In March 2023, the Belgian Minister of Finance published a proposal for a broad tax reform aiming more generally at modernising and simplifying the tax system and making the system more equitable. Items of the reform included, for example, changes to the participation exemption regime, the innovation income deduction, the investment deduction regime, the partial wage withholding tax exemption for research & development, the use of the stock option plans and the tax regime of carried interest.

After several months, it appeared difficult to reach political agreement on the various aspects of the tax reform. In July 2023, the Prime Minister announced that negotiations on the tax reform had failed as no consensus could be reached. Although no major reform could be agreed upon, some tax measures were announced in October 2023 as part of the budget agreement. These budgetary tax measures are incorporated into a Program Law and have been approved on 21 December 2023 in Belgian Parliament in plenary session. The Program Law has, however, not yet been published in the Belgian Official Gazette.

Many legislative changes are typically approved by Belgian parliament before year end. In this respect, some other tax measures have been approved recently or will be approved shortly. The Belgian Parliament approved, for example, on 15 December 2023 the draft Bill that implements the Pillar Two rules and that amends the current Tax Credit for R&D to qualify as a Qualified Refundable Tax Credit under Pillar Two rules. For more information we refer to our Tax Flash of 16 November 2023.

Below, we discuss the most important budgetary tax measures. Some aspects are rather complex and will require a case-by-case analysis.

Towards a more stringent CFC rule

CFC-legislation aims to avoid profit shifting by taxing non-distributed income, earned by a Controlled Foreign Company (CFC) at the level of the controlling parent entity.

The Anti-Tax Avoidance Directive (ATAD) obliged

Member States to implement a CFC rule and left Member States the

option to (i) either include non-distributed specific types of

passive income in the taxable basis of the controlling taxpayer

(Model A); or (ii) include non-distributed income arising from

non-genuine arrangements which have been put in place for the

essential purpose of obtaining a tax advantage (Model B).

At that time, Belgium opted for Model B, implying that CFC income

can only be taxed in Belgium if it is attributable to the

significant people functions carried out by the Belgian controlling

taxpayer. This CFC rule entered into force in 2019, but the

Minister of Finance confirmed in May 2023 that this rule was never

applied in Belgium so far as it overlaps with transfer pricing

rules.

Since the current CFC rule proved in practice to be of little relevance, the Belgian legislator has now decided to switch from Model B to Model A, which is the other, more far-reaching option that the ATAD provided. The new CFC rule is further explained below.

1. What is a CFC and which conditions should be met?

A foreign company (or PE of this foreign company) qualifies as a CFC if the participation and taxation tests are met. A foreign permanent establishment (PE) of a Belgian taxpayer is also included in the scope of application if Belgium concluded a double tax treaty with the country where the PE is located and the taxation test is met.

a) Participation test

The Belgian taxpayer should by itself or together with associated enterprises hold, directly or indirectly, the majority of voting rights, or own, directly or indirectly at least 50% of the capital, or is entitled to receive at least 50% of the profits of the foreign company. The assessment of the participation test must be made at the end of the taxable period.

b) Taxation test

The foreign company or foreign PE is in its country of residence either not subject to an income tax or is subject to an income tax that is less than half of the income tax that would be due if the company or PE would be established in Belgium. In calculating this income tax, the profits that the foreign company would have realized through a PE is disregarded if a double tax treaty applies between the country of the foreign company and the country in which the PE is located that exempts this profit.

The taxation test is deemed to be met if the foreign company or PE is established in a jurisdiction which appears on a Belgian list of no or low taxed countries or the EU's list of non-cooperative jurisdictions. This presumption is rebuttable.

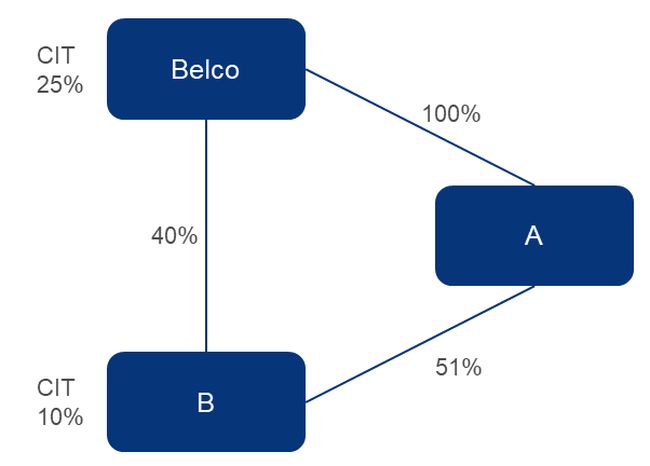

Example:

