INTRODUCTION

U.S. tax law contains several provisions designed to discourage erosion of the U.S. tax base by moving U.S. businesses offshore. Code §367(a) relates to the transfer of most assets, and unless a transfer of business assets or shares of stock falls within an exception, gain is recognized immediately by the U.S. transferor.1 Under that section, a U.S. person must recognize gain on the transfer of appreciated property to a foreign corporation in a transaction that would otherwise be tax-free, such as a contribution to a controlled corporation that is made by a shareholder or a transfer incident to a reorganization.

The outbound transfer of intangible assets, such as intellectual property ("I.P."), is the subject of a provision within Code §367 because intangible assets are generally easy to move from one country to another and, for that reason, a transfer to a foreign entity in a low-tax jurisdiction could more easily erode the U.S. tax base. As an example, I.P. developed and patented by a U.S. parent corporation may be sold or transferred to its foreign subsidiary corporation with legal title to the I.P.; possession of all of the accompanying rights would also be transferred to the foreign subsidiary corporation simply through the execution of a document and the filing of registration papers. In comparison, when tangible property, such as machinery and equipment, is transferred, the assets must be disassembled and shipped, and factory premises must be constructed or leased.

In the case of outbound transfers of intangible property, Code §367(d)(2) is the counterpart to Code §367(a). It provides that a transfer of I.P. to a foreign corporation in an otherwise tax-free transaction is treated for U.S. income tax purposes as if the I.P. were sold in exchange for payments that are contingent upon its productivity, use, or disposition. In broad terms, the transfer generates an ongoing income stream for the transferor akin to a stream of royalty payments.

While Code §§367(a) and (d) are negative incentives, the Tax Cuts and Jobs Act ("T.C.J.A.") provides a rather broad tax benefit for the use of intangible property, which is defined in the form of a new regime for foreign-derived intangible income ("F.D.I.I."). F.D.I.I. is the portion of a U.S. corporation's specified income derived from serving foreign markets that is broadly defined to be in excess of a return on the tangible assets of a controlled foreign corporation ("C.F.C."). Under Code §951A, F.D.I.I. is included in the income of a U.S. Shareholder (i.e., 10% owner), but under Code §250, F.D.I.I. derived by a U.S. corporation is eligible for a deduction of 37.5% for tax years beginning before 2026 and 21.875% thereafter.2 At the U.S. corporate income tax rate of 21%, the deductions have the effect of reducing the tax rate on F.D.I.I. to 13.125% for tax years beginning before 2026 and 16.406% for tax years beginning after 2025.

This article will examine the following topics:

- The deemed royalty imposed on transfers of I.P. to a foreign corporation

- In the case of a U.S. corporation, the possibility of benefitting from the F.D.I.I. regime by licensing the use of the I.P. to a related or unrelated foreign company

- Using a foreign partnership to avoid deemed royalty treatment in the special (but arguably common) situation of starting up or expanding operations offshore with financing from an investor, such as a private equity fund

DEEMED ROYALTY TREATMENT FOR OUTBOUND I . P. TR ANSFERS

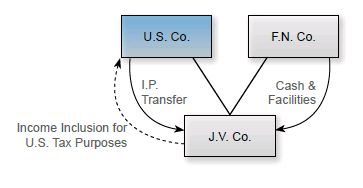

Suppose a U.S. business wants to transfer I.P. to a foreign joint venture that is operated in corporate form. The I.P. will be used in the business operations of the joint venture corporation and is likely contributed as an offset to other contributions by a local co-venturer. The transfer will be subject to Code §367(d), which applies when a U.S. person transfers property to a foreign corporation in a transfer that would be tax-free as a contribution of property to a corporation that is controlled by all the transferors.3

A U.S. person is a U.S. citizen or resident, a domestic corporation, a domestic partnership, an estate other than a foreign estate, or a trust that meets a statutory test that determines whether a trust is controlled by U.S. persons or subject to the jurisdiction of U.S. courts. In that case, the otherwise tax-free contribution in exchange for stock is treated as a taxable sale. If hard assets are contributed, the U.S. person generally must recognize built-in gain with respect to the property. The gain cannot be reduced by any built-in loss. Code §367(a) is said to impose a toll charge on the outbound transfer of appreciated property to a foreign corporation.

If the property contributed to the foreign corporation is I.P., the outbound transfer is governed by the rules of Code §367(d), which take precedence over those of Code §367(a). Under Code §367(d)(2), the contribution is treated like a sale in exchange for payments that are contingent upon the productivity, use, or disposition of the intangible property. In other words, the U.S. person is treated as if it sold the property in exchange for a stream of payments. Note that Code §367(d) controls the tax consequences to the U.S. transferor; it has no effect on the business deal of the parties. The stream of income inclusions must reasonably reflect the amounts that would have been received annually over the useful life of the property in an arm's length sale for ongoing payments. The deemed payments are taxed as ordinary income of the U.S. transferor. The U.S. person must prepare a valuation of the intangible property in accordance with rules set forth in the Treasury regulations.

