Why a Private Trust Company (PTC)?

Over the last decade professional trustees in offshore jurisdictions have become far more cautious in the way they exercise their powers. This is for two reasons. Firstly, as trusts mature, there have been a number of actions against trustees by creditors, beneficiaries and settlors, which have highlighted the trustees’ duties to these parties and the consequences of following the settlors’ instructions blindly without considering the other interested parties. Secondly, there have been a number of mandatory guidelines issued by regulatory authorities detailing how the responsibilities of trustees should be fulfilled.

The result of these developments is that where a trust has been set up to hold assets other than a simple investment portfolio, for example the family business or the family home, the simplest transactions become complicated as the trustee seeks legal advice and/or indemnities from beneficiaries and potential beneficiaries. Trustees are reluctant to make new investments in non standard assets.

Furthermore, another trend is for wealthy families to take more control over the management of their wealth by establishing family offices which look at all aspects of wealth management and inheritance planning for the family.

What is PTC?

The Private Trust Company has evolved to cope with these trends. A PTC is a company formed to act as trustee to a limited number of trusts, either for the benefit of a single family, or for the benefit of different branches of a family or for distinct (but related) family groups. In this way, the PTC takes on the trusteeship of the various family trusts and act as the registered owner of their assets. The administration of the PTC is delegated to a Licensed Trust Company like Mauritius International Trust Company Limited (MITCO). It is the Directors of the PTC that carry out their duties on behalf of the company which will be the trustee of the trust/s. The Board of Directors may be drawn from the Settlor’s own family, his close advisers or others. We will normally recommend that at least one Director is provided by MITCO in order that we may fulfill our duties under the law but also provide practical and technical advice to the Board.

Whilst a PTC is administered by a Licensed Trust Company, it is not owned by that company and may be directed by family members or other professional advisors. It can therefore be more flexible in taking investment decisions and will probably be run by people with a more complete understanding of the families needs. It can also allow members of succeeding generations to sit on the Board and take part in running the family business.

The question arises though as to who will own the PTC if not the Licensed Trust Company. If it is to act for the trusts of a group of closely related families, then which representatives of those families should own the company? What will happen when one of those members dies? If the trusts have been established for fiscal objectives, will those be met if the settlor owns the trustee of those trusts?

Purpose Trust

For the "control" reasons referred to above, some families are reluctant to actually "own" the PTC which they will be using to manage the family trust or trusts. The answer to this question is that the shares should be held by a Purpose Trust established by the licensed Trust Company with the sole purpose of establishing and holding the shares in the PTC.

A purpose trust may be established under the Mauritius Trusts Act 2001 if it is to fulfill a purpose that is specific, reasonable and capable of fulfillment. The life of a purpose trust is limited to 25 years in Mauritius but there is nothing in the law to prevent a successor trust being established.

The trust deed will usually make provision for the appointment of an enforcer, which is a role that is similar to that of the protector. However, the appointment of an enforcer to enforce the trust and provide for the appointment of successors is not a requirement in purpose trusts as the statute gives the settlor, a trustee, or any person with a sufficient interest in the trust, the power to make application to the court to enforce the trust.

Incidentally, the Purpose Trust, in combination with a company wholly-owned by such a trust, can provide the means by which bankruptcy remoteness can be achieved, while enabling the transaction to be effected "off balance sheet" or as an "orphan" structure in relation to its originator. Purpose trusts have been used in conjunction with asset financing transactions and securitisations as well as private trust companies. For example, the purchase by a specially incorporated company of a ship or aircraft with finance provided by a lending institution. They are particularly popular in credit enhancement and in financing transactions.

In its commercial role, the trust is established for the purpose of acquiring and holding the shares of the company, which is to engage in particular transactions.

The trust deed can specify that the Enforcer has the right to remove and replace trustees. The trustee will, as sole shareholder, have the power to appoint and remove directors of the PTC. The terms of the trust can require that he only exercises this power with the consent of the enforcer.

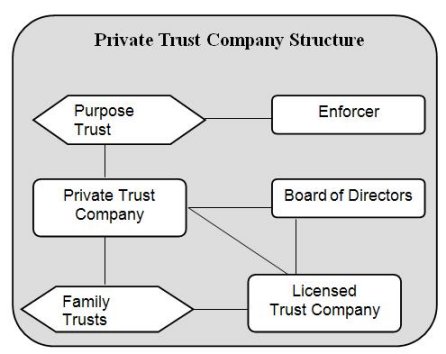

The PTC Structure

The structure is illustrated below:

There is no public register of Directors or Shareholders of the PTC in Mauritius and there is no requirement for registration of the individual underlying trusts. However, the PTC is required to provide a list to the Financial Services Commission annually of the trusts for which it acts.

The Financial Services Commission is very clear that the responsibility for ensuring compliance with the terms of the licence rests with the appointed Licensed Trust Company.

Conclusion

The establishment in Mauritius of a PTC owned by a purpose trust provides a flexible and cost effective basis for administering a group of family trusts whether those trusts are domiciled in Mauritius (to take advantage of Double Tax Treaties) or in other jurisdictions. The level of control by the settlor can be adjusted according to individual circumstances and philosophy. Of course, the balance must always be found as between retaining as much control as possible (as described above) and risking attack on the grounds of sham or even that the trust income should be taxed in the settlor’s country of residence as he effectively "manages and controls" the whole thing from that jurisdiction. In our experience, the right balance can usually be found.

Mauritius is a business-friendly and stable financial centre offering the established & flexible legal framework for setting up and administering PTC and non-resident trusts.

Mauritius International Trust Co. Ltd (MITCO) is licensed and regulated by the Financial Services Commission of Mauritius since 1993 to provide a complete range of trust, tax and wealth management services to international investors. We have built up considerable expertise in advising clients on global trust and estate planning, business succession and administration of trust (including PTCs).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.