The Roschier Disputes Index comprises a market survey focusing on Northern Europe's prevailing practices and trends in dispute resolution, as seen from the perspective of the largest companies operating in Sweden and Finland. The objective of the Roschier Disputes Index is to garner opinion on the various facets of commercial dispute resolution: preferred dispute resolution methods, preferred substantive rules of law as well as arbitration rules, and the most important developments noted or anticipated in the way the largest companies in the region resolve disputes.

The data for the Roschier Disputes Index was collected on behalf of Roschier by TNS SIFO Prospera, an independent market research firm that is one of the leading market information and insight companies in the field with over 20 years' experience conducting research in the Nordic region.

The results of the Roschier Disputes Index are based on comprehensive interviews conducted by TNS SIFO Prospera with General Counsel and other persons in managerial positions in the 100 largest companies operating in both Sweden and Finland.

The financial downturn of 2009-2010 has obviously affected the business climate in Northern Europe as it has in most other parts of the world. In the previous financial downturn at the end of the 1990s the dispute resolution market boomed, and dispute resolution has since been perceived as counter-cyclical. During the last year and a half, the dispute resolution market has thus faced a lot of speculation regarding the effects of the downturn on disputes in the region.

Despite the speculation, however, there is little publicly available data to prove (or disprove) the perceived trends in dispute resolution. The Roschier Disputes Index was intended to uncover such data so as to permit conclusions on the basis thereof.

Perhaps the single most notable finding of the Roschier Disputes Index is that despite the experiences with booming dispute resolution during the last downturn, no signs of a boom are as yet in sight. On the contrary, a majority of the companies surveyed have not experienced significant growth in the number of disputes and do not anticipate such growth over the coming years either. As evidenced by the survey results, the major trends in the coming five years rather relate to cost consciousness, cost cutting and improved cost management. Companies are clearly interested in exploring alternative ways of resolving disputes. The Roschier Disputes Index thus confirms the general perception among management – that dispute resolution is expensive and to be avoided, if possible.

Another interesting observation is that in selecting arbitration as a preferred dispute resolution method, the confidentiality of the process seems to play a much larger role than is sometimes assumed. In jurisdictions that do not regard confidentiality as an inherent feature of the arbitral process, clients who consider confidentiality important should have this in mind when drafting and negotiating arbitration clauses in their contracts.

We hope that Roschier Disputes Index will be a helpful tool for management and external counsel, as well as for anyone with a particular interest in business dispute resolution.

Methodology

TNS SIFO Prospera carried out a market research project, contacting General Counsel, CEOs, CFOs and in-house counsel from the 100 largest companies (based on turnover) in Sweden and Finland, respectively. Of these companies, 164 were included in the survey. The response rate was 82%, i.e. 135 organizations responded to the survey. Subsidiaries that have their own legal department or handle legal issues themselves were interviewed; subsidiaries were excluded only if interviewers were directed to the parent company. Numerous international subsidiaries have their legal department outside the Nordic region; such subsidiaries are not included in the survey. The universe of organizations is presented at the end of this report.

Interviews were conducted from 10 May to 25 August 2010. The interviews were executed as telephone interviews and based on a questionnaire prepared by Roschier in cooperation with TNS SIFO Prospera, with a focus on business disputes with a value of EUR 100 000 or more. All interviews were entirely confidential and figures have been reported only in the aggregate. The survey results are divided by country and by size of company.

Tier 1 companies include all interviewed organizations that had a turnover in 2009 of at least EUR 5 billion, inclusive of subsidiaries. Tier 2 companies include all interviewed organizations with a turnover in 2009 between EUR 0.7 billion and EUR 4.9 billion, inclusive of subsidiaries.

Key Findings

- While arbitration is the preferred dispute resolution method overall and while most contracts refer disputes to arbitration, most disputes that materialize are tried in litigation. Hence the volume of non-contractual disputes would seem to be substantial.

- Despite the trends of globalization, Nordic companies still hold a strong preference for their own national law and local arbitration institutions.