Belco holds in total more than 50% of the capital of company B (i.e. 40% directly + 51% indirectly). Company B, a foreign company, which is not located in a jurisdiction targeted by one of the abovementioned lists, has a taxable income of EUR 100,000 according to its local tax rules. The corporate income tax due amounts to EUR 10,000 (10% x 100,000). According to the Belgian tax rules, the taxable income of company B would amount to EUR 125,000. If the company would be established in Belgium, corporate income taxes in the amount of EUR 31,250 (25% x 125,000) would be due. Since the taxes paid by company B (EUR 10,000) are less than half of the taxes that would be due if the company would be established in Belgium (EUR 15,625), the foreign company qualifies as a CFC.

2. Are there any exclusions?

Even if the participation and taxation tests are fulfilled and the foreign company or PE qualifies as a CFC, the (non-distributed) CFC income is not necessarily subject to CFC taxation. An exemption applies in any of the following three situations:

- The CFC carries on a substantive economic activity supported by staff, equipment, assets and premises as evidenced from facts and circumstances. An 'economic activity' means selling goods or providing services on a certain market. Rendering intra-group services cannot be considered as an economic activity if the terms and conditions are not at arm's length. The economic activity must also substantive, i.e. the income derived from these activities must be substantial compared to the total income of the CFC;

- Less than one third of the income accruing to the CFC constitutes passive income;

- The CFC qualifies as a financial undertaking as defined by law (for example, credit

institutions, investment companies and (re)insurance undertakings) and derives its passive income for max. one third from transactions with (an associated entity of) the Belgian taxpayer.

3. Which categories of income are taxed under the CFC rules?

If a foreign company or PE qualifies as a CFC and cannot benefit from an exemption, the non-distributed passive income of the CFC as determined according to Belgian tax rules becomes taxable in the hands of the Belgian taxpayer. The following categories of passive income are targeted:

- Interest or any other income equal to interest (i.e. similar as for the EBITD rule);

- Royalties or any other income generated from intellectual property;

- Dividends and income from the disposal of shares, bonds, options and similar securities;

- Rental income, or income from financial or operational leasing;

- Income from asset management, investment, insurance, banking and other financial activities;

- Income from the purchase and sale of goods and services to which little or no economic value is added by the CFC.

4. How is double taxation being avoided?

Double taxation is avoided by three different measures.

First, the CFC income that is taxable must be limited to the Belgian taxpayer's direct participation in the foreign company that qualifies as a CFC. The highest percentage of direct participation held in voting rights, capital or profit entitlement must be considered in this respect. Referring to the example above, and assuming that the entire income of the CFC constitutes qualifying (non-distributed) passive income and no exemption applies, the CFC income that is subject to corporate income tax in Belgium amounts to EUR 50,000 (125,000 x 40%).

If other countries would impose a CFC tax on indirect participations, double taxation could arise. In these circumstances, these other countries are expected to eliminate the double taxation.

Second, previously taxed CFC-income that is being distributed will in principle fully benefit from the participation exemption regime ("DBI-aftrek" / "déduction RDT") in the hands of the Belgian taxpayer (controlling entity). In addition, capital gains realised on the disposal of shares of a CFC will in principle be exempt to the extent that the profits of the CFC have already been taxed in the hands of the Belgian taxpayer (controlling entity) as CFC income and these profits have not yet been distributed and still exist on an equity account prior to the alienation of the shares. An exception applies in case of a change of control of the CFC that is not motivated by legitimate financial or economic needs.

Finally, a tax credit is granted to the Belgian taxpayer for the taxes that the CFC pays in its country of residence on the passive income. In case of insufficient Belgian taxes to offset the CFC's local taxes, the unused CFC's taxes are not repaid but can be carried forward.

5. Are there any reporting obligations?

Under the current regime, a Belgian taxpayer should only report in its tax return that it holds a participation in a foreign company or PE that qualifies as a CFC if the income is subject to tax in the hands of the Belgian taxpayer pursuant to the CFC rule.

Under the new regime, the reporting obligation is extended. A Belgian taxpayer should always report in its tax return that it holds a participation in a foreign company or PE that qualifies as a CFC, even if the CFC benefits from an exemption. If the presence of a CFC is reported, some additional information must be disclosed, such as for example the place of management of the CFC and, if applicable, the exemption that is relied upon.