If the foreign corporation subsequently disposes of the I.P., the U.S. transferor is treated as if it received a final payment on that disposition. The following diagram illustrates the transaction.

For Code §367(d) purposes, intangible property is listed in Code §367(d)(4) as including patents, invention, formula, process, design, pattern, know-how, copyright, trademark, trade name or brand name, franchise, license or contract, and other items with a value (or potential value) that is not attributable to tangible property or the services of any individual.

KEEPING I . P. ONSHORE FOR F. D. I . I . TREATMENT

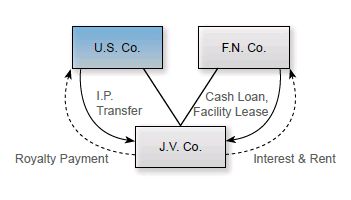

The first alternative to a contribution of I.P. to a foreign corporation is a license of the I.P. as part of a modified structure.

If, instead of forming a foreign corporation that would fully operate a business abroad, the U.S. company retained its I.P. and licensed it to the foreign joint venture in return for an actual royalty payment, Code §367(d) would not be applicable. Rather, the F.D.I.I. regime could apply and ultimately result in reduced U.S. tax for the U.S. participant. Consequently, the foreign co-venturer would likely demand a comparable payment in return for its assets, leading to a somewhat different structure.

The F.D.I.I. of any U.S. corporation is its "deemed intangible income" multiplied by a ratio consisting of its "foreign-derived deduction eligible income" as the numerator and its global "deduction eligible income" (i.e., U.S. and foreign) as the denominator.

The U.S. corporation's deemed intangible income is effectively all of its income [net of allocable deductions and certain exclusions such as its Subpart F Income and global intangible low taxed income ("G.I.L.T.I.")] inclusions reduced by a deemed routine return of 10% of its adjusted tax basis in its depreciable tangible property.

Perhaps the most important component of F.D.I.I. is the foreign-derived deduction eligible income. In broad terms, foreign-derived deduction eligible income is any deduction eligible income (i.e., gross income, reduced by allocable deductions and certain exclusions) derived in connection with

- property that is sold by the taxpayer to any person who is not a U.S. person and established to be for foreign use or

- services provided by the taxpayer that are established to be provided to any person not located in the U.S. or with respect to property not located in the U.S.

The terms "sold," "sells," and "sale" include any lease, license, exchange, or other disposition. Foreign use means any use, consumption, or disposition outside the U.S.

Property sold to another person (other than a related party, as discussed below) for further manufacturing or other modification in the U.S. is not treated as sold for a foreign use, even if the other person subsequently uses the property for foreign use. Similarly, services provided to another person (other than a related party, as discussed below) located in the U.S. do not generate foreign-derived deduction eligible income even if that other person uses the services in providing services that generate foreign-derived deduction eligible income for itself. Here, those limitations should be inapplicable as the joint venture corporation is a foreign corporation with actual foreign operations. Hence, the license – the equivalent of a sale – is to a foreign corporation, which depending on the character of the I.P., will either use the licensed I.P. to manufacture abroad or will use the licensed I.P. to sell abroad.

If the property is sold to a foreign related party,4 the sale is not treated as for a foreign use, unless the property is ultimately sold by the foreign related party to another person who is unrelated and foreign, and the taxpayer establishes to the satisfaction of the I.R.S. that the property is for foreign use. Similarly, if a service is provided to a related party who is not located in the U.S., the service is not treated as provided for foreign persons or with regard to property located outside the U.S., unless the taxpayer establishes to the satisfaction the I.R.S. that the service is not substantially similar to services provided by the related party to persons located in the U.S.

The F.D.I.I. regime presents the possibility of keeping I.P. in the U.S. and licensing it to a foreign joint venture corporation for use in manufacturing or selling a product for use outside the U.S. The license would not run afoul of Code §367(d) and would generate F.D.I.I. for the U.S. corporation. If the licensee is a foreign related party for F.D.I.I. purposes, the joint venture corporation will be required to demonstrate that the I.P. was used to service foreign markets.

The U.S. corporation's tax rate on the F.D.I.I. (i.e., the royalty income from the lisidiary) will be 13.125% (16.406% for tax years beginning after 2025). This is clearly more favorable tax treatment than that imposed under Code §367(d)(2) since the deemed royalty income would be subject to U.S. corporate income tax at 21%.

