The unique EU State aid control law requires, in principle, prior notification by Member States and approval by the Commission of all State aid. During a time of crisis, like the COVID-19 pandemic, EU law allows for a flexible approach for approving urgent State aid. In this post, we discuss the current state of play in the EU and offer some general items to consider for undertakings receiving State aid during this extraordinary time.

Crucial need for EU State aid control

The concept of EU State aid control is unique to the EU only (although more and more included by the EU in Free Trade Agreements with other regions). In a nutshell, this control consists of prior notification by the Member States and approval by the European Commission of all State aid, except for de minimis measures and aid covered by the so-called General Block Exemption Regulation, which does not currently cover most of the measures adopted under this COVID-19 outbreak. This control is combined with the parallel protection of subjective rights of companies and individuals by national courts in the event of violations of these procedural obligations by Member States. State aid control aims at achieving and safeguarding EU market integration. In other words, it remedies the destructive competition between EU Member States, often influenced by their natural sovereign and nationalist tendencies. Without State aid control, there would likely be no European Union!

Flexible approach in exceptional circumstances

In the event of exceptional circumstances such as the 2008-2009 financial crisis, the 9/11 disaster, or the 2010 volcanic ash aviation lockdown, EU State aid law allows for a flexible approach to State aid control. Indeed, on 13 and 19 March 2020, the European Commission adopted a series of measures implementing this flexible approach for approving urgent aid granted by Member States to companies (undertakings in EU law jargon) affected by the COVID-19 outbreak.

EU law offers two specific legal means to deal with these situations:

- State aid is automatically exempted "to make good the damage caused by natural disasters or exceptional occurrences" (the European Commission must approve these aid measures, without discretionary compatibility assessment provided that there is an "exceptional occurrence" causing economic damages – Article 107(2) b) TFEU); the European Commission has already clarified that the COVID-19 outbreak constitutes an "exceptional occurrence"; or

- State aid may be exempted under a discretionary compatibility assessment by the European Commission when the objective of the aid is "to remedy a serious disturbance in the economy of a Member State" (Article 107(3) b) TFEU is the legal basis, used only three times between 1958 and 2008 and then more than four hundreds times during the financial crisis).

EU State aid law also allows for traditional rescue and restructuring aid to save "firms in difficulty" under strict conditions (Article 107(3) c) TFEU). During the financial crisis, specific guidelines were adopted by the European Commission in 2009, which influenced the new 2014 guidelines for this type of exemption. The European Commission has not yet adopted "COVID-19 rescue and restructuring" guidelines but it is possible that it may do so in the future.

New measures adopted by the European Commission

On 13 March 2020, the European Commission adopted a coordinated response to counter the economic impact of the COVID-19 outbreak. On 19 March 2020, it also adopted a new State aid Temporary Framework valid until the end of 2020 (like the financial crisis temporary framework adopted in 2009).

What are the measures that Member States can adopt in line with EU State aid rules?

- State measures not constituting State aid (which do not need EU prior approval):

- public support measures available to all companies (no selectivity) such as wage subsidies, suspension of payments of corporate and value added taxes or social contributions, and support directly to consumers, for example, for cancelled services or tickets that are not reimbursed by the operators concerned;

- State aid to help companies cope with liquidity shortages and needing urgent rescue aid:

- measures to compensate companies for the damage directly caused by "exceptional occurrences", for instance measures in sectors such as aviation and tourism, hospitality and retail;

- Note that the Commission will require

that the Member States provide specific COVID-19 related data to

approve these automatically exempted measures:

- date of first case reported in the country;

- number of affected persons at the time of notification;

- economic impact of the COVID-19 outbreak in the Member State;

- sequence of (main) events between the occurrence of the COVID-19 outbreak and the adoption of the State aid scheme including any official recommendations or prohibitions decided by the competent authorities;