6. When will the new CFC rule enter into force?

The new CFC rule will apply as of assessment year 2024.

7. What is the impact of Pillar Two on the new CFC rule?

The Pillar Two rules allow low tax jurisdictions to impose a Qualified Domestic Minimum Top-Up Tax (QDMTT). The QDMTT is a minimum tax that is included in the domestic law of a (low tax) jurisdiction and that is calculated in a way that is consistent with the Pillar Two rules. Once this domestic minimum tax fulfills all conditions and can be considered a QDMTT, this QDMTT is credited against any top up tax due under the Pillar Two Rules. The primary taxing rights are thus attributed to the jurisdiction applying the QDMTT which allows a low tax jurisdiction to tax own revenues, and which prevents that the top up tax would go to another country. The OECD Administrative Guidance of 1 February 2023 foresees that the QDMTT applies before any CFC tax. It remains unclear at present whether the application of the QDMTT in a low tax jurisdiction automatically excludes the application of the CFC tax in Belgium. Although one might assume that the QDMTT paid by the CFC can be considered when verifying the above-mentioned taxation test, a clarification in this respect would be helpful. The Administrative Guidance of 17 July 2023 mentions though that jurisdictions may decide how to allocate the QDMTT liability among the Constituent Entities in its jurisdiction. A jurisdiction could thus allocate the QDMTT liability to another entity than the low tax entity. In these circumstances, the CFC rule might still be applicable considering that the taxation test should be verified on an entity-by-entity basis.

Cayman Tax: a never ending story

The Cayman tax is a set of rules in the Belgian Income Tax Code, introduced in 2013, to prevent Belgian tax residents from avoiding taxation by holding assets through foreign low-taxed legal entities and trusts (legal structures). Individual tax residents of Belgium, subject to personal income tax, and legal entities established in Belgium, subject to the tax for legal entities, are in scope of the Cayman tax, if they are a founder (and/or beneficiary) of a legal structure (founder).

A founder is taxed on the income generated by the assets of the legal structure as if he (or she) received the income directly (look-through-tax).Tax is also due by the founder (and/or beneficiary) on distributions received from the legal structure. The founder needs to report the legal structure in his (or her) personal income tax return.

Although the Cayman Tax has been adjusted several times since its introduction in 2013, the Minister of Finance considers that certain loopholes are still not closed. The Cayman Tax can, for example, be circumvented by interposing an entity that does not qualify as a legal structure or by emigrating from Belgium. In addition, it appears that the Belgian Tax Administration encounters practical difficulties in classifying a Belgian taxpayer as a founder, assessing the actual economic activity of a legal structure (when the so-called substance carve-out is invoked, see question 7) and in monitoring the application of the Cayman Tax. These issues were already raised in a report of the Belgian Court of Audit on the Cayman Tax dated April 2023 and are now being addressed by the Belgian legislator in the approved Program Law. These amendments to the Cayman tax are far-reaching and have a significant impact in practice.

1. How is a legal structure defined under the current rules and what will change?

Under the current rules, trusts qualify as legal structures and are in scope of the Cayman tax, if an individual Belgian tax resident is the (heir of the) settlor of the trust. Entities established outside Belgium that are not taxed or low-taxed according to Belgian standards qualify as legal structures and are in scope of the Cayman tax, if an individual Belgian tax resident holds the shares of the entity.

Under the current legislation, direct shareholdings are in scope as well as shareholdings via one or more other legal structures (chain of legal structures).

Under the new rules, the concept of chain of legal structures is replaced by the concept of intermediate structure (intermediate structure). An intermediate structure is a legal structure or an entity (with or without legal personality) that holds the shares of a legal structure or another intermediate structure.

The application of the Cayman tax on shareholdings via intermediate structures in thus introduced. An intermediate structure can be a company subject to tax.

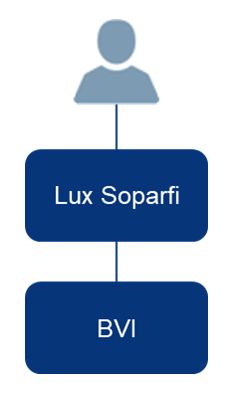

Example:

An individual Belgian tax resident holds a BVI company through a Luxembourg Soparfi. The Soparfi is a normally taxed company established in Luxembourg. Under the current rules, the Cayman Tax does in principle not apply since the Belgian resident does not hold the shares of the BVI company directly and the Luxembourg Soparfi is not a legal structure. Under the new rules, the individual Belgian tax resident will qualify as a founder of a legal structure (the BVI company) via an intermediate structure (the Luxembourg Soparfi).