Note that there is a G.I.L.T.I. component to the planning, as well. A U.S. Shareholder of a C.F.C. will be subject to tax on the G.I.L.T.I. of that C.F.C. A full discussion of G.I.L.T.I. is beyond the intended scope of this article. Nonetheless, it is important to note that the G.I.L.T.I. provision, like F.D.I.I., is a new regime introduced by the

T.C.J.A. It imposes an immediate tax on the G.I.L.T.I. of a C.F.C., which in broad terms is all income of the C.F.C. with certain exceptions, including (i) Subpart F Income otherwise taxed in the hands of a U.S. Shareholder (excluding the effect of exemptions from Subpart F), (ii) effectively connected income taxed in the U.S., and (iii) a base amount of the C.F.C.'s gross income that is attributable to a routine return on depreciable tangible property, as mentioned above.

The tax rate on G.I.L.T.I. generally is 10.5% (13.125% for tax years beginning after 2025), although the computation of the rate is subject to the variable of foreign taxes paid or accrued on the G.I.L.T.I. Proposed regulations under Code §951A, other than rules related to the foreign tax credit for a G.I.L.T.I. inclusion, were published by the I.R.S. on September 14, 2018.5

NO DEEMED ROYALTY ON TR ANSFER TO PARTNERSHIP

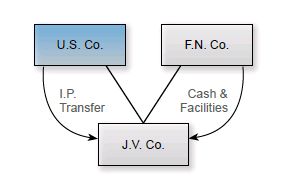

The second alternative is to use a foreign partnership as the joint venture vehicle. Under Code §721(a), neither a partnership nor any of its partners will recognize gain or loss on the contribution of property to the partnership in exchange for an interest in the partnership. This is illustrated in the following diagram, where the joint venture corporation makes a "check-the-box" election to be treated as a partnership for U.S. income tax purposes. In principle, J.V. Co. remains a separate company for purposes of the tax in its country of residence and in F.N. Co.'s country of residence.

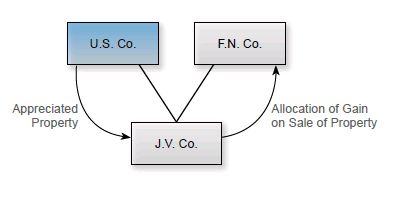

There are several exceptions to the general rule nonrecognition tool of Code §721(a), including Code §721(c), which grants the I.R.S. the authority to draft regulations that override the Code §721(a) nonrecognition rule when the contribution of appreciated property to a partnership will result in a foreign person recognizing the built-in gain. The concern addressed by Code §721(c) is the shifting of the built-in gain from a U.S. person to a fo eign person through the contribution of the appreciated property to the partnership.

Code §367(d)(3) states that the I.R.S. may issue regulations applying the deemed royalty treatment of Code §367(d)(2) (discussed above) to a transfer of intangible property by a U.S. person to a partnership. Code §721(d) cross-references Code §367(d)(3) for regulatory authority to treat transfers of intangible property as sales. Thus, under §721(c) the I.R.S. has the authority to issue regulations to turn off the Code §721(a) nonrecognition rules and under Code §721(d) it has authority to issue regulations to apply the deemed royalty treatment of Code §367(d)(2) to an outbound transfer of intangible property to a partnership. To date, the I.R.S. has issued temporary regulations under Code §721(c) but has not issued regulations under Code §721(d).

The temporary regulations issued under Code §721(c) address the contribution of appreciated property by a U.S. person to a partnership (domestic or foreign) in which (i) a related foreign person6 is a direct or indirect partner and (ii) the U.S. person and the related persons own, directly or indirectly, 80% or more of the interests in the partnership capital, profits, deductions and losses.

The appreciated property, referred to as "Code §721(c) property," is broadly defined as property other than "excluded property." Excluded property is cash, securities, tangible property with de minimis built-in gain, and an interest in a partnership in which effectively all of its assets consist of the foregoing excluded property. As a result, Code §721(c) property includes intangible property.

Importantly, the nonrecognition treatment of Code §721(a) may nonetheless apply to such a contribution if the partnership takes certain steps. In broad terms, the partnership must elect to apply a certain method of allocating the built-in gain with respect to the contributed property, referred to in the regulations as the "gain deferral method" and follow certain administrative procedures. The gain deferral method ensures that partnerships will not be able to shift the tax on the built-in gain contributed property to the related foreign person and thereby escape U.S. taxation. If the partnership fails to follow these steps, the gain recognition rules of the temporary regulations are triggered.

Although the I.R.S. has issued guidance under its authority to treat outbound transfers of property, including intangible property, to a partnership as taxable, the guidance covers the narrowed circumstances of a partnership with a foreign partner that is related to the U.S. transferor. To date, the I.R.S. has not used its authority to issue guidance or regulations that override the Code §721(a) nonrecognition rule and impose a deemed royalty in the case of intangible property transferred to a partnership for use outside the U.S.

