Introduction

The modern trust and estate practitioner has a wealth of vehicles at his/her disposal, each with varying degrees of sophistication, to address the needs of both international and local clients. Traditionally, the use of trust structures, such as a discretionary trust, has formed the backbone upon which practitioners have crafted bespoke solutions to meet client needs. With the passage of time, relatively new solutions, such as private trust companies and non-charitable purpose trusts, which can offer clients (in some respects) a greater degree of asset protection and financial privacy, have evolved.

However, no matter how well structured an estate planning solution may seem, the era of "secrecy" has come to an end. Today's landscape has been irrevocably altered due to the introduction of stronger compliance policies and reporting requirements spurred on by governments seeking to claw back lost tax revenue. The push for stronger compliance regulation and reporting is also due in part to the need to limit the avenues available for individuals to launder money.

It is in this light that we must go forward and rethink the concepts of financial privacy that were the hallmarks of the profession a decade ago. Today's market is one where the client's needs must be tempered with managing expectations as to what is feasible.

Rather than viewing the changing tides as a storm to be weathered, practitioners should focus instead on innovating and reimagining the possible applications of current estate planning instruments whether in conjunction with newer structures or as stand-alone solutions.

Compliance Issues

As mentioned above, the unavoidable reality of today's environment is that regulatory bodies now require a great deal of information about not only the "ultimate beneficial owners " but also background information on the settlor if (s)he should be different. Furthermore, with the growth of TIEAs and tax exchange agreements, it has become imprudent for clients to hold the belief that they can dodge the tax bullet by transferring funds offshore. Statutory provisions and regulatory policies, which require that financial institutions provide reports to oversight bodies ("Reporting Requirements"), are now entrenched. It is true that these Reporting Requirements provide a means by which the regulating authority can ensure that the vehicle is validly created and administered in accordance with the rules of the governing jurisdiction, however, it is also self-evident that they now form part of the sieve by which foreign governments are able to discourage the use of tax avoidance vehicles. Foreign governments are also seeking out those individuals and businesses who would try to aggressively mitigate or circumvent the tax laws of their home jurisdiction.

This fact is readily exemplified by the advent of automatic exchange of information legislation such as the US Foreign Account Tax Compliance Act ("FATCA") and the inevitable introduction of the Common Reporting Standard. These standards place financial institutions under stringent obligations to carry out know your client ("KYC") measures to ensure accurate reporting compliance. Under the FATCA regime, failure to report accurately comes with a heavy penalty of a 30% withholding tax on a financial institution's US source of income.

Much has been written about the impact that compliance regulations will have on the private client industry and it is not the intent of this paper to rehash the same point. What is of importance though is the recognition that even though clients will in many cases no longer be able to take advantage of the same tax savings that were available in the past, they will still be able to avail themselves of the asset protection benefits inherent in the structures discussed in this paper.

These requirements pose a host of challenges to potential clients and settlors who seek to take advantage of the financial privacy features inherent in trust structures.

FATCA was enacted to de-incentivize United States tax residents from taking advantage of foreign structures so as to evade tax. It has also acted as a further stimulus for other jurisdictions to implement legislation similar to FATCA, such as GATCA in the United Kingdom.

Turning now to the Common Reporting Standard, this particular scheme was designed by the Organization for Economic Cooperation and Development ("OECD") so as to obtain financial information of account holders. The information to be exchanged would effectively do away with a large swathe of the privacy to which clients had been accustomed in relation to the government and themselves. It should be noted that the information exchanged should not become part of the public domain, and as such the confidentiality that has always existed between the client and the general public will be maintained. However, the greatest threat to this protection would be the misuse of information collected by governments whose data protection procedures are not as secure as those of the transferring country.

In light of the oncoming changes to required compliance and reporting standards, privacy can no longer be looked at from the view point of the client keeping the world at large away but instead the client keeping the general public from knowing the details of his/her estate planning activities.

With this in mind, the following vehicles can provide clients with the opportunity to manage their assets in a sophisticated and cost effective manner.

Private Family Funds

In the Bahamian context there are a number of options for structuring private family funds, such as the ICON, trust, or through a corporate entity. One of the more popular structures used by clients for private family funds in the Caribbean is the Bahamian Specific Mandate Alternative Regulatory Test Fund ("SMART Fund"). SMART funds come in seven different permutations, each with its own structure geared towards a different type of investor. In particular, a category four SMART fund allows wealthy families to consolidate complex cross jurisdictional assets into a flexible investment structure while limiting the investor pool to a maximum of five participants.

This vehicle is excellent when used in conjunction with other wealth management structures so as to ensure constant and effective valuation of assets held while imposing structure in relation to how such assets should be pooled to achieve greater returns.

The process of creation is relatively easy because investors need only fill out a term sheet rather than a prospectus and this vehicle marries the flexibility and feature set of a traditional hedge fund structure with the ease of creation and use found typically in small investor focused products.