- Decisive factors when choosing between arbitration and litigation include speed, confidentiality and cost, though misconceptions exist regarding the confidential nature of arbitration.

- The credit crunch has had less effect on dispute resolution than expected – no signs of a counter-cyclical disputes boom are in sight.

- Future trends include greater cost consciousness, predictability concerning cost, and willingness to explore ADR/mediation.

Survey Findings

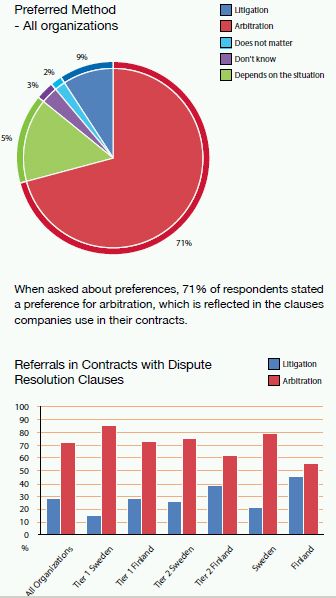

Dispute Resolution Clauses

A division emerged between Swedish Tier 1 companies and Finnish Tier 1 companies, with 85% of Swedish Tier 1 companies' contracts referring to arbitration but only 72% of Finnish Tier 1 companies' contracts doing the same. A similar division became apparent between Swedish Tier 2 companies and Finnish Tier 2 companies. While such companies' contracts still evidenced a preference for arbitration, the percentages were lower: contracts with dispute resolution clauses referring disputes to arbitration were 75% and 62% for Tier 2 companies in Sweden and Finland, respectively, while 25% and 38% referred disputes to litigation.

While the percentage of contracts that contain dispute resolution clauses were similar between Sweden and Finland, a preference for arbitration was much clearer in Sweden, where Among all organizations, some 52% of disputes that materialize are litigated while 48% are arbitrated.

Among Tier 1 companies, the percentage of arbitration disputes rises to 64%, while only 36% of disputes are litigated. Tier 2 companies' disputes tend to go to litigation (55%) more frequently than arbitration (45%).

Key Finding

Almost all of the organizations' contracts (93%) contain dispute resolution clauses, and of those, most clauses (72%) refer disputes to arbitration. However, while most contracts refer to arbitration, more of the disputes that materialize are litigation disputes. The likely explanation for this is that a substantial number of disputes are non-contractual.

Decisive Factors for Choice of Dispute Resolution Method

According to the respondents, litigation:

- Costs less

- Involves greater transparency

- Offers the possibility to appeal an unfavorable decision

- Provides greater process management opportunities

According to the respondents, arbitration:

- Costs less

- Is confidential

- Is faster than litigation

- Allows parties to choose decision-makers with particular Expertise

Key Finding

Speed and confidentiality seem to be the most significant factors in most organizations' decision making on this point, which is not surprising. Having said this, many respondents noted that the decisive factors in choosing a dispute resolution method vary from case to case, depending on the nature of the contract, the identity of the counter party and the negotiation balance of power between the parties.

Learning Point I

In reality litigation can be just as costly as arbitration, depending on the circumstances of each case.

Learning Point II

Contrary to what many respondents seemed to think, arbitration proceedings under most arbitration rules are confidential only if the parties have expressly so agreed.

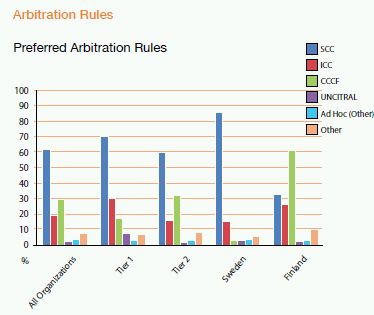

The Stockholm Chamber of Commerce (SCC) Rules were the most preferred arbitration rules, though the Central Chamber of Commerce of Finland (CCCF) Rules were popular among Finnish companies. More Tier 1 companies than Tier 2 companies preferred the International Chamber of Commerce (ICC) Rules, which were also slightly more commonly applied in Finland than in Sweden. Only a small percentage of respondents preferred to use the UNCITRAL ad hoc arbitration rules.

