INTRODUCTION

The limitation of interest deductibility to approximately 30% of E.B.I.T.D.A. (earnings before interest, tax, depreciation, and amortization) introduced in amended Code §163(j) has focused the attention of U.S. corporations and their lenders on a new constraint.

For companies with sales less than $25 million that borrow from a foreign parent, the body of case law in the style of Mixon and Laidlaw has remained the standard against which interest deductibility is evaluated by the I.R.S. Large subsidiaries of foreign parents that do not qualify for the Code §246 gross sales exemption of $25 million are accustomed to (i) proving their capacity to carry and service debt and (ii) demonstrating that the rate of interest and other terms attaching to a cross-border loan are arm's length under Treas. Reg. §1.482-2, the concepts of Code §385 regulations, and applicable case law. These companies are also subject to the 30% E.B.I.T.D.A. limitation.

For related domestic borrowers, including companies with less than $25 million in sales, the Code §163(j) limitation introduces a requirement to think differently about debt, importing rules that were used in international transactions into a wholly domestic context. This comes at a time when debt has become a critical means of funding continuing operations and expansion for many businesses.

The boundary between debt and equity has historically been located using one of three approaches: the qualitative approach of case law, the data-driven approach of comparative analysis, and the procedural approach for borrowers as set out in the Code §385 regulations.

CASE LAW

The case law focuses on the difference between the expected tax consequences of debt, on the one hand, and equity, on the other. Interest income to a lender results in an expense deduction to the borrower within certain limitations, whereas the dividend distributions on equity funding result in income to the equity-holder but no deduction to the borrower.

In a cross-border context involving most treaty partner jurisdictions, interest revenue is taxable to the lender only in its jurisdiction of residence, whereas the dividend is subject to withholding tax by the jurisdiction of the payor and typically exempted in the context of a parent-subsidiary fact pattern. While repayment of loan principal is tax-free, repayment of shareholder capital is accorded different tax treatment. Hence, legal or economic analysis is required to distinguish between an equity investment and a loan. The ultimate conclusion is whether, on balance, the instrument appears to be more like debt or more like equity.

Successive decisions added to the list of factors suggestive of bona fide debt and came to be known as the Mixon factors. These factors were applied to indebtedness circumstances other than in the financial and insurance sectors. Jurisprudence that references these factors invariably state that no single criterion or any set of criteria point conclusively to an instrument being debt or equity, and that a unique set of fact deserves a unique evaluation. As a consequence, the Mixon factors currently provide a useful list of do's and don'ts of debt but are suggestive of neither a process nor a definitive analytical framework.

CODE § 385

The first attempt at U.S. codification was introduced in 1969 and was, through many starts and stops, either the official or unofficial rule on bona fide indebtedness until 2018.

Regulations issued by the I.R.S. under Code §385 in its most recent incarnation aimed to classify an interest in a corporation (or part thereof) as either stock or indebtedness for the purposes of the Code. Drafted as a response to inversion transactions, the regulations concentrated on defining indebtedness for U.S. borrowers (i.e., U.S. issuers of debt) using some of the Mixon factors to set out a four-factor definition that referenced the issuer's binding obligation to pay a sum certain, the holder's rights to enforce payment, a reasonable expectation of repayment, and a course of conduct that is generally consistent with the debtor-creditor relationship. At once reviled by businesses and adored by consulting firms ready to meet yet another vague and onerous documentation requirement, the regulations implementing the Code §385 documentation requirement was removed on September 23, 2018, by REG-130244-17.

If the Mixon factors and Code §385 can be thought of as theory in search of a pattern in the data, the quantitative methods that grew up to fill a gap in debt characterization and pricing analysis follow a loose approximation of the opposite approach – relying on patterns in the data to reveal and test possible theories. Where Mixon falls short on method, the behaviors of C.F.O.'s and lending institution credit officers offer guidance, as do loan covenant terms in credit agreements appended to S.E.C. filings and the published rating practices of credit rating agencies.

QUANTITATIVE APPROACH

Likening the negotiation of a term sheet between a related corporate lender and its related borrower to a C.F.O. preparing for a presentation to a bank or mezzanine lender and the inevitable follow up questions proves instructive. Rather than diving directly into the market for a dark blue suit in what may be the buyer's last known or aspirational size and trying to fit into an off-the-rack product from Mixon, a C.F.O. is far better off with measurements and a list of requirements in hand, as well as a budget constraint. All that remains is to determine how much suit can be purchased and, with that information in hand, let the tailoring begin.

A good starting point is to draft a term sheet. This would include the issue date, maturity date, principal amount, detail on tranches, whether security will be taken back, seniority, initial target interest rate (fixed or floating), frequency of payment of interest and principal, prepayment options, guarantees, and demand options. This will form the basis for comparability analysis, debt capacity, creditworthiness, and preparation of forecasts.

Going back to the hypothetical C.F.O.'s meeting with the credit officer, the next consideration is to think about the loan instrument in context. At any particular time, a borrower will have a certain capital structure that will be the starting point for the addition of debt. The current capital structure is the result of past activity that carries with it a history of accessible capital markets terms and covenants related to prior financing. With some knowledge of the current disposition of credit markets toward borrowers in the relevant industry, some of which can be gleaned from informal discussions with bankers and other financial industry participants, it is usually not difficult to construct a hypothetical third-party lender and to anticipate some of the constraints or concerns such a lender would want to manage through terms in a loan agreement. Some of these hypotheticals will lead to revisions in the draft term sheet, and a better understanding of the credit market that is currently relevant to the proposed borrowing.

