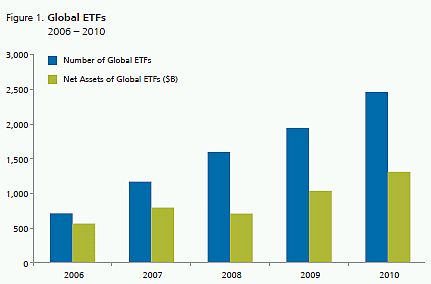

Exchange-traded fund (ETF) strategies continue to increase in scope, involving active management and more sophisticated financial instruments. Furthermore, the size of the ETF market has more than tripled by number of ETFs, and more than doubled by net dollar value of assets, over the past four years:

Notes and Sources: Data are from

BlackRock's ETF Landscape Industry Review, End of Q12011

available online at http://www.blackrockinternational.com/content/groups/internationalsite

/documents/literature/etfl_industryreview_q111.pdf.

The increasing flexibility and versatility of ETFs have been accompanied by claims by regulators and others of destabilizing effects on markets and potential for abuse by market professionals. Moreover, the suitability of ETFs for retail investors and even institutions has become a source of greater concern. We briefly outline several recent ETF issues and follow with an overview of future issues that may impact the growth of ETFs and their regulation.

Recent Issues

Unauthorized Trading

Attention has focused on ETFs as a result of the recently disclosed rogue-trading scandal at UBS, the losses from which are estimated by the bank at $2.3 billion. The alleged rogue trader, Kweku Adoboli, held the position "Director of ETF and Delta1 Trading." The trades that lost money for UBS do not appear to have involved ETFs, but rather were long positions in index futures on the S&P 500, DAX, and EuroStoxx indices. However, according to UBS, Adoboli booked "fictitious, forward-settling, cash ETF positions" to give the appearance that the positions taken in index futures were hedged, and that he was staying within risk limits prohibiting unhedged, speculative positions. In Europe, settlement of ETF trades is sometimes delayed beyond the standard three-trading-day lag after the trade date, and some banks do not confirm trades until settlement—facts that Mr. Adoboli, who had previously held a back-office position at UBS, may have exploited.

Insider Trading

Insider trading involving ETFs is an increasing point of focus for regulators. Front-running, one form of insider trading, is based on non-public information about order flow by authorized participant or institutions. Recently, a former Goldman Sachs trader was accused of taking long and short positions in the underlying securities held by an ETF prior to large executions. Also of concern for regulators is "ETF stripping," wherein a trader with non-public information purchases (or sells short) an ETF representing an index of securities, and then shorts (or buys) all of its constituents except the one about which he or she has non-public information, amounting to a disguised position in a single security. This is a modern day variant of index stripping, an older strategy employed using stock indexes. These strategies will increase in sophistication along with increased ETF trading and product offerings.

Excessive Market Volatility

ETF trading received attention during the so-called "flash crash" in May 2010. In that episode, the Dow Jones Industrial Average dropped by more than 600 points within five minutes, only to recover most of this decline over the next half-hour. During this period, some ETFs lost all their value, dropping to a penny per share, before experiencing a rebound. Due to a number of factors including potential busted trades, competing technology, the specific order type placed by investors (stop loss), and regulatory constraints, quotes became erratic or non-existent. Expanding worldwide securities markets, increasingly sophisticated technology, and broader use of ETF products will likely lead to future bouts of pricing disconnect and volatility in the ETF market

Derivatives

A series of securities class action lawsuits were filed against issuers of leveraged and inverse ETFs—financial instruments designed to provide returns equal to multiples (or inverse multiples) of daily returns on various benchmark indices. The lawsuits alleged that the effect of compounding over periods of more than one day could lead to investment gains or losses different from what some investors would expect. The class action lawsuits followed SEC and FINRA warnings (based on suitability) regarding the same return characteristics for these instruments.

These actions have highlighted the importance of prospectus disclosure. In addition, recent reports of an SEC investigation on the impact of leveraged ETFs on market volatility demonstrate that ETFs that incorporate derivatives into their strategy may receive additional regulatory scrutiny or be subject to greater litigation risk.