Key Finding

Respondents showed a strong preference for regional institutional arbitration rules (the SCC and the CCCF) over international rules; however, this preference was more pronounced in Sweden than in Finland and among Tier 2 companies than among Tier 1 companies. The data shows that the rules used in practice generally correspond quite closely with the rules companies say they prefer.

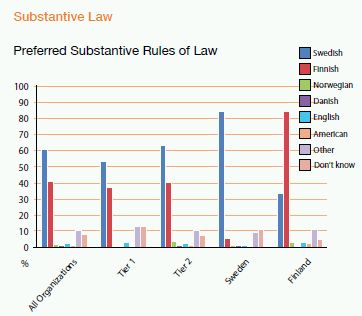

Among all organizations surveyed, Swedish law is the most preferred, with the second most preferred substantive law being Finnish law. On average, more Tier 2 companies' contracts than Tier 1 companies' contracts referred to the respondents' preferred substantive law. For most of the respondents from both Sweden and Finland, on average just over three-quarters (79%) of their contracts refer to their preferred substantive law.

Among all respondents, the largest percentage of litigation disputes involved Swedish substantive law, with Finnish substantive law second. Tier 1 companies tended to apply Swedish law more than Finnish law in their disputes, whereas among Tier 2 companies the choice of law was evenly split.

Key Finding

As might have been expected, a clear preference emerged among respondents for their own national substantive law or the law of a neighboring country.

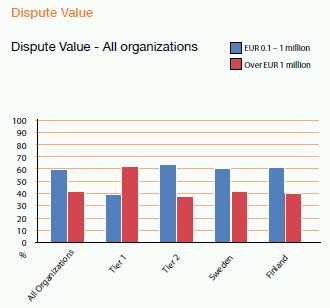

The survey focused exclusively on disputes valued at more than EUR 100 000. In both Sweden and Finland, most disputes (59- 60%) have a value between EUR 100 000 and 1 million, while some 41% have a value over EUR 1 million. The percentage of disputes over EUR 1 million was 61% for Tier 1 companies, while only 37% of Tier 2 companies' disputes were valued at more than EUR 1 million.

Key Finding

It is more common for disputes to have a value between EUR 100 000 and 1 million than to have a value of over EUR 1 million.

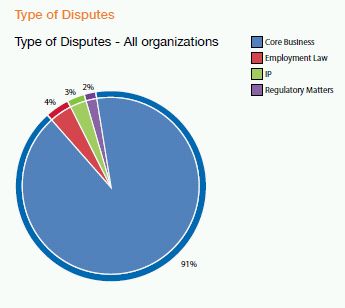

Most disputes – whether decided in litigation or arbitration – overwhelmingly involve companies' core business (91%), with smaller percentages involving, in descending order: employment law, IP matters and regulatory matters. These figures held for both Tier 1 and Tier 2 companies, and for companies in both Sweden and Finland, with only minor differences in the distribution.

Key Finding

Disputes, whether resolved through litigation or arbitration, generally involve the company's core business. Notably, employment disputes are generally more common than IP disputes.

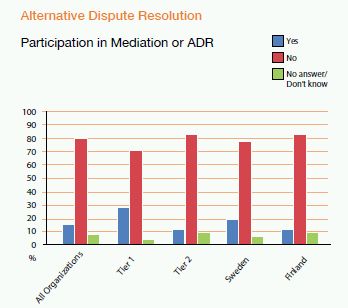

Most respondents (79%), whether in Finland or Sweden, do not currently participate in mediation or ADR proceedings. More Tier 1 companies (27%) than Tier 2 companies (10%) said they had participated in mediation or ADR proceedings in the past year. A greater percentage of Swedish respondents (18%) than Finnish respondents (10%) said that they currently use mediation or ADR as a dispute resolution method.