2. Who is a founder under the current rules and what will change?

Under the current regime, only direct shareholders are founders as well as shareholders via a chain of legal structures. If the direct shareholding of an individual Belgian tax resident is held in a normally taxed company that holds in its turn the shares of a low taxed entity, the shareholder will not qualify as a founder of the low taxed entity under the current regime as is shown in the example under question 2.

Under the new rules, the concept of founder is extended to indirect shareholdings via a chain of intermediate structures. The concept of intermediate structure is defined in our answer to question 1.

In addition, the new rules introduce a rebuttable presumption: individual Belgian tax residents who are identified as ultimate beneficial owner (UBO) of a legal structure (in the Belgian UBO register or its foreign equivalent) are deemed to be a founder.

3. What is the look through approach under current rules and what will change?

Based on the look-through approach, income realized by a legal structure is taxable in the hands of the founder, as if the founder received the income directly. The actual distribution of the income to the founder is not relevant.

Taxation of the income in the hands of the founder is based on the personal income tax rules. Dividends and interest are taxed at a flat rate of 30%. Capital gains realized on shares can be free from income tax in the hands of an individual Belgian tax resident, provided that the gains are realized within the normal management of private assets.

Example:

An individual Belgian tax resident is the founder of a BVI company (legal structure). The BVI company holds a securities portfolio. The BVI company sells shares and realizes a capital gain. The look through tax is applicable. The founder will not be effectively taxed if the gain qualifies as realized within the normal management of private assets.

In case of a chain of legal structures, all income received by the legal structures of the chain will be added together and taxed in the hands of the founder, with rules to avoid double taxation.

The above look-through approach remains unchanged under the new rules, being it that it is now explicitly specified that the look-through approach will aways have precedence over taxation upon distribution to the founder, even when the legal structure/intermediate structure distributes the income in the same year.

4. How are distributions to the founder taxed under the current rules and what will change?

Under the current legislation, all distributions made by a legal structure are taxed at a flat rate of 30%, unless and insofar:

- the distribution stands for contributions made by the founder (this exemption may only be invoked if the founder can demonstrate that the overall value of the legal structure has dropped below the amounts initially contributed), or

- the distribution stems from income that has been subject to tax in Belgium.

Under the new rules, all distributions made by a legal structure or an intermediate structure are taxed at a flat rate of 30%, unless and insofar:

- the distribution stands for contributions made by the founder (this exception remains unchanged), or

- the distribution results from income that has effectively been taxed in Belgium.

Income that is not taxable in the Belgian Income Tax Code has not effectively been taxed. The same goes for income that is exempted pursuant to the Belgian Income Tax Code or a double tax treaty.

This new rule also applies to accumulated profits.

The new rules on taxation of distributions will apply upon the making of a distribution by a legal entity that qualified for at least 1 of the 3 previous tax years as a legal structure. Appropriate timing should be considered in this regard.

Example:

An individual Belgian tax resident is the founder of a BVI

company (legal structure). The founder contributes a securities

portfolio with a value of € 10 million into the legal

structure.

In year 3, the BVI company sells the securities portfolio with a

capital gain of € 2 million. The look through tax is

applicable. The founder is not effectively taxed. The gain

qualifies as realized within the normal management of private

assets.

In year 4, the BVI company distributes the proceeds of € 12 million to the founder.

Under the current legislation, no tax will be due upon the distribution of € 12 million: € 10 million stands for the contribution by the founder and € 2 million results from a capital gain that has been subject to tax in Belgium.

Under the new rules, € 2 million is taxed at the flat rate of 30%: € 10 million stands for the contribution by the founder and € 2 million results from the capital gain that has not effectively been taxed in Belgium.

5. What is the introduction of fictitious distributions about?

The undistributed profits of the legal structure are deemed to be distributed to the founder, upon:

- the contribution of the economic rights, shares or assets of the legal structure into another legal structure or legal entity, or

- the transfer of the legal structure to another jurisdiction than Belgium.

The undistributed profits are taxed at a flat rate of 30%.

Example:

If the founder contributes his (or her) shares of the BVI company (legal structure) into a Luxembourg company, the legal structure is deemed to have distributed its undistributed profits to the founder. The founder will be taxed on said profits at the flat rate of 30%. Upon contribution of the shares into a Belgian company, no tax is due.