- detailed required information that were published for certain sectors, such as the aviation sector (identification of the additional costs, of the foregone revenues -loss of traffic, reduced demand-, variable costs, catering not incurred, reference period, reconstitution of damages caused by comparison of the situation during the period of spread of the COVID-19 and the reference period);

- rescue and restructuring aid: individual aid or schemes to meet acute liquidity needs and support undertakings facing financial difficulties, due to or aggravated by the COVID-19 outbreak;

- the new State aid Temporary Framework (19 March 2020) clarifies other types of aid measures which Member States can adopt to support enterprises affected by the COVID-19 outbreak (only companies which entered into difficulty after 31 December 2019 and subject to prior notification to, and approval by, the Commission are eligible):

- aid in form of direct grants, repayable advances or tax advantages (small size aid measures up to €800,000) to address urgent liquidity needs;

- aid in the form of guarantees on loans – measures more destined to large enterprises: (i) guarantee premiums set at a minimum level depending the recipient credit risk margin or (ii) aid schemes on the basis of this credit risk margin basis, but whereby maturity, pricing and guarantee coverage can be modulated (e.g. lower guarantee coverage offsetting a longer maturity); this type of aid will ensure banks keep providing loans to the business customers who need them to cover immediate working capital and investment needs;

- aid in the form of subsidised interest rates for loans: (i) loans granted at reduced interest rates (at least 1 year IBOR or equivalent plus the credit risk margins depending on recipient's credit risk margin), or (ii) aid schemes, on the basis of the credit risk margin, but whereby maturity, pricing and guarantee coverage can be modulated (e.g. lower guarantee coverage offsetting a longer maturity); these loans can help businesses cover immediate working capital and investment needs;

- aid in the form of guarantees and loans channeled through credit institutions or other financial institutions: measures building on banks' existing lending capacities, and using them as a channel for support to businesses/small and medium-sized companies; this type of aid is considered as direct aid to the banks' customers, not to the banks themselves;

- short-term export credit insurance: additional flexibility on how to demonstrate that certain countries are not-marketable risks.

In a matter of 24 or 48 hours following notifications, the European Commission has already adopted several decisions under the legal bases mentioned above:

- on 12 March 2020, a €12 m Danish scheme to compensate damages caused by cancellations of large public events due to COVID-19 outbreak;

- on 21 March 2020, a Danish €130 million aid scheme to support small businesses and three French aid schemes State guarantees on commercial loans and credit lines to companies that have up to 5,000 employees and State guarantees to banks on portfolios of new loans for all types of companies up to €300 bn of liquidity support);

- on 22 March 2020, an Italian €50 m aid scheme for the production and supply of medical equipment and masks; four Portuguese €3 bn schemes for small and medium-sized enterprises and midcaps; two German subsidised loan programmes (one covering up to 90% of the risk for loans for mid-sized and larger companies with a maturity of up to 5 years and to €1 billion per company, depending on the company's liquidity needs, and one in which the German federal promotional bank participates together with private banks to provide larger loans – risk cover taken by the State up to 80% of a specific loan but not more than 50% of total debt of a company).

DG COMP of the European Commission has set up a dedicated mailbox and telephone number to assist Member States with any queries on COVID-19 State aid measures:

- +32.2.296.52 00

- COMP-COVID@ec.europa.eu

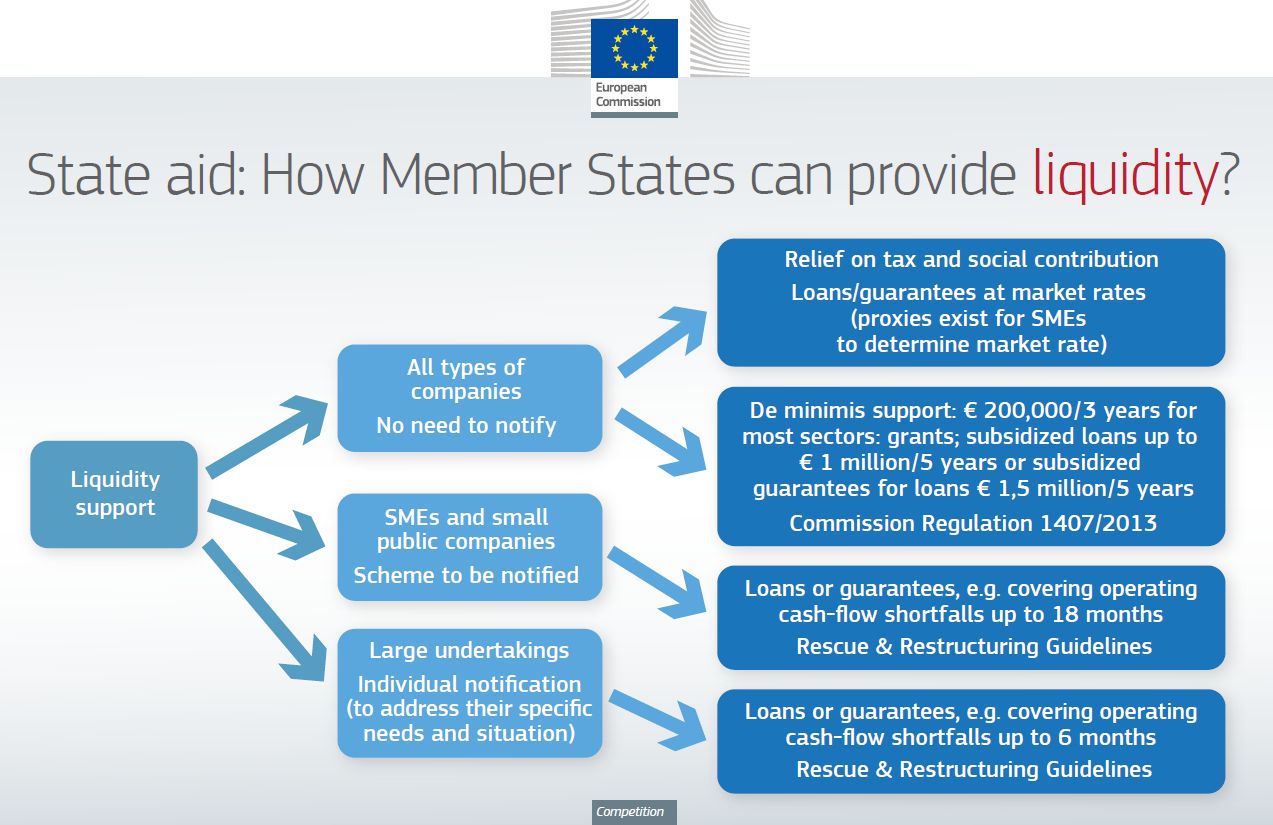

DG COMP has also illustrated the various forms of liquidity aid in the following chart:

Our recommendations

- Identify the detailed difficulties and needs with a direct causal link to the COVID-19 outbreak.

- Always verify that the support that the Member State offered was duly notified and approved by the European Commission or did not constitute State aid under EU rules, or was exempted from this process because it is clearly covered by the General Block Exemption Regulation or the de minimis

- Provide technical and legal assistance to the Member State concerned for the examination of your case and during the whole notification process to the European Commission. No matter how well-intentioned a Member State may be, a company is always best placed to explain the difficulties it is facing and why State support would be justified.

- Be conscious that any acceptance of State aid not notified or not approved by the European Commission (i.e. an "unlawful State aid", even if later declared compatible by the European Commission) constitutes unfair competition likely to trigger liability under national laws.

- Be conscious that any State aid unlawfully granted and received will almost always have to be recovered without the possibility of an argument based on alleged legitimate expectations being admissible (the Member State may not legally provide any assurances to aid beneficiaries; only the European Commission can do so).

- Always require specialised State aid advice to avoid the negative consequences of Member States' violations of the applicable rules (in particular unlawful aid recovery).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.