Introduction

Maitland once wrote: '[O]f all the exploits of Equity the largest and most important is the invention and development of the Trust. It is an institute of great elasticity and generality; as elastic, as general as contract. This perhaps forms the most distinctive achievement of English Lawyers.' Indeed, the trust concept which finds its inception in England in the Medieval times and started as a means to circumvent feudal rigidities, has across the centuries transformed itself into one of the most useful and flexible tools for practitioners, the use of which is multifold.

The basic idea behind the trust lies in the fact that the management and enjoyment functions of ownership are split between different persons. The role of management is vested in the trustee whilst the enjoyment of the thing subject to the trust is vested in the beneficiaries. To do this, a settlor will transfer the legal title of his property in a trustee who will hold it and manage it for the benefit of the beneficiaries. "Trust" in its literal sense is very much the basis of and underpins the relationship between the settlor and the trustee. It was thus typical that traditionally trustees would be people who were very close to the settlor, such as their advisors, close friends or family members. At the time, trusteeship was considered to be an 'act of great kindness' (see Knight v. Earl of Plymouth 1747) and was performed gratuitously.

"Trusting" Professional Trustees

The 20th century saw the development of trusteeship as a professional service and the introduction of the concept of corporate trustees or trust companies. There are a number of benefits to be gained by appointing an institution to act as trustee over an individual. A professional trustee can offer continuity, permanence, professionalism and investment expertise. Choosing a professional trustee also may help avoid the biases that may result when you select a family member. However this lead to other difficulties, principally that of settlors unwilling to give away control of the assets to an institution which effectively is a stranger. How does one reconcile the basis of the concept as being one based on "trust" to the giving away of one's assets to an outsider, the more so to a corporation which may be located in a foreign "offshore" jurisdiction?

Whilst it is true to say that practitioners and law draftsmen have been very creative in coming up with solutions to provide more comfort to settlors in the form of reserving power for settlers in the trust instrument or by inventing the position of a protector who may be given powers to sanction decisions made by trustees, both have their limits. On the other hand, the Private Trust Company (PTC) is a relatively new animal, but the last decade has witnessed a growth in its popularity because of its appeal to settlors and trustees alike.

What is a Private Trust Company?

The PTC in its simplest form is a company formed for the specific purpose of acting as trustee of a single trust, or a group of related trusts. However, a PTC does not generally require to be licensed as a fiduciary in its jurisdiction of incorporation, nor to meet the standard local capitalisation requirements for licensed trust companies, as it is deemed not to be carrying out business as a fiduciary. It therefore allows settlors to have their own "trust company" without having to go through the requirement of setting- up a licensed fiduciary business.

How the PTC resolves the dichotomy?

For years and years, the relationship between the client and the trustee could have been described as a tug-of-war, each pulling in opposite directions. On the one hand, the modern trustee with their office becoming more and more onerous is likely to adopt a prudential attitude in performing their duties fully aware of the possibility of being faced with an action for breach of trust by one disgruntled beneficiary. The office of the trustee can be better compared today to a minefield exposed to ever expanding and increasingly expensive litigation.

Then, the standard of care required of professional trustees as established by the eponymous rule in Bartlett v. Barclays Bank Trustee (1980), means that clients want the trustees to take rapid commercial decisions in relation to the trust's underlying assets whereas the professional trustee, fully mindful of their risks and potential liability, prefers legal advice before taking strategic decisions.

For the ageing settlor, the traditional trust structure does not allow them to empower children and pass control and influence over family business interests and wealth to the 'next generation'.

A PTC converges these contradictory interests by providing a means by which a settlor (or their family) can retain a greater degree of control over their trust affairs, having a 'hands- on' approach in the management of the affairs of the trust without compromising the validity of the trust structure and whilst providing enhanced protection for fiduciaries.

With a PTC, the settlor, members of their family or their advisors can be appointed to the board of directors and in this capacity they can influence the manner in which the trust is administered. The composition of the board can be changed from time to time to bring in members of succeeding generations. The company itself will generally be administered by a fiduciary in the chosen offshore location and which will be represented on the board.