6. What is the introduction of the exit tax upon emigration of the founder about?

Upon emigration of the founder, the undistributed profits of the legal structure are deemed to be distributed and are taxed at a flat rate of 30%.

A so-called "mitigation" has been built in by providing for the possibility of staggered payment of the tax if conditions are met.

7. What does the substance carve out entail and what will change?

Under the current regime, the founder can provide evidence that the legal structure has sufficient substance. In such case, the look-through tax is not applicable. The legal structure should however still be reported in the personal income tax return.

The new rules tighten the substance carve-out. The following conditions need to be fulfilled:

- The legal structure needs to be established in a country that has entered into a double tax treaty or an agreement on the exchange of information relating to tax matters with Belgium;

- The legal structure needs to exercise a substantial economic activity, supported by staff, equipment, assets and buildings and needs to have the activity as the main source of its income;

- The substantial economic activity cannot have as an objective the management of the private wealth of the founder; and

- The exercise of the substantive economic activity must comprehend the offering of goods or rendering of services on a specific market.

The fourth condition is new and the second condition has been tightened. This tightening aims to counter the creation of minimum substance to fall under the carve-out by, for example, merely renting office space or hiring an employee.

8. What will change for founders investing in private investment funds?

Under the current regime, legal structures taking the form of public or institutional investment funds were excluded from the Cayman tax unless they were substantially owned by the founder and related persons (fonds dédié).

The new rules set a clear standard for substantial ownership by the founder and related persons of (compartments of) investment funds. The benchmark is set at a shareholding of more than 50%. If the shares in an investment fund are held for more than 50% by an individual Belgian tax resident (as the case may be, together with related persons), the investment fund qualifies as a legal structure (fonds dédié). The new standard applies for substantial ownership on private, public, and institutional investment funds.

Under the new rules, private investment funds established outside the European Economic Area are now excluded from the Cayman Tax, unless they qualify as a legal structure (fonds dédié).

Two rebuttable presumptions are introduced: an investment is presumed to be a fonds dédié if the fund's asset manager receives specific instructions or if there is no independent asset manager.

9. Is the Dutch foundation (STAK) a legal structure and, if so, what are the consequences?

According to the Minister of Finance, a STAK qualifies as a legal structure and should be reported in the income tax return of the founder. However, the income only falls under the look-through tax in case the certificates relate to shares of a legal entity which itself qualifies as a legal structure or if the conditions of Article 13 of the Law of 15 July 1998 are not met.

Consequently, the STAK that certifies shares in accordance with the Law of 15 July 1998 qualifies as a legal structure that must be reported but its income is out of scope of the look-through tax. Please note that this is a position of the Minister of Finance but is not written down in the law.

The Law of 15 July 1998 equates the certificates with the underlying securities. The income of the underlying securities is attributed to the certificate holder. Therefore, there can be no distribution of income. Certification and decertification are tax neutral. The neutrality is confirmed in the Explanatory Memorandum.

10. What are the current reporting requirements and what will change?

Under the current regime, the following data must be reported in the income tax return of the founder:

- Name and first name of the founder;

- Full name of the legal structure;

- Legal form of the legal structure;

- Address of the legal structure; and

- Identification number of the legal structure.

Under the new rules, the information that must be reported is extended allowing the Belgian Tax Administration to better verify the correct application of the Cayman Tax. In this respect, the income derived by each legal structure must be reported in an annex to the income tax return. The annex must include the following information:

- The income received by the legal structure, as reported in the income tax return under the look through approach;

- The value of the assets of the legal structure at the end of the taxable year;

- The portion of the assets contributed by the founder;

- The dividends distributed by the legal structure or the intermediary structure;

- The deemed dividends (fictitious distributions);

- The exempted dividends (exempted distributions); and

- The dividends (distributions) that are not declared in the tax return due to the Belgian withholding tax.

11. When will the amendments enter into force?

The amendments will enter into force as from income year 2024 (assessment year 2025)

The new reporting requirements will enter into force as from income year 2023 (assessment year 2024) which implies that the extended reporting obligation already applies for personal income tax returns to be submitted in 2024.

Two Specific Anti-Abuse Rules brought in line with EU Law

The Program Law amends two Specific Anti-Abuse Rules (SAAR) in the Income Tax Code, notably a specific rule dealing with the deductibility of payments made to tax havens as well as a specific rule for the transfer of certain assets to tax havens. These changes are made against the background of the "SIAT" judgement (C-318/10 dd. 5 July 2012) of the Court of Justice of the European Union (CJEU).

