agile pricing frameworks, businesses can navigate the balance of capturing customer demand, while keeping a sharp eye on competitors and maintaining the maximum return.

3. Effective sourcing strategies

A disrupted market presents an opportunity to reinvigorate your own sourcing processes. Now is a good time to reassess and challenge your supply base. The key tools in your arsenal should include:

- "Should cost" modelling

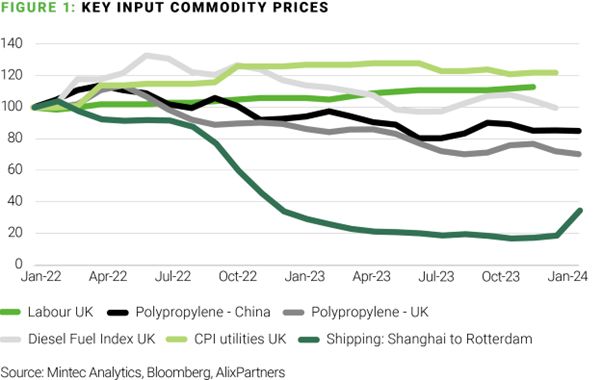

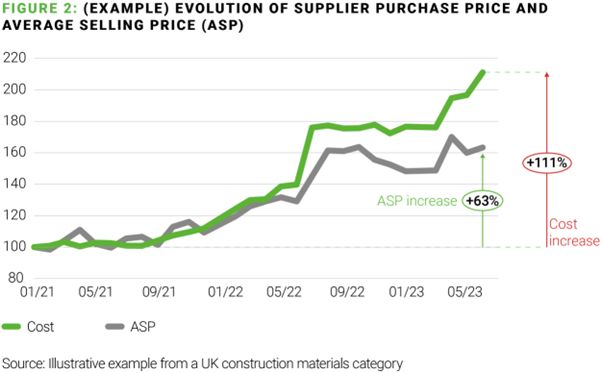

Create or update models of all main product groups, reflecting the key cost components within the finished product. Use key commodity indices to model how finished goods costs should have evolved over time, incorporating other sources of supplier funding to compare with how they have tracked. Focus on directional trends and the most significant relative movements, to guide efforts and anticipate future trends.

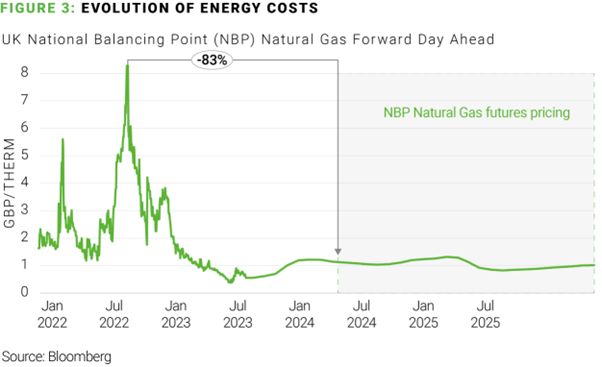

Consider supply-side dynamics, such as contrasts in shipping and energy costs between far- and near-sourcing where possible, including forward-looking views. Energy pricing, for example, has shown historic volatility, so futures pricing is an important element of your negotiation (see figure 3). Use data-driven insights to get ahead of the curve, and be proactive in speaking with key suppliers before your competitors do.

- Assessing the level of category

opportunity

How commoditised are the categories under review? For true commodity products, where pricing is defined by the supply market, identify where you need to differentiate to gain competitive advantage, and how you can offer further value to customers.

Where does the balance of power with the supplier sit? What proportion of your key suppliers' revenues do you currently account for, and what is the potential?

- Deploying the best sourcing approach

-

- Direct vendor negotiations typically offer the quickest results, and with the lowest risk. Share relevant data insights with suppliers, and ensure any negotiations are robust and data-backed. Build a robust view, and be transparent with suppliers about alternative options.

- Tendering is a more intensive and structured process, however, when supported with robust SKU-level specifications, can offer greater benefit where there are credible alternative suppliers.

4. Landing the change

To land your changes effectively to the bottom line, we recommend:

- Embedding sustainable capabilities across your

organisation

Create an end-to-end view of product and category, and build inflation- or index-tracking into your operating model. Develop user-friendly interfaces, and pilot dashboards with relevant teams to increase engagement. Structured training and on-the-job coaching will ensure that new insights translate into sustainable, margin-enhancing capabilities. - Extending this approach to your supply

base

Build or reintroduce appropriate inflation-linked mechanisms into key contracts. Embed visibility of end-to-end profitability as part of your Quarterly Business Review process, and enable suppliers to collaborate with you on solving your margin challenges. - Driving cultural buy-in

Build a robust, top-down process of capturing heads, hearts, and hands. Ensure the business, and especially branch teams, understand and embrace the programme and target outcomes to avoid benefit dilution. Consider incentivising category teams on an end-to-end profit basis to drive accountability for bottom-line performance.

Conclusion

The market outlook for builders' merchants and DIY retailers remains challenging, and all players must evolve their capabilities to manage through ongoing disruption.

The inherent complexity of navigating continuous change requires significant organisational effort. A refreshed view of strategy and proposition, alongside a ruthless focus on end-to-end category profitability, will ensure the right business actions are prioritised, and both customer and business objectives can be delivered.

Merchants will require supply chain agility, to manage a more complex demand mix and establish greater control of inventories. Profitability will remain a challenge, and increasingly sophisticated, data-driven approaches will be necessary to ensure that every margin opportunity can be captured.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.