Win-win situation

The PTC enables clients to control the trust without compromising the validity of the trust structure. The board also provides an opportunity to create a round-table forum. When the trust assets comprise of operating companies, the PTC is well-placed to take rapid commercial decisions concerning the management of the operating companies being able to draw on the specialist experience of its board members.

But over and above the mere issue of control or security, a PTC- unlike other techniques to address the difficulties with settlor control issues, enables family participation and can lead to the start of a 'family office' where all the client's financial affairs may be centralised. It provides a convenient way to pass control and influence over family business interests and wealth to the 'next generation' over a suitable period of time and in a regulated manner by bringing in designated successor(s) as director(s) of the PTC during the lifetime of the client.

By allowing a designated successor to participate in the affairs of the PTC during their lifetime, the settlor achieves the dual objective of allowing the successor to become familiar with the operations of the PTC, the underlying business and investment acti- vities, the way in which the structure is run allows but also to evaluate the suitability of their designated successor and aptitude to run the business.

The PTC as an 'umbrella structure' has a definite cost element where the assets are substantial, as the costs of maintaining the structure are likely to be less than the costs that would otherwise apply were the family trusts to be directly administered by a professional trust company.

The advantages of the PTC for the professional trust company should also not be underestimated. The trust company is unconcerned about the underlying assets of the trust or about the settlor exercising control as it is not providing trusteeship services. The trust company therefore bears no trustee liability and still gains a commercial advantage as it still provides corporate administration services to the PTC. There are no problems of conflict with settlor's or family's wishes as the trust company is not acting as a trustee and does not have to take decisions.

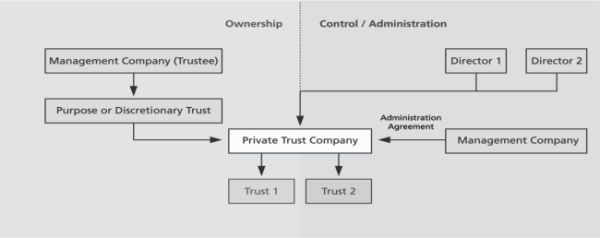

Ownership and governance

So, who should own the shares of the PTC? While there is no legal impediment for the client to own the shares of the PTC, it is generally thought to be undesirable that the ownership should have any link with the client, particularly if the client is from a civil law jurisdiction, as the shares do not then form part of their estate. Separating the ownership of the PTC also limits the possibility that the PTC may be held to be a sham.

There are various options regarding ownership including the use of a 'purpose trust' or 'purpose foundation' to hold the shares of the PTC.

The board of the PTC forms its backbone and choosing the right directors is crucial. One of the reasons for setting up a PTC is to provide a means by which a settlor (or their family) can retain a greater degree of control over their trust affairs. So the structure would ideally make provision for at least one representative of the settlor or their family on the board. Depending on the jurisdiction in which the PTC is set up, corporate directors may also be allowed. But, care should be taken not to have the majority of directors in a jurisdiction having CFC rules, as this may adversely impact on the taxation of the PTC trustee and hence on the residence of the underlying trust(s). Also the question as to who appoints directors has to be determined at the outset. Normally under most company legislations directors of a company may be appointed by ordinary shareholder resolution. But in the case of a PTC the appointment of directors could still be reserved to the shareholder purpose trust but the purpose trust deed could be drafted in such a way that at least one director shall be nominated by the protector of the trust - who may be the client himself.

Practical issues and pitfalls

Obviously, professional advisors and trustees should be wary of the pitfalls of setting up a PTC, but provided appropriate care is taken none of them are insurmountable. The perceived difficulties in the set-up are the sham argument, central management and control issues, and liability issues for the directors.

Sham

To avoid any possibility that the structure may be held to be a sham, there must be evidence that both the settlor and the trustee intended to set up a trust, the trust must have substance and the trust should be run as if it were to be treated as a trust. Therefore the role of the board of the PTC and how it operates becomes crucial to avoid the sham argument. However, the fact that the day-to-day administration of the PTC undertaken by a professional trust company minimizes the risk of the structure being held to be a sham.