1. Which SAARs are envisaged and why are amendments being proposed?

The Belgian Income Tax Code includes a SAAR on the basis of which certain payments (notably including interest, certain royalties and service fees) are treated as non-deductible for tax purposes if they are paid to a non-resident taxpayer (or foreign establishment) if the latter is either (i) not subject to any income tax or (ii) subject to a "significantly more advantageous tax regime" for the relevant income as compared to Belgium. Such expense may nevertheless be deductible if it is demonstrated that the payment relates to real and genuine arrangements and does not exceed normal limits.

In the SIAT-case, the CJEU considered that this SAAR requires the Belgian taxpayer to provide proof that all the services rendered to non-resident taxpayers are genuine without any objective criteria pointing towards abuse and without the tax administration being required to provide even prima facie evidence of tax evasion or avoidance. The CJEU also scrutinized the condition relating to a "significantly more advantageous tax regime" stating that it gives rise to uncertainty for taxpayers and contravenes the freedom to provide services. After this judgement, this article was in practice not applied anymore within the EU.

The Belgian Income Tax Code contains another SAAR that uses similar wording. This SAAR targets the transfer of shares, bonds, receivables or similar titles, certain IP and/or cash from Belgium to a non-resident taxpayer that is either (i) not subject to any income tax or (ii) subject to a significantly more advantageous tax regime for the relevant income as compared to Belgium. Such transfers are currently not opposable towards the tax administration (i.e. taxation can be imposed in Belgium as if the transfer has not taken place), unless it can be demonstrated that either (i) the transfer is made for genuine financial or economic needs or (ii) the Belgian transferor has received a countervalue that generates a normal effective tax rate in Belgium as compared to the situation existing prior to the transfer. Since similar wording is being used, the same compatibility issues with EU Law arise.

To bring both SAARs in line with EU Law, the Belgian legislator has narrowed the scope and improved the predictability of these rules.

2. What will change if in scope payments are made or assets are transferred to low or un-taxed non-resident taxpayers?

The scope of application of both SAARs is narrowed since the SAARs will only apply to certain payments made or assets transferred directly or indirectly to a related non-resident taxpayer (or a foreign establishment). The concept of being related is broadly interpreted: any lien of interdependence could be sufficient (e.g. a quasi-exclusive client-supplier relation), without formal legal ownership being required.

The Program Law further amends the counterproof that can be provided, which will be a two-step approach.

Firstly, the vague concept of "significantly more advantageous" is now more clearly defined: a tax regime is considered as being significantly more advantageous if it is demonstrated that the payment or transfer is made to an enterprise that is subject to an effective income tax that is less than half of the income tax due if the enterprise were a Belgian tax resident.

Secondly, the threshold for economic counterproof is more clearly defined and aligned to the wording of other anti-abuse rules in EU (case) Law. The SAAR will not apply if the taxpayer demonstrates that the payment or transfer is part of a genuine arrangement entered into for valid commercial or economic reasons that reflect economic reality.

3. What will be the expected impact?

The amendments make clear that payments or transfers to unrelated non-residents do not fall into the scope of these anti-abuse rules. In these circumstances, taxpayers are no longer burdened with a disproportionate counterproof. For payments and transfers to related non-residents, the minimum taxation threshold and the counterproof requirements are more clearly defined, although the burden of proof remains with the taxpayer. It is therefore recommended for taxpayers to maintain supportive documentary evidence of the commercial reasons underlying the transaction and/or of the tax status of the beneficiary. Although these measures were seldomly applied in practice so far, it can be expected that the Belgian Tax Administration will now more easily rely on these rules, even within an EU context.

Note that other deduction limitations and reporting requirements for payments to tax havens remain fully in place and are not amended.

4. When will the amendments enter into force?

These amendments will enter into force as of 1 January 2024 with respect to payments made/attributed or transfers performed as of that date.

Additional tax for Specialised Real Estate Investment Funds ("FIIS/GVBF")

The legal framework for a Belgian Real Estate Investment Fund (REIF – Gespecialiseerd Vastgoedbeleggingsfonds / Fonds d'Investissement Immobilier Spécialisé) was introduced in 2016 and has proven its merit as investment vehicle in the Belgian real estate market.