We can anticipate that taxing authorities will become more and more aggressive, and that as a consequence, professional funds will become more popular. External investment banks do not subject professional funds to the same compliance requirements as private investment companies, although an administrator is required to obtain KYC on any investor. Such funds also benefit to a greater extent from pooling, e.g. negotiation of fees, access to information and group experience.

Single Family Private Trust Companies

Private trust companies (PTCs) offer clients a greater degree of flexibility and control in relation to the management of trust structures than institutional trustees. A major advantage is that the client can use the PTC as a holding structure for multiple family businesses and assets which may not be feasible for an institutional trust company.

This flexibility to create bespoke solutions particular to the needs of the client is exemplified in the PTC's corporate entity structure. The client has the potential to decide who will act as the directors of the board in control of the PTC. This option allows the client the opportunity to appoint trust associates or family members who would have a more intimate understanding of the client's intentions and/or how the assets under their stewardship should be handled. Finally, should it be desirable to change a member of the board the client is able to influence a change in the board or the investment policies of the PTC.

This structure effectively removes the need for an institutional trustee in the traditional sense but an institutional trustee often provides back end administrative assistance. In addition, institutional trustees can provide the structure with experienced guidance e.g. by its officer(s) acting as director(s).

A PTC has the added benefit of generational planning given that the corporate documents of the PTC will establish how it should be run. This customization can be further augmented through the use of a family constitution that governs how the different share classes and their respective holders interact with each other and with the company itself. This has the advantage of not only clearly establishing the rules regarding the division of assets and how family members are able to enter and exit the governance of the PTC but also the mechanisms by which members can resolve disputes.

Finally, a PTC can shield its owners from possible unlimited liability in the event of bankruptcy or insolvency. This has the added benefit of protecting the settlor from third parties who would first have to pierce the corporate veil in order to establish a connection between the settlor and the PTC.

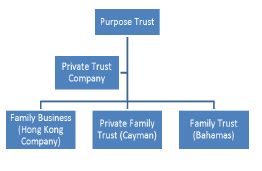

Purpose Trusts

Purpose trusts are excellent standalone tools for settlors to create a vehicle that is free of certain constrains which are normally applicable to a discretionary trust. The most distinct feature of a purpose trust, which is absent from other non-charitable trusts, is the fact that it can be created to fulfil a beneficial purpose rather than to benefit a specific beneficial class. This particular attribute affords the purpose trust protection from the principles of Saunders v Vautier. Thus settlors of purpose trusts can benefit from the knowledge that not only will the intended beneficiaries be unable to bring an end to the trust, they will be protected from third parties seeking to gain access to their potential benefits under the trust. This is due to the fact that the assets of the purpose trust will never vest in a potential beneficiary until it has been distributed to such beneficiary.

To ensure that the purpose trust is run in the manner the settlor intended, an Enforcer is usually appointed to give effect to the settlor's wishes. The settlor can appoint a trusted associate to carry out this role so that the settlor can maintain a sufficient degree of separation from control of the purpose trust in order to avoid relevant tax authorities attributing the assets to him for tax assessment purposes.

A purpose trust is also free from the rule against perpetuity, which allows it to take on the possible role of a dynasty style trust vehicle. A practical disadvantage of a purpose trust, is that like other orphan structures, it can prove difficult to satisfy the compliance requirements of banks.

Corporate Entities

Corporate entities provide a different mechanism by which a practitioner is able to provide estate planning solutions. For example, a corporate entity can have two different share classes, one class, A, carries with it all of the voting rights and the other class, B, carries with it all of the rights to dividends. By means of this arrangement, the client can retain control of the voting shares while a trustee holds the other class of shares.

In this way the settlor can retain control over how the assets are used and distributed while the beneficial interest remains in the hands of the trustee who then apportions out said interest in either a discretionary or express manner.

This solution has many of the same benefits inherent with the PTC while lacking the same level of flexibility or complexity. One distinct advantage that it does possess comes from the unique concessions afforded to special types of corporate entities. For example, Cayman Islands exempted limited companies and Bahamian International Business Companies are exempt from certain taxes for a specific period of time.

Another structure which can substitute for a trust and which has been used for many years, especially in the Isle of Man, is the company limited by guarantee. Whilst there are many permutations on its use, typically a division of control and benefit is achieved through a variation in the rights attached to the members of a company.

Many Vehicles One Purpose

Each of the vehicles mentioned above may be used in isolation to achieve the goals of the settlor. However, they can also be used to complement each other so as to address the varying needs of clients.

A good example of such a structure is a PTC controlled by a purpose trust and used as the holding company for underlying trust and corporate structures. Although potentially complex, this arrangement exemplifies the numerous options available to clients to structure their wealth planning solutions.

Conclusion

While clients may continue to press practitioners for structures which are tax driven, practitioners must be mindful of the new global regulatory regime in which we operate. In doing so, we as practitioners must focus our attention on explaining the benefits from a structuring and an asset protection stand point while re-educating clients on what is now feasible. In some instances a trust may not be the ideal vehicle and in others it can be more than adequate for the purpose. It is also important to remember that no matter how well designed a structure is, its administration will be the determining factor in whether it can withstand challenges from beneficiaries or third parties.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.