Key Finding

The use of mediation and ADR proceedings is notable but still moderate in the region.

A marginally higher percentage of Swedish respondents than Finnish respondents reported no change in business disputes involving their core business over the last 12 months. No decisive differences could be noted between Finnish and Swedish companies or between Tier 1 and Tier 2 companies.

Concerning matters other than the companies' core business (i.e. employment law, IP and regulatory matters), most respondents across the board (between 80 and 90% for each category) reported no changes over the past 12 months. Also here, no decisive differences could be noted between Finnish and Swedish companies or between Tier 1 and Tier 2 companies.

Key Finding

Despite predictions to the contrary due to the financial downturn of the last 12 months, most companies have seen no major change in disputes concerning their core business or disputes related to employment, IP or regulatory matters.

What Does the Future Bring?

Anticipated Change in the Coming Year

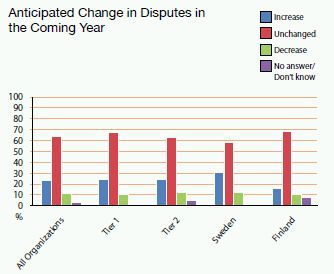

In both countries, most companies (63% overall) expect that their number of disputes will remain unchanged, while 23% overall expect an increase and 11% anticipate a decrease in the number of disputes. These numbers hold true for both Tier 1 and Tier 2 companies. By country, however, it appears that more Finnish companies – 68%, as opposed to 58% of Swedish companies – expect no change in the number of disputes. Interestingly, the percentage of Swedish companies expecting an increase (30%) is twice that of Finnish companies anticipating the same (15%). In certain other jurisdictions, notably in the common law world, it seems that the expectation concerning future volume of disputes is that of a substantial increase. Assuming that this observation is correct and that Nordic companies are no less able than, for example, US or UK companies to accurately predict the future of dispute prevalence, a possible explanation may be that Nordic companies are simply less litigious in their approach to conflict management.

Overall, 86% of respondents anticipate no change in their company dispute resolution policy, while 13% of respondents foresee a change. Some 14% of Tier 2 companies – compared to only 7% of Tier 1 companies – anticipate a change. A greater percentage of Finnish companies (16%) than of Swedish companies (9%) indicated a change was on the horizon for them.

Key Finding

Concerning the coming year, most respondents do not foresee a significant change in the number of disputes. However, of those who do anticipate a change, a greater number of Swedish companies than Finnish companies foresee an increase in disputes. Similarly, most companies do not anticipate any change in their dispute resolution policies, though the percentage of companies that do anticipate policy changes is greater in Finland than in Sweden.

Anticipated Change in the Coming Year

Cost consciousness

- Search for simplified dispute resolution procedures

- Need for alternative ways of resolving disputes and flexible solutions

-

- Mediation / ADR

- Prevent disputes before they occur

- Pre-dispute resolution

- Conciliation

Greater influence of globalization

- Branching out from regional business to business across continents

- Contacts with outside businesses may result in more arbitration or litigation

Use of external counsel

- Specialists

- Choose wisely and build good relationships with external counsel

- Consider having in-house disputes lawyers

Key Finding

Most companies do not anticipate major changes in the coming five years, although respondents indicated that cost consciousness and interest in alternative forms of dispute resolution, such as mediation and ADR proceedings, are increasing.

Sweden

The following Swedish organizations were included. In order to ensure the anonymity of the interviewees, the list does not specify participating and non-participating organizations.

Finland

The following Finnish organizations were included. In order to ensure the anonymity of the interviewees, the list does not specify participating and non-participating organizations.

Roschier Disputes Index

The Roschier Disputes Index comprises an independent market survey focusing on practices and trends in dispute resolution, as seen by the largest companies operating in Sweden and Finland. The survey was conducted between 10 May and 25 August 2010 on behalf of Roschier by TNS SIFO Prospera, one of the leading independent market research firms in the Nordic region.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.