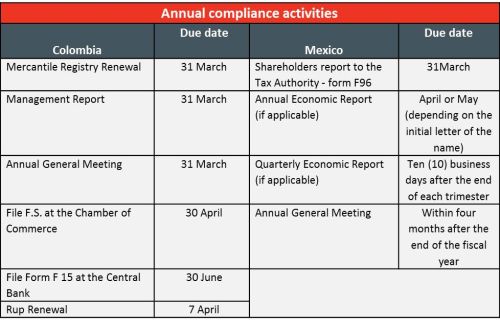

Every year companies must comply with local mandatory activities in order to fulfil legal requirements. Our local experts explain the main activities in Colombia and Mexico.

The annual compliance activities in Colombia are:

- Mercantile Registry Renewal

at the Chamber of Commerce

In the Mercantile Registry merchants must report personal, professional, economic and financial information to the Chamber of Commerce. The Mercantile Registry makes the merchant status public and legal, and allows third parties to obtain information about particular commercial activities. This report must be completed by 31 March. - Management

Report

This is a brief description on the previous year's operation including income, expenses, as well as company objectives for following year. The report is created and signed by the Legal Representative of the company. - Annual General Meeting

(AGM)

At the annual general meeting, the general manager and board of directors (if there is one), submit the financial statements and reports for the previous fiscal year to the shareholders for approval. Once the financial statements are approved, the shareholders determine the allocation of the company's distributable profits for the preceding year. The AGM should be done by 31 March each year. - File F.S. at the Chamber of

Commerce

Financial statements must be prepared in accordance with the Colombian GAAP, which is issued by the Technical Council for Public Accounting. Financial statements include the balance sheet, the income statement, the statement of changes in equity, the statement of changes in financial position, and the cash flow statement. This must be submitted to the Chamber of Commerce by 30 April (one month after the AGM is celebrated). - File Form No. 15 at the

Central Bank

Also known as "Equity Reconciliation – Companies and Branches of the General Regime," the F15 is presented to the Foreign Exchange Department of the Central Bank after they have held the annual general meeting. The F15 reports the shares or quotas for the year corresponding to the issuance of the shares and must be submitted electronically by 30 June. - RUP Renewal

The Single Proponents Listing (RUP) is a listing where every individual or legal person must report its legal, financial and organizational standing, and classification – if it wants to undertake agreements with State entities. This applies to domestic and foreign persons, or a branch office in the country. Due date is the fifth working day of April, this year it is 7 April.

The annual compliance activities in Mexico are:

- Shareholders report to the

Tax Authority - form F96

Form F96 is presented to the Tax Administration Service (SAT) when a Mexican company has shareholders / foreign partners with no Mexican Tax ID (RFC) – which means they don't pay taxes directly in Mexico. The form must be submitted by 31 March each year along with the Annual Statement. It should contains the name, address, nationality and additionally for 2016, the Tax ID where each shareholder / partner is taxed. - Annual Economic Report (if

applicable)

The Annual Economic Report must be submitted by those who meet or exceed $110,000,000 Mexican pesos in any of the following items: Active Total (initial and/or final), Total Liabilities (initial and/or final), income (in the country and abroad) or outflows (in the country and abroad).

The report is presented before the National Registry of Foreign Investments and in accordance with the following schedule (letter with which the name of who submits starts):

- Letters A to J, during April of each year

- Letters K to Z, during May each year

- Quarterly Economic Report (if

applicable)

The Quarterly Economic Report is required by the National Registry of Foreign Investment (RNIE) when amounts equal or exceed $20,000,000 Mexican pesos in the following three areas:

- Where there are new contributions or withdrawals that do not affect capital; or

- Where retained earnings of the last fiscal year and disposal of accumulated retained earnings are in existence; or

- Where there are payable or receivable loans to: resident subsidiaries abroad; the parent company abroad; resident foreign investors abroad participating as partners or shareholders; and resident foreign investors abroad who are part of the group to which the physical person, foreign legal entity or Mexican company that presents the report belongs to.

Modification notice:

Quarterly compliance obligations include keeping the corporate information updated in the following cases:

- Any amendment to the presenter name or denomination, legal address or social activity or object must be reported without exception.

- Any amendment to capital (increases or decreases) or to the stock or corporate structure in an amount (equal or greater) of $20,000,000 Mexican pesos must be reported. In case of notice of modification to the stock or corporate structure, supporting documentation must be attached showing the amount of the transaction (e.g. Contracts).

- Annual General

Meeting

In Mexico, the annual shareholders' meeting must be held within four months after the end of the financial year. During this meeting the ending fiscal year financial statements get approved, rejected or modified. Also, the sole administrator or Board of Directors and Statutory Auditor – who prepares a report on the company's year-end financial information and examines the company's books and records – are selected.

Failure to comply with all of the filing requirements may result in the imposition of penalties and loss of good standing.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.