EXECUTIVE SUMMARY

There is much diversity in accounting for extractive industries under International Financial Reporting Standards (IFRS). Terminology is inconsistent, treatments vary and the requirements of IFRS 6: Exploration for and Evaluation of Mineral Resources permit widely divergent practices on a national and global basis. The draft discussion paper: Extractive Activities, recently released by the International Accounting Standards Board (IASB), seeks to address these concerns and harmonise the accounting between the mining and oil and gas industries.

Whilst the paper ostensibly proposes approaches producing a similar outcome to common industry practice, there are a number of interesting issues and considerations arising from it.

In summary, the discussion paper:

- Proposes to adopt the mineral reserve and resource definitions established by the Committee for Mineral Reserves International Reporting Standards (CRIRSCO): International Reporting Template for the Public Reporting of Exploration Results, Mineral Resources and Mineral Reserves.

- Identifies the legal right to explore and extract as the fundamental basis of a mining asset.

- Recommends measurement on an historical cost basis (i.e., by capitalising exploration, evaluation and development costs) but countenances the possibility of requiring a fair value measurement basis instead.

- Proposes to retain a modified impairment approach to assets in the exploration and evaluation stage.

- Introduces a new asset recognition approach, which largely formalises the policies companies apply in capitalising exploration expenditure, with option to expense seemingly being removed.

- Mandates extensive disclosures for proved, and proved and probable mineral reserves quantities.

- Introduces other disclosures, including a form of standardised value for reserves and possibly responding to the Publish What You Pay proposals.

Whilst a new accounting standard may yet be some way off, the discussion paper is an important first step in a process that could radically change the shape of mining companies' results and balance sheets, and introduce extensive new disclosure requirements for mineral reserves as well as enhance transparency around payments made by mining companies to governments.

The IASB plans to invite comments on the project team's proposals in Q1 2010. Given the significant impact of these proposals – in particular the level of detail communicated to stakeholders, and the considerable practical burden of transitioning to, and then sustaining, the proposed reporting requirements – those who prepare financial statements would be well advised to consider these and ensure their views are heard.

Here we have summarised the draft discussion paper along with our own commentary.

BACKGROUND

In August 2009, the IASB published the research project's draft findings and proposals relating to accounting for extractive industries. These proposals challenge the fundamentals of accounting for activities in the mining industry under IFRS.

Any new standard would replace IFRS 6 which was always intended by the IASB to be a temporary solution, and will bring an end to the flexibility the existing accounting standard affords mining companies.

Project Timeline

ASSET MEASUREMENT

A key consideration was the appropriate basis for recognising and measuring rights associated with mineral and oil and gas properties. Two measurement methods that were deliberated were fair value and historical cost.

Fair Value

The draft paper sets out three possible ways for measuring fair value:

- Market approach – using prices and other information generated in market transactions.

- Cost approach – current replacement cost.

- Income approach – discounted future cash flows.

Market and cost approaches were determined to be unsuitable for mining properties given that each is unique; as a result an income approach was thought to be the most suitable measurement of fair value.

However, those consulted on the benefits of measuring mineral and oil and gas rights at fair value had concerns that the calculations would be costly and time consuming to prepare, whilst providing little benefit to users of financial statements given the wide range of assumptions made and the subjectivity this introduces.

In addition, measuring assets at fair value, whilst consistent with the current trend in IFRS, introduces high levels of volatility into the balance sheet and potentially the income statement.

Historical Cost

The other option considered was measurement at historical cost – as is currently used in the industry to account for mining assets.

It was noted that historical cost provides a verifiable measure of the cost of acquiring, exploring and developing a property, giving an indication of management's historical performance and return on capital employed. However, given the minimal correlation between the cost of exploration and the value of any resulting discovery, the relevance of this measure diminishes over time as subsequent exploration and evaluation generates more information about a property, and as economic conditions change.

The Project Team's View

Having considered the various options it was recommended that a single historical cost approach should be applied, and assets should be subject to depreciation and impairment testing.

However, this is only the view of the project team, and as yet fair value accounting is not entirely off the table.

The research also concludes that historical cost measurement alone would not provide financial information that is sufficiently useful to users, and hence extensive disclosures for mineral reserves are also proposed, based on the reserve and resource definitions as set out in the Committee for Mineral Reserves International Reporting Standards (CRIRSCO) International Reporting Template for the Public Reporting of Exploration Results, Mineral Resources and Mineral Reserves (CRIRSCO template).

HISTORICAL COST ACCOUNTING PROPOSALS

Asset Recognition

Having recommended that the most appropriate measurement basis for mining assets is historical cost, the paper goes further, discussing the application of these principles in the context of the extractive process.

It acknowledges that extractive activities usually begin with the acquisition of legal rights to explore a defined area. This is followed by exploration and evaluation activities which are performed to increase the geological understanding and establish the presence (or otherwise) of mineral reserves in commercial quantities. Over time, this understanding will increase to a point where an assessment can be made as to whether it is economical to develop the deposit.