In the case of a U.S. person negotiating a foreign joint venture to service foreign markets where the business terms contemplate a transfer of I.P. to the foreign joint venture corporation, a check-the-box election to treat the joint venture as a partnership may solve the deemed royalty issue under Code §367(d)(2).

However, the solution comes with a tax cost. The U.S. corporation will not benefit from the low tax under F.D.I.I. because foreign branch income does not qualify for the deduction and will not qualify for the low tax under G.I.L.T.I., because only a C.F.C. triggers income under Code §951A and the deduction under Code §250. Nonetheless, it may provide tax results that are in line with the business deal under negotiation by the U.S. corporation and the foreign co-venturer.

If the I.P. relates to a trademark or a trade name, the transfer of the I.P. must meet the tests of Code §1253 in order to be treated as a sale or exchange of property. Under the general rule of Code §1253(a), the transfer of trademarks, trade names, and franchises is not treated as a sale or exchange of a capital asset if the transferor retains any "significant powers, right, or continuing interest" with respect to the subject matter of the franchise, trademark, or trade name.

A significant power, right, or continuing interest includes but is not limited to, a right to

- disapprove any assignment of the interest, or any part thereof,

- terminate at will,

- prescribe the standards of quality of products used or sold, or of services furnished, and of the equipment and facilities used to promote such products or services,

- require that the transferee only sell or advertise products or services of the transferor,

- require that the transferee purchase substantially all of his supplies and equipment from the transferor,

- payments contingent on the productivity, use, or disposition of the subject matter of the interest transferred, if such payments constitute a substantial element under the transfer agreement.

If the transferor retains any significant power, right, or continuing interest in the franchise, trademark, or trade name, any payments contingent on the productivity, use, or disposition of the property, it will generally be treated as ordinary income of the transferor. Although not relevant to this type of planning, any payments received that are not contingent payments described above will be treated as gain from the sale of a capital asset of the transferor.

The key to addressing control of a product that is to be sold under a brand name without having the U.S. corporation run afoul of Code §1253 is to build the prescribed factors into the shareholder's agreement rather than the license agreement. This approach can be used to ensure that the operations of the joint venture corporation are carried on in a way that does not adversely affect the value of the trademark in other parts of the world. However, reliance on a shareholder's agreement will not protect the U.S. corporation from losing control of the trademark within the country in which the joint venture corporation operates in the event of a bankruptcy of the joint venture corporation. Protection against that risk may require an option to acquire the trademark at fair market value in the event of a filing for court protection against claims of creditors.

CONCLUSION

When expanding operations abroad, the transfer of ownership of I.P. or use of I.P. requires careful planning. With proper structuring, it is possible that a license arrangement in return for an arm's length royalty may provide benefits under the F.D.I.I. and G.I.L.T.I. rules by reducing the rate of U.S. Federal corporate income tax from 21% to as little as 13.125% for F.D.I.I. and 10.5% for G.I.L.T.I. However, in a cross-border joint venture where the U.S. party is contributing I.P., the need to pay a royalty may not fit the business deal. In that set of circumstances, use of a joint venture corporation that makes a check-the-box election may be the easiest structure to implement if the U.S. corporation is amenable to transferring ownership of the I.P. within a specific geographical location to the joint venture hybrid entity. Care must be taken to ensure that the transfer of a trademark in return for a partnership interest is viewed to be a transfer of property and not a de facto license by reason of Code §1253.

Footnotes

1 The T.C.J.A. eliminated one principal exception that allowed gain to be deferred in connection with a tax-free transfer of assets to a foreign corporation when the assets would be used in an active trade or business. See "Tax Cuts and Jobs Act Adopt Provisions to Prevent Base Erosion," Insights 5, no 1 (2018), pp. 40,

46-47.

2 Note that the amount of the Code §250 deduction is capped by the U.S.

3 Code §351(a).

4 For this purpose, a related party is determined under the rules for determining whether a corporation is a member of an affiliated group of corporations within the meaning of Code §1504(a) by substituting "more than 50%" for "at least 80%" and certain other adjustments (Code §250(b)(5)(D)).

5 REG-104390-18, September 14, 2018.

6 Whether the persons are related is governed by the rules of Code §§267(b) or 707(b)(1). Code §§267(b)(1) through (13) describe related parties, including, inter alia, family members and entities that are controlled by the same persons. Individuals are considered related if they are spouses, siblings, ancestors, and lineal descendants. A corporation and a partnership are related if the same persons own more than 50% in value of the outstanding stock of the corporation and more than 50% of the capital interest, or the profits interest, in the partner- ship. Under §707(b)(1), a partnership and a partner are related if the person owns, directly or indirectly, more than 50% of a capital or profits interest in the partnership, and two partnerships are related if the same persons own, directly or indirectly, more than 50% of the capital interests or profits interests.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.