Welcome to part 4 of our 6-part article series about how audit committees ("ACs") can prepare and deal with new legislation. Specifically, the law of 23 July 2016 on the audit profession ("Law") and Regulation (EU) N° 537/2014 ("Regulation") will have an impact on audit committees in terms of their roles and responsibilities, and their relationships with external auditors.

Step 4 – What is the specific role of the AC in terms of non-audit services?

Step 5 – What kind of relationship should the AC maintain with the external auditor?

Step 6 – What should the additional report of the external auditor to the AC include?

In this article, we will discuss the AC's role regarding non-audit services ("NAS"). The new legislation introduces prohibitions on certain NAS as well as fee caps for public interest entities ("PIEs").

Which NAS are prohibited?

The following NAS are prohibited, as per Luxembourg legislation:

The statutory audit firm of the PIE and any member of its network cannot provide prohibited NAS to:

- the PIE itself

- its EU parent undertakings

- its EU controlled undertakings

There are also limited restrictions applicable to controlled undertakings outside the EU. A "threats and safeguards" approach is required, although a limited number of absolute prohibitions still apply.

When will these restrictions apply?

The statutory auditor cannot provide prohibited NAS to the PIE between the beginning of the financial year under audit and the release of the audit report. The restrictions apply to the first financial year starting on or after 17 June 2016. This means that, for a PIE with a 31 December 2016 year-end, the restrictions on NAS would apply from 1 January 2017.

What NAS can be provided?

Those NAS which are not on the list of prohibited services are permitted, subject to the general principles of independence and audit committee approval.

Luxembourg has taken the view that valuation and certain tax services are allowed (e.g. preparation of tax forms, identification of public subsidies, support for tax inspections, calculation of direct and indirect tax and deferred tax, and tax advice)—provided (1) that they have no direct effect, or have an immaterial effect, either separately or in aggregate, on the audited financial statements, (2) that an estimation of their effect on the audited financial statements is comprehensively documented, and (3) that the independence principles are complied with.

...and the fee cap?

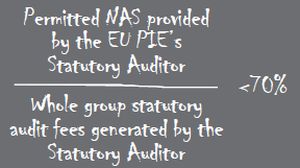

In addition, a 70% cap on fees from permitted NAS also applies to the statutory audit firm. It is computed on the average of the statutory audit fees over the preceding three years.

The 70% fee cap applies to permitted NAS provided by the statutory audit firm to the PIE, its parents and controlled undertakings. The geographical location of these group entities is irrelevant. The fees are paid to the statutory audit firm but not to its network.

When will the NAS fee cap clock start to tick?

The 70% fee cap starts to apply as from the first financial year starting on or after 17 June 2016. For example, for a PIE with a 31 December year-end, the first financial year to count would be the year ending 2017. Assuming three consecutive years of service, the cap would first apply to the financial year commencing on 1 January 2020. Any full-year "break" in the consecutive nature of the permitted NAS will result in the clock resetting back to zero.

What are the AC's responsibilities?

ACs have the responsibility to pre-approve permissible NAS after properly assessing threats to independence and the safeguards applied. ACs shall also perform oversight of the operation of the 70% fee cap.

What are the practical considerations for selection and management of professional advisers?

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.