Introduction

The year 2019 marked the 11th anniversary of the implementation of the Anti-monopoly Law and was also the first full calendar year since the State Administration for Market Regulation (SAMR) took over the role as China's single centralised antitrust enforcement agency.

The SAMR maintained a consistently rigorous and prudent attitude towards merger control review in 2019. The overall case handling efficiency has been improved in view of the fact that the total number of cases concluded increased while the average time for case reviews was reduced. The SAMR concluded 465 cases in 2019. Among them, the SAMR unconditionally approved 460 cases and conditionally approved five cases. As to the cases that were conditionally approved, the SAMR imposed various tailored conditions. There was no prohibited merger case in 2019. In addition, the SAMR investigated more non-filing cases and imposed more penalties on non-filers compared with 2018. In particular, a total of 16 penalty decisions against non-filers of merger cases were published throughout 2019, which was the highest annual figure over the past decade.

Legislation

On 7 January 2020 the SAMR released a draft of the Interim Provisions for Merger Control Review (the Interim Provisions) for public comment1. The Interim Provisions incorporate all major regulations for merger control review into one consistent and easy-to-follow comprehensive regulation, although no substantial new changes have been proposed thereunder. The final version of the Interim Provisions is expected to be adopted in mid-2020.

On 2 January 2020 the SAMR released a revised draft of the Anti-monopoly Law for public comment (the Revised Draft)2. Although the Revised Draft follows the current Anti-monopoly Law's basic framework, it significantly enhances the legal liability of Anti-monopoly Law violators. For example, in accordance with Article 55 of the Revised Draft, the proposed penalty will be up to 10% of the non-filer's annual sales in previous year instead of the maximum amount of fine Rmb500,000 under the current Anti-monopoly Law, which is clearly insufficient for deterring non-filers. It also clarifies practical issues such as 'controlling rights' for merger filing purposes. At present, there is no clear timetable for the finalisation of the Revised Draft or the promulgation of the new Anti-monopoly Law.

Unconditionally cleared cases

The SAMR unconditionally approved 460 cases in 2019 - slightly higher than the previous year (444 cases). As regards simple cases, 341 were concluded in 2019 (73.3% of all cases). The proportion of simple cases decreased compared with 2018 (81.53% of all cases). On average, simple cases took 15 days to be concluded, which was a slight reduction from the 16-day conclusion rate in 2018. Almost all simple cases were cleared within 30 days of formal acceptance by the SAMR. This demonstrates that