Future Issues

Active Management

A small number of actively managed ETFs have been available for several years. Recently there have been filings with regulators seeking approval for new actively managed ETFs by several large banks and institutions. Unlike an index or passive ETF, an actively managed ETF relies on a proprietary investing or trading strategy, so issuers of such instruments have a interest in avoiding full public disclosure. The ability to maintain a proprietary trading strategy while depending on some level of market transparency (and trading by authorized participants) to maintain a "reasonable" premium or discount has been one of the primary roadblocks to creating actively managed ETFs.

Synthetic ETFs

In Europe, synthetic ETFs now account for approximately 45% of ETF assets under management.1 In a synthetic ETF, the authorized participant enters into a swap agreement with a counterparty, typically an investment bank that agrees to provide the return of the reference index in exchange for the performance of the securities held by the ETF. This reduces the tracking error associated with physical ETFs, but introduces other risks, most notably the risk that the counterparty may be unable to pay the index return.

Moreover, institutions such as the Bank for International Settlements, the International Monetary Fund, and the Financial Stability Board have expressed concern about systemic risks potentially posed by synthetic ETFs. For example, if a counterparty bank finances illiquid assets through swap payments received from authorized parties under synthetic ETFs, there is a liquidity mismatch between the bank's short-term liabilities and the longer-term funding, which could be a systemic threat if there were a sudden, widespread liquidation of ETFs. The IMF has also voiced concern about possible distortion of and volatility in the prices of commodities, particularly gold, as a result of the large funds flowing into and out of commodity-based ETFs.

NAV Premiums and Discounts

The foundation of ETF trading is the market-driven arbitrage mechanism between the ETF share price and the price of the underlying securities. If the arbitrage system falters, potentially due to correlated risk aversion by authorized participants, the magnitude of the price disparity could widen. How retail and other investors would react to the premium or discount component to price changes will be of interest. In particular, high premiums or discounts in ETF trading values relative to NAVs during periods of market turmoil highlight the challenges that ETFs may face in delivering liquidity when it is needed most.

Securities Lending

Securities lending is a significant generator of income to ETF managers and investors. Most investors are unaware of the existence of securities lending or the implicit role it plays in the market. Many economists argue, and regulators recognize, that a liquid securities lending market (enabling short selling) is an essential factor for efficient markets. However, short selling has also received blame as the cause of market inefficiency by regulators and corporate leaders. Increasingly, discussion of the risk of collateral investment loss and issues surrounding the transparency of lending utilization, fees, tax consequences, and counterparty risk has been relevant to investment management regulators and investors. There may be operational issues particular to the ETF market in settling short sale transactions.

Commodities

Regulatory constraints—specifically position limits—continue to be a main issue for commodity ETFs (commodity exchange-traded notes). CFTC rules that limit the amount of derivative contracts used to gain exposure to commodities can cause unexpected tracking errors. Some predict that if position limits impede the growth and efficiency of commodity ETFs, managers will turn to other financial products, limit the size of their funds, or diversify their holdings to get under the limits.

Footnote

1 In the European market as of Q1 2011, there were 714 synthetic ETFs with $138.0 billion in AUM, out of a total of 1,122 managing $307.5 billion. See: BlackRock's ETF Landscape Industry Review, End of Q12011.

About NERA

NERA Economic Consulting (www.nera.com) is a global firm of experts dedicated to applying economic, finance, and quantitative principles to complex business and legal challenges. For half a century, NERA's economists have been creating strategies, studies, reports, expert testimony, and policy recommendations for government authorities and the world's leading law firms and corporations. We bring academic rigor, objectivity, and real world industry experience to bear on issues arising from competition, regulation, public policy, strategy, finance, and litigation.

NERA's clients value our ability to apply and communicate state-of-the-art approaches clearly and convincingly, our commitment to deliver unbiased findings, and our reputation for quality and independence. Our clients rely on the integrity and skills of our unparalleled team of economists and other experts backed by the resources and reliability of one of the world's largest economic consultancies. With its main office in New York City, NERA serves clients from more than 20 offices across North America, Europe, and Asia Pacific.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.