The Information Commissioner's Office ("ICO") has recently issued technical guidance, entitled "Data Protection Technical Guidance: Determining what is personal data" ("the Guidance") for data protection purposes. It will assist in determining whether data falls within the definition of "personal data" when responding to subject access requests. In addition, it impacts on how employers comply with their obligations when processing employees' personal data.

Although the Guidance is not legally binding, it represents the Information Commissioner's view on what amounts to personal data for the purposes of the Data Protection Act 1998 (the "Act") and should therefore be highly persuasive to the interpretation of personal data by the courts.

The Interpretation Of Personal Data Before The Guidance

Under the Act, personal data is defined as data that relates to a living individual who can be identified from that data, whether alone or together with other information that is in the possession of, or is likely to come into the possession of, the data controller. Following the introduction of the Act, this definition was given a broad interpretation which presented particular problems for employers responding to subject access requests given that this right of access for employees extends to all personal data processed by their employer.

In Durant v Financial Services Authority (2003), the Court of Appeal considered, in relation to a subject access request by Mr Durant, whether certain documents held by the Financial Services Authority contained personal data. The Court of Appeal approached this on the basis that personal data must "relate to" a particular individual. It found that data will only relate to an individual where it is "...information that affects privacy, whether in his personal or family life, business or professional capacity". This decision was welcomed by employers since it reduced the scope of documents to be disclosed, in responding to a subject access request.

The Interpretation Of Personal Data Under The Guidance

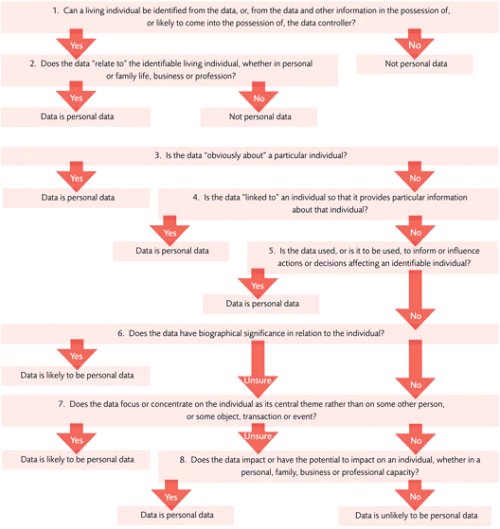

In the vast majority of cases, it will be obvious whether particular data amounts to personal data. The Guidance sets out a series of questions to assist in determining whether data amounts to personal data, in cases where this is not obvious. These questions are set out in the flow-chart below. The eight questions should be addressed in the order set out in the flow-chart.

Question 1

This question focuses on the identification of a person from particular data. It should be approached from the perspective of the potential identifier, taking into account the context in which the data appears. Where no name is given, an individual may be identified from a combination of data about his age, gender, grade or salary. If there are no reasonable means of identifying an individual from the data, the information will not amount to personal data. The Guidance suggests that the threshold for deciding whether an individual can be identified from the data is a low one.

Question 2

This question deals with whether the data "relates to" an identifiable person - whether in personal or family life, business or profession.

Questions 3-8

These questions cover a broad range of issues to assist with assessing question 2, as to

- whether the data is "obviously about" a particular individual;

- whether the data is "linked to" a particular individual;

- the purpose of processing the data;

- whether the data has any biographical significance;

- the focus of the data, i.e. whether it is centred on the particular individual; and

- the central impact the data will have on an individual.

Cumulatively, the effect of questions 3-8 is that data controllers are required to adopt a broader approach to what amounts to personal data than is stated in Durant. It is clear from the Guidance that the mere possibility of a connection between certain information and an individual may be sufficient to bring the information within the concept of personal data.

It will only be necessary to consider biographical significance (question 6) where the information is not clearly about, or linked to, the individual. An example which the Guidance gives of biographical significance is if the individual is listed as an attendee in meeting notes because it is a record of the individual's whereabouts at a particular time, and therefore amounts to personal data.

The Guidance states that where individuals express views in their capacity as employees, the views themselves will not amount to personal data. However, in some instances, it may be difficult to draw this distinction where, for example, an individual is expressing views on the culpability of a fellow employee when appearing as a witness as part of a disciplinary investigation.

Disclosure Requirements

The Guidance makes it clear that an individual's personal data may be limited to a small section of a document. In these circumstances, to comply with its obligations, an employer is only obliged to disclose relevant extracts of documents to the extent that the document relates to the individual. For example, where meeting notes record a conversation in which a number of possible candidates are considered for promotion, only the section which relates to a particular candidate is that individual's personal data, and therefore discloseable. Likewise, the Guidance makes it clear that, where meeting notes only refer to the individual in the list of attendees, only this section of the meeting note will amount to personal data.

Conclusion

There was some disquiet, albeit not from employers, following the Court of Appeal's decision in Durant that the scope of personal data was too narrow and was not in keeping with the general understanding of what personal data encompassed. In view of this, it is not surprising that the concept of personal data has been widened by the Guidance. Employers should refer to the Guidance when responding to a subject access request, and be mindful of the extended scope of personal data. Employers can, however, take comfort from the fact that the Guidance supports a pragmatic approach to information which does not focus on the individual.

Employers should also be mindful of the Guidance's interpretation of personal data in the context of processing employees' data.

The ICO states that it will soon be producing new guidance on the meaning of "relevant filing system" which, we anticipate, may further broaden the scope of data to be considered when responding to a subject access request.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.