Often, it is not a big matter to prepare a forecast for a new project, investment, or acquisition. Forecasting earnings and free cash flow is needed to determine the investment internal rate of return and also serves as the basis for understanding the capacity to borrow – commonly known as debt capacity – even in the circumstance where the lending is being contemplated to support financing ongoing operations. A good forecast will clearly show the borrower's ability to service debt and repay debt at maturity (two of the Mixon conditions) and allow for the calculation of certain leverage ratios that will help go beyond Mixon to determine whether the proposed debt can reliably be called debt by reference to comparable company or industry participant leverage ratios.

Taken together, the ability to service debt, repay principal and interest, and maintain a balance sheet of comparable attributes will lead to a conclusion about debt capacity. Does the principal amount on the term sheet push any of the debt service or leverage capacity measures offside? A scan of covenant terms using Reuters Loan Connector and Dealscan is helpful here, as is Bloomberg, S&P Capital IQ, and other sources for comparable industry or peer company data and deal terms.

When the amount and type of debt is known, the last step is to compute an arm's length interest rate. The risk profile of the borrower is often represented as a credit score or credit rating, and the same construct can apply to a controlled issuer of indebtedness. Computing a hypothetical letter rating can be done using the Moody's or S&P scales. Rating agencies publish their methodologies by industry, and with a little effort, these methods can be applied using company financial statements and forecasts. As an alternative to a first principles approach using a published rating method, a "black-box" calculator like S&P Credit Model or Moody's RiskCalc can be used to derive a synthetic credit rating.

A letter rating will allow for the screening of loan and bond issue data for issues of a similar creditworthiness. It should be noted that for Code §482 transfer pricing issues, a standard of comparability must be met. This means that the characteristics or terms of individual issues must be examined to ensure that the interest rate selected is based on issues with comparable terms. One can often find published credit spreads for composite issuers or issues of a certain credit rating. These points of data may be useful in the domestic context. However, they often are too aggregated to be used to meet the comparability criteria in the cross-border or international transfer pricing context.

Comparability encompasses all loan and guarantee terms, not just the price or interest rate. Examples of terms that must be examined for comparability to the proposed controlled indebtedness issue include currency, industry sector, purpose or use of financing, term to maturity, payment frequency, embedded options, securitization, seniority, size of borrowing or principal amount, and geographic attributes.

Perfection is not the objective here, as the effects of differences may be eliminated with appropriate adjustments. For example, fixed rates can be converted to floating rates using the appropriate interest rate swap contract data, and term to maturity can be adjusted using an appropriate yield curve.

This approach must often be taken in an iterative manner, incorporating new terms into forecasts to determine whether the financial ratios related to debt service and repayment terms are consistent with ratios sampled from comparable deals or companies. Adopting the practice of adjusting the draft term sheet while iterating toward an arm's length result creates the favorable outcome of a table that can be referenced while drafting the loan or credit agreement.

The result is a range of interest rates and collection of on-market terms that stand as an estimate of the terms of bona fide indebtedness for all marginal dollars of debt or of specific amounts of indebtedness within specific debt tranches.

TAX REFORM IMPACT

The T.C.J.A. in 2017 influenced debt financing through a "thin cap" rule that limits interest expense for leveraged issuers and the B.E.A.T. rule, which may apply to deductions for interest expense paid to foreign affiliates. Further, the Code §267A anti-hybrid rules deny a deduction for interest and royalty payments that constitute "disqualified related-party amounts." These anti-hybrid rules target cases in which a U.S. person gets a deduction but the foreign person has no income pick up.

SUMMARY

While Code §482 often is thought of as applying in international contexts, its scope with broad enough to apply to domestic transactions. Hence, it may be prudent to consider taking an abbreviated quantitative approach where debt principal values in domestic transactions are large or loan terms are unique. Apart from the 30% profit limitation to interest deductibility (with profit measured as E.B.I.T.D.A., transitioning to E.B.I.T. (earnings before interest and taxes) for taxable years beginning on or after January 1, 2022), case law will still apply.

The current Code §163(j) interest deductibility limitation serves only to limit the total interest expense on total indebtedness and does not define the point at which a marginal dollar of funding ceases being debt and begins to be equity in its character. The location of this cut-off point, and therefore the test for bona fide indebtedness, remains to be determined using case law, a quantitative approach, or some combination of the two. Code §163(j) should therefore be treated as a necessary but not sufficient condition for interest deductibility.

Footnotes

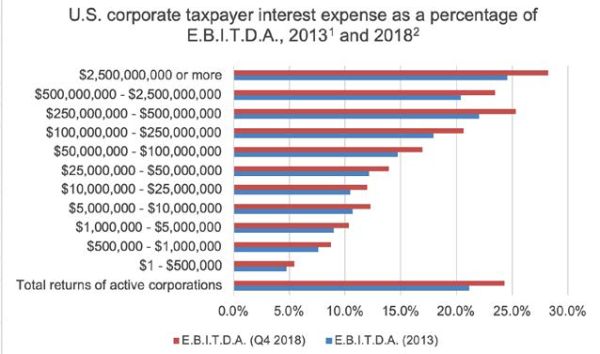

1. I.R.S., Balance Sheet, Income Statement, and Selected Other Items, by Size of Total Assets Tax Year 2013, SOI Tax Stats – Table 4.

2. Estimate produced using Q4 2013 and Q4 2018 values from Board of Governors of the Federal Reserve System (U.S.), Nonfinancial Corporate Business; Debt as a Percentage of the Market Value of Corporate Equities, Level [NCBCMDPMVCE], retrieved from FRED, Federal Reserve Bank of St. Louis.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.