A REIF is a closed-end fund with fixed capital that exclusively invests in real estate and that is only available for institutional and professional investors. The REIF must register itself on a list maintained by the Ministry of Finance, which also results in the application of a special REIF corporate income tax regime consisting of a limited tax base. In practice, this regime implies that the real estate income is in principle exempt from corporate income tax. If a normally taxed Belgian company (subject to 25% corporate income tax) is transformed into a REIF, an exit tax at the rate of 15% applies on all tax-exempt reserves and latent capital gains underlying the assets (notably the real estate) of the company. In other words, the real estate is deemed realized for tax purposes at the moment of the transformation and taxed at a separate 15% rate. This exit tax also applies in case of certain reorganizations (e.g. merger of an ordinary company into the REIF or the contribution of real estate into the REIF against the issuance of shares).

The Belgian legislator now aims to tackle structures whereby a company would first transform into a REIF making any untaxed reserves and latent gains taxable at 15% and would subsequently re-transform into an ordinary company (no longer having untaxed reserves and/or latent capital gains) or liquidate the REIF. By doing so, a 10% tax saving is realized by applying the 15% exit tax rate as opposed to the 25% standard corporate income tax rate.

To counter such types of potential abusive structures, an additional 10% tax will be levied if (i) the REIF is not maintained as a recognized REIF for an uninterrupted period of at least five years, or (ii) shares obtained from a contribution into a REIF are not maintained for an uninterrupted period of at least five years. The tax is calculated on the value determined upon registration.

These changes enter into force as of 1 January 2024 and apply to situations in which as of 1 January 2024 the five-year requirement is not met. Contrary to general anti-abuse rules, this new anti-abuse rule does not allow for counterproof (e.g. economically genuine reasons for re-transforming out of the REIF regime within five years). REIFs should thus be vigilant for this rule when assessing future reorganizations.

Increased registration duties on long-term leases and rights to build

The rate of registration duties on long-term leases and rights to build will be increased from 2 to 5% as from 1 January 2024. More in particular, the new rate will be applicable to authentic deeds on long-term leases and rights to build signed on or after 1 January 2024 (unless a private deed was signed earlier) and private deeds on long-term leases and rights to build signed on or after 1 January 2024. The reduced rate of 0.5% for the long-term leases and rights to build acquired by a (international) non-profit organisation remains.

Annual tax on credit institutions, collective investment undertakings and insurance companies

The annual tax on credit institutions, collective investment undertakings and insurance companies is currently for 80% treated as a disallowed expense for corporate income tax purposes. As of 1 January 2024, this annual tax will fully be treated as a disallowed tax expense.

In addition, the tax rate will increase with respect to the annual tax on credit institutions. Credit institutions are subject to this annual tax since 2016. The tax base consists of the average amount of the debts to clients in the year preceding the fiscal year. The Program Law increases the rate of this tax to 0.17581% for the portion of the tax base exceeding EUR 50 billion. The rate to be applied for the portion of the tax base not exceeding EUR 50 billion remains unchanged, i.e. 0.13231%.

Credit institutions and their branches may not recharge the cost of this tax to their clients, but to date no sanction is applied if this rule is not complied with. The Program Law therefore also introduces a fine, which cannot be recharged to the clients either. The fine ranges from 10% to 200% (to be established by Royal Decree) depending on the repetition of the offense. The fine is calculated on the tax due for the assessment year to which the recharged tax or fine relates.

The increase of the rate and the introduction of a fine enter into force on 30 December 2023.

Expansion of and limitation to flex jobs scheme

The flexi-job scheme is a form of employment in certain sectors whereby the employer only pays an employer's contribution of 25% of the remuneration of the flexi-employee. The latter does not have to pay social security contributions or taxes.

The main condition for hiring an employee under a flexi-job scheme is that the employee must already be working at least 4/5 of a full-time equivalent for one or more other employers. However, retirees who can be hired under the flexi-job system do not have to fulfil this condition.

The Program Law extends the scope of the sectors eligible for the flexi-scheme but also makes amongst others the following changes to this flexi-scheme:

- The employer's contribution will be increased from 25% to 28% for remunerations awarded as from 2024.

- The tax exemption for flexi-employees will be limited to EUR 12,000 per taxable period. Above this threshold, flexi-employees will be taxed at progressive rates. This maximum amount is prorated if the taxable period is less than 12 months. The tax exemption for retirees will remain unlimited. This limitation will enter into force as from assessment year 2025.