Central Management and Control

Central management and control is another hazard for the unwary. As the residence of a trust normally depends on where the trust is administered and where the majority of the trustees are resident, care should be taken in not allowing the trustee PTC to become resident in another jurisdiction through the residence of the directors. This is because if the majority of the board of the PTC is resident in a jurisdiction having CFC rules, this may result in the PTC being controlled and managed in such a jurisdiction which would make the trust resident in that jurisdiction with adverse tax consequences. Therefore it is crucial that central management and control not only be seen to be from the jurisdiction of incorporation of the PTC but actually there. This goes beyond the mere fact of having a majority of directors resident there but involves the directors properly discharging their duties, understanding what they are doing, meeting to discuss and being aware of the company's business as opposed to acting as mere rubber stamps.

Dog-leg' claim?

Finally, the issue of liability of the directors of the PTC directly to the beneficiaries of the trust is worth looking at, especially in the light of the case of HR v. JAPT. On a strict application of company law, directors have to act in the best interests of the company. By necessary extension, directors of the PTC should not generally be liable for the acts of the PTC in its capacity as trustee. Even in the case where directors have breached their duty, the general rule is that duties imposed on directors are owed to the company and not to the shareholders. This is generally the case under most company legislations. Generally directors could be held liable if the court is willing to lift the veil of incorporation. The circumstances when this will happen are generally well settled from cases such as Adams v. Cape Industries (1991) and Trustor AB v. Smallbone (2001), namely where the company is a sham or when there is fraud. In the case of HR v. JAPT, there was an attempt to make the director of a trustee company personally liable to the beneficiaries. The judge held it was possible for directors of a trust company to be liable for the acts of the trust company in its capacity as trustee where they have procured or assisted in a breach of trust and/or on the basis of an indirect fiduciary and/or indirect tortious duty to the beneficiaries (a Dog-leg' claim). It would appear that the availability of such claims have been ruled out by the recent Jersey case of Sheikh Mohamed Ali M Alhamrani and Four Others v. Sheikh Abdullah Ali M Alhamrani and Four Others (2007) and the English case of Gregson v. HAE Trustees Limited (2008).

Choice of Domicile

Many of the prominent offshore international financial centres including Mauritius allow the setting-up of PTCs. Different rules apply to PTCs in each jurisdiction.

PTC Regime in Mauritius

It is worth noting that there is no specific legislation in Mauritius specifically relating to the PTC but the Financial Services Commission of Mauritius has advised that where a private company acts (as trustee) for a limited number of trusts for the benefit of a family or related family groups, rather than offering its services to the public in general, it will not be regarded as carrying on (trust) business in Mauritius and therefore, provided that it satisfies various safeguards, it will not, therefore, be required to be licensed under the Financial Services Act 2007 as a Corporate Trustee. The salient features of the Mauritius PTC Regime are as follows:

- A PTC can be set up either as a Category 1 Global Business Company (GBC2) or a Category 2 Global Business Company (GBC2)

- The PTC must be set-up by a licensed Management Company (MC)

- The PTC must adhere to conditions set out by the Financial Services Commission

- The PTC does not need to be licensed as a Corporate/Qualified Trustee

- THE PTC is required to:

- restrict its activities to that of private trust business services;

- at all times maintain a minimum paid up capital of US$5,000;

- provide its private trust business services solely to connected persons;

- not solicit trust business from, or provide trust business services to, the public;

- appoint a duly licensed Management Company to carry out its trust ad- ministration services in relation to any express trust to which it is a trustee;

- appoint the Management Company as Company Secretary;

- Adhere to the AML/CFT Framework.

Conclusion

As discussed above, there are now many compelling reasons for families to establish their own Private Trust Companies. PTCs allow them to involve their family members, advisors and institutions, all with the goal of providing fiduciary and other wealth management services to the family, through the family owned PTC. Additionally, the PTC provides the family with several advantages and benefits they could not otherwise attain. However, care should be taken in the way that the PTC is structured to avoid unwanted consequences.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.