As a result, the view is that the underlying asset is the legal right (i.e., the licence) and information associated with the mining property is an integral part of this asset. Essentially the exploration licence, geological and geophysical studies and exploratory drilling (whether or not successful) all form part of a combined exploration and evaluation asset based on the legal rights to explore, rather than separate assets.

The proposals may therefore indicate a change in accounting policy for any company which currently expenses exploration costs, as they appear to remove the option to do this, instead indicating that exploration costs would be capitalised as part of the mining asset until and unless the legal rights are derecognised (see consideration of impairment).

Unit Of Account

Also addressed in the draft discussion document, is the definition of a unit of account (i.e., at what level assets would be disaggregated or aggregated for recognition in the financial statements).

The paper identifies two key considerations when determining the unit of account for mining assets:

- Geographical boundaries (e.g., at the property level, individual geological area, or at a country level).

- Components which should be recognised as a single item (e.g., the legal rights or the property, plus any associated plant and equipment assets).

The draft discussion document's view is that for exploration rights, the unit of account would initially be the legal rights held for each exploration property. As the exploration and evaluation activities occur, the unit of account would shrink such that by the time the asset is brought into development and production the geographical boundaries of each unit of account would be no larger than a single prospect, or group of contiguous prospects for which the rights are held, which is managed separately and which generates independent cash flows. Plant and machinery which is dedicated to the mining property would also form part of the unit of account.

A number of practical allocation issues appear to arise in applying this concept (e.g., costs specifically related to the part of the area which is no longer of interest), which the paper does not seek to address in detail.

Depreciation

The paper proposes that existing depreciation rules under IFRS should not change. However, it does recommend that a consistent approach be applied across the extractive industries, but does not go as far as to suggest what this should be. Notably it does not address whether the unit of production calculation should be based on proved or proved plus probable reserves, and indeed questions whether it should be by reference to revenues rather than reserves. This would imply that the existing choice between methods would end, though it does not indicate which method might ultimately prevail.

Given the North American emphasis on proved reserves, and the IASB's emphasis on best estimates, this looks set to become an area of some debate.

Impairment

IAS 36: Impairment of Assets currently applies to extractive activities in the development or production phase and the paper does not recommend any change in this approach. However, it does propose that IAS 36 would be problematic to apply to exploration properties where there is generally insufficient information available to evaluate the exploration results and reach a conclusion on whether it is economical to develop. Therefore some modifications to the generic impairment rules would be needed.

The overall view was that exploration properties should be tested for impairment when evidence is available to suggest that full recovery of the asset is unlikely. Therefore, exploration assets would not be tested for impairment at the reporting date if the necessary evidence was not available or inconclusive, but disclosure should be provided as to why management considers that the carrying amounts of these properties are not impaired.

This represents a subtle but significant relaxation of the IAS 36 requirements, similar to that embedded in IFRS 6 at present.

The paper does indicate that the general requirements of IAS 36 should apply in determining the cash generating units for all impairment tests of mining properties, including exploration and evaluation assets.

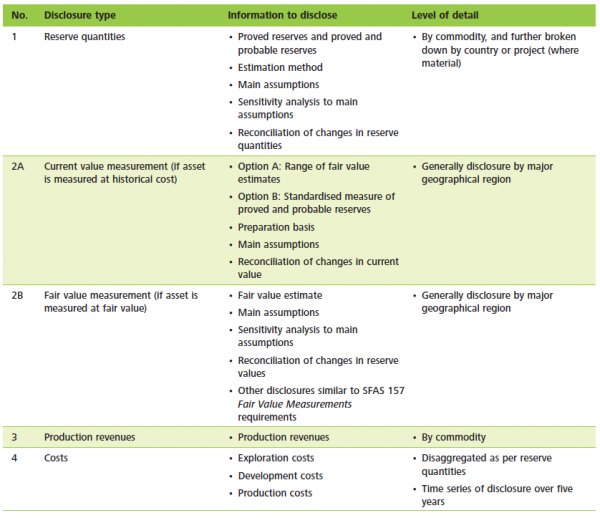

RESERVES QUANTITY AND VALUE DISCLOSURES

The paper acknowledges that the cash flows which result from the extraction of the minerals or oil and gas are the most significant driver of value for upstream operations. Therefore, disclosure of information relating to quantity of reserves is important in enabling users to estimate the value of an entity's minerals or oil and gas properties and the future cash flows that might be generated from those properties.

The project team considered the variety of reserves definitions used by the mining industry, including the SEC definitions. The draft discussion paper recommends adopting the reserve and resource definitions as set out in the CRIRSCO template, the definitions of which are identical to, or materially consistent with, widely adopted reporting codes such as JORC, PERC and SAMREC.

Outlined opposite are the proposed disclosures. Whilst the project team acknowledges these are extensive, it nevertheless regards them as the minimum that should be provided.