Fiscal work bonus increased

The fiscal work bonus is a reduction of the personal income tax for low-wage employees entitled to a reduction in the amount of social security contributions (so-called social work bonus). The reduction of the personal income tax is calculated as a percentage (i.e. 33,14%) of the social work bonus with a certain cap (i.e. non-indexed amount of EUR 550). The aim of the social and fiscal work bonus is to guarantee these workers a higher net wage, without increasing the gross wage. In this way, the aim is to widen the gap between the lowest wages and unemployment allowance and thus reduce unemployment traps.

The Program Law now increases the cap of the fiscal work bonus to a non-indexed amount of EUR 710 for assessment year 2025 and EUR 765 for assessment year 2026. In addition, the above-mentioned percentage of 33.14% is increased to 52.54% but only for the lowest wages.

VAT and excise duties

1. What VAT changes do businesses need to prepare for on

the eve of 2024?

With regard to VAT, the budgetary measures announced at the end of 2023 are less ambitious than what was expected from the tax reform announced at the beginning of the year. While most of the measures announced will see their entry into force postponed (see below), two provisions will come into force on 1 January 2024.

1) harmonization of reduced rate schemes for the demolition and reconstruction:

There are currently two distinct reduced rate schemes for demolition and reconstruction in Belgium. Both provide for a reduced VAT rate of 6% but differ slightly in their scope of application. The first is a permanent measure geographically limited to 32 urban areas, while the second is a temporary measure that applies to the rest of the national territory but include specific 'social conditions' (i.e. the building must be rented out as a residential building under a management mandate granted by the project owner to a social real estate agency or a social housing company recognized as such by the competent authority).

As of 2024, the 6% VAT rate will apply across the whole country to the demolition and reconstruction works of a building located on the same cadastral parcel and intended for the housing of the natural person project owner (but no longer on the subsequent sale of the rebuilt housing) or which falls under the social conditions.

The application of this reduced rate is, however, subject to a number of strict conditions, including conditions relating to:

- the building itself, i.e. its usage and surface area after completion of the works, and

- a series of formalities to be completed by the project owner and the supplier.

As a result, the scope of the reduced rate applicable to demolition and reconstruction has been considerably reduced and real estate developers, investors and multiple-owners hence are generally excluded from the new scheme.

A transitional period is also foreseen to allow the move from the two separates schemes to the new harmonized regime.

2) a one-year extension of the reduced rate for the installation of heat pumps:

In response to the energy crisis caused by the invasion of Russian troops on Ukrainian territory, the current measure establishing a reduced VAT rate on the supply of heat pumps is extended for an additional year in support of households.

Nevertheless, the coming years are shaping up to be quite turbulent in terms of VAT. Here's a summary of what can be expected:

- new functionalities of the VAT current account, among other designed to improve the management by VAT taxable persons of their VAT balances and VAT refund processes, are due to come into force in 2025,

- the entry into force of e-invoicing obligations, as initiated at the EU level, has been postponed and should be phased in gradually from 2026, and

- a general overhaul of reduced VAT rates was also announced in the frame of the tax reform. If it is no longer on the political agenda, it may well take place during the next legislature. In a nutshell, the announced project would be to replace the current reduced rates of 6% and 12% by a single reduced rate of 9%, except for certain utilities (for domestic use, like energy and tap water supplies) that would remain subject to the 6% rate. A new reduced rate of 0% would also be introduced for goods of first necessities like fruits and vegetables, medicines... The standard rate of 21% would continue to apply.

2. What changes in relation to excise duties do businesses need to prepare for as from January 2024?

As of January 1, 2024, e-liquids and novel tobacco products like heated tobacco products will become excise products and will be subject to the same rates as other tobacco products. This extension of the tobacco excise law aims to adapt the excise framework to new trends in the market and the evolution of tobacco products. Like other Member States, Belgium already subjects these products to excise duties in anticipation of a revision of the Tobacco Directive 2011/64/EU.

The excise duty on e-liquids applies to any liquid intended for use in an e-cigarette or that can be used for refilling. Both nicotine-containing and nicotine-free liquids are included. The excise duty is levied per milliliter of liquid. Aside from creating a new excise product, the excise tax on tobacco products will be increased.

Businesses operating in the vaping industry will be required to obtain a license, file excise duty declarations and affix a tax stamp to these excise products before releasing them for consumption.

Questions?

These new budgetary tax measures may have an impact on the tax position of many Belgian taxpayers. Some aspects are rather complex and will require a case-by-case analysis. Should you have any questions, please contact the authors of this newsletter or your trusted Loyens & Loeff advisor.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.