Q3 2013 IPO Market Review

The IPO market produced 121 IPOs during the first three quarters of 2013—39 more (48%) than the 82 IPOs completed in the first three quarters of 2012 and nine more than the annual average of 112 IPOs that has prevailed for the past three years. The year-to-date 2013 total is only four IPOs below the average January- September tally recorded between 2004 and 2007—a period with an annual average of 186 IPOs. Gross proceeds declined from $30.60 billion in the first three quarters of 2012 to $25.83 billion in the first three quarters of 2013, a drop largely due to the inclusion of Facebook's $16.0 billion offering in the 2012 tally.

Emerging growth companies (EGCs) continue to dominate the IPO market, accounting for 82% of all IPOs in the first three quarters of 2013—slightly higher than the 76% market share claimed by EGC IPOs last year, following the enactment of the JOBS Act in April 2012.

There were 53 venture-backed US issuer IPOs (44% of the total) in the first three quarters of 2013—12 more than the 41 in the first three quarters of 2012 (50% of the total) and two more than the full-year total for 2012. The first nine months of 2013 saw 39 IPOs by life sciences companies—surpassing the full-year total of 14 in both 2011 and 2012.

With private equity–backed IPOs performing well in the aftermarket and private equity firms eager to achieve liquidity for their portfolio companies, the number of PE-backed IPOs jumped to 38 in the first three quarters of 2013 (32% of the total)—ten more than the full-year 2012 total (28% of all 2012 IPOs).

Overall, technology and life sciences companies have accounted for 65% of the year's IPOs thus far, up from 58% for full-year 2012 and the highest percentage since the end of the dot-com bubble in 2000.

The average IPO company in the first three quarters of 2013 enjoyed a 19% first-day gain from its offering price— eclipsing the 16% average first-day gain for full-year 2012. In the first three quarters of 2013, 37 companies—31% of the total—produced a first-day gain of at least 25%. In this period, 23% of IPOs were "broken" (IPOs whose stock closes below the offering price on their opening day), compared to 20% in all of 2012, but this percentage still represents the second-lowest level of broken IPOs since 2007.

At the end of September, the average 2013 IPO company was trading 44% above its offering price and 36% of the year's IPOs were trading at least 50% above their offering price. Overall, 77% of the year's IPOs were trading above their offering price as of September 30.

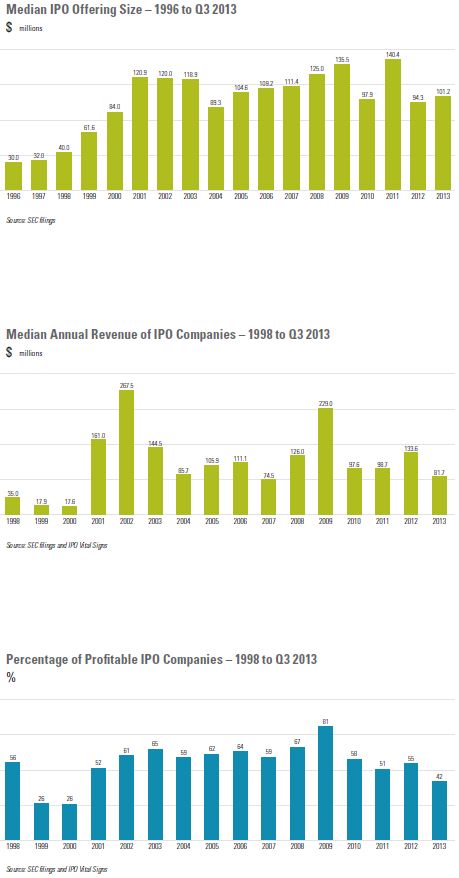

The median deal size of $101.2 million for the first three quarters of 2013 was 7% higher than the $94.3 million median in full-year 2012. The median deal size for VC-backed companies was $77.5 million— the lowest level since the $72.0 million median in 2006—while the median deal size for non-VC backed companies was $226.1 million, 55% higher than the prior ten-year average of $146.0 million. The median deal size for EGCs, at $81.6 million, was less than a fifth of the $436.3 million median deal size for other companies.

The median annual revenue of IPO companies in 2013 remains well below the 2012 level, in part due to the high percentage of life sciences companies going public. Median annual revenue decreased 39%, from $133.6 million in 2012 to $81.7 million in the first three quarters of 2013—the lowest level since the $74.5 million median in 2007. Life sciences companies going public in the first three quarters of the year had median annual revenue of just $10.6 million. EGCs completing IPOs had median annual revenue of $53.7 million, compared to $2.36 billion for other companies.

The percentage of profitable companies going public declined from 55% in 2012 to 42% in the first three quarters of 2013— the lowest level since the 26% in both 1999 and 2000. With investor focus shifting to growth over profitability, only 26% of this year's life sciences and technology-related IPO companies were profitable.

Despite the Federal Reserve's decision not to scale back its bond-buying program, the recent government shutdown and political brinkmanship over raising the country's debt limit that ended with only a short-term solution suggests there may be some market turbulence on the horizon. The currently robust pipeline, however, points to an active fourth quarter with a number of eagerly anticipated IPOs.

Law Firm Rankings

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.