Proved vs. Probable

The project team proposes that entities should be required to disclose proved reserves and, separately, the sum of proved and probable reserves, both split by commodity and by country. This would represent an increase in the amount of reserve disclosure provided by many mining entities. This includes all SEC registrants that until recently have been prohibited from disclosing reserve quantities other than proved reserves in their annual reports. A revised SEC rule now permits, but does not require, entities to disclose probable reserves and possible reserves.

Royalties, Taxes, Interests In Mineral Properties And Joint Ventures

The reserves that are attributable to an entity are those quantities of minerals that an entity has the enforceable right to extract. In some jurisdictions, the taxation or royalty arrangements that apply to the production of minerals or oil and gas may be payable in cash or in kind (e.g., the entity may be required to deliver a portion of production quantities direct to the government or royalty owner).

In principle, the project team thinks that all these arrangements should be consistently accounted for. Consequently each type of payment should be treated as an expense of the entity regardless of whether the cost is denominated in cash or in kind. As such, the financial statements should present production revenues and the tax or royalty expenses separately – and consistent with this, the underlying reserve quantities that are controlled by the entity should be included in the reserve quantities disclosed by the entity.

Reserves held by equity or cost accounted investees should not be included as part of those quantities (but might be separately disclosed). Therefore, the IASB's proposals to disallow proportional consolidation of joint venture entities could have significant implications for an entity's reserves quantity disclosures under the project team's proposals, because the reserves attributable to a share in a joint venture could not be attributed to the reporting entity.

Audit Of Reserves Estimates

The paper notes that national regulators often determine whether reserves estimates must be prepared or reviewed by a 'reserves auditor' or equivalent. However, it does not address the practical and capacity issues that could arise from a broader requirement for the certification or independent audit of reserves estimates.

The paper does not explicitly address whether or not the proposed disclosures would be within the scope of the audit opinion on a set of financial statements, which appears to be a natural question if the disclosures are to appear within the annual report and the requirements are to be embodied within IFRS.

Price Assumptions

The paper notes that the basis to be used for selecting a commodity price assumption for estimating reserves quantities is particularly contentious, with the following alternatives being commonly proposed:

- Market participant assumption.

- Management's own expectations.

- Historical price such as the year-end spot price or an average of past spot prices.

The trade off is between consistency and comparability and the relevance of the estimates on a forward-looking basis. On balance, the project team's view is that faithful representation of reserves estimates requires the use of forecast prices, and that the use of historical prices risks misrepresenting the reserve quantities whenever the historical price is not consistent with expected future prices, particularly in the context of the often volatile commodity markets. The project team proposes that the pricing assumptions used in estimating reserve quantities should be disclosed.

Sensitivities

The project team recommends that a sensitivity analysis disclosure should be provided to show the sensitivity of the reserves quantity estimate to changes in the main economic assumptions. They expect that, at a minimum, the sensitivity analysis would be based on changes to the price assumption. However, sometimes a reserves estimate will be more sensitive to changes in other economic assumptions (such as development, operating costs or exchange rates), in which case the sensitivity should be based on changes in those assumptions.

The project team also acknowledges that changes in the commodity price assumptions could have various impacts on the assumptions made, (e.g., about development and production costs as a result of property-specific factors, such as the optimal extraction method or indeed whether or not to proceed with a development at all).

The paper recommends that the sensitivity analysis should take into account the impact of changes an entity should be able to reasonably anticipate and quantify, without requiring a detailed reassessment of all components of the reserves estimate. It seems likely that this could give rise to significant issues in practice, for example where a particular development is highly material to an entity's reserves.

Value Disclosures

On the premise that assets would be recognised at historic cost, the paper recommends standardised value disclosures, in addition to volumetric disclosures. The rationale is that users familiar with the disclosure of the standardised measure have indicated that it can provide useful information, notwithstanding that the value itself may not be useful.

This approach is similar to that already mandated in the US, except that the project team recommends the disclosures be applied to proved plus probable reserves, rather than just proved reserves.

PUBLISH WHAT YOU PAY PROPOSALS

Also included in the paper is a chapter addressing the Publish What You Pay proposals, which are being promoted by a coalition of non-governmental organisations. The disclosures proposed overlap to a large extent with those outlined in the draft discussion paper, with the exception of payments to governments. There is no recommendation as to whether such disclosures should be included in financial reports or not, although it does outline the view that disclosure of payments to governments would be useful to some capital providers, but may be difficult or costly to prepare for some entities, and could be commercially or contractually sensitive in some circumstances.

CLOSING REMARKS

History has shown that views expressed early in the life of an IASB project are the most influential, before a momentum builds towards a particular outcome.

This is particularly so in this case, because the unusual circumstances surrounding the draft discussion paper mean the IASB has not yet formulated its own views and may decided to propose a different approach (e.g., the use of fair value accounting for mining properties).

Given the significant impact of the proposals – in particular the level of detail that will need to be communicated to stakeholders and the considerable practical burden of transitioning to, and then sustaining, the proposed reporting requirements – those who prepare financial statements would be well advised to consider the proposals and ensure their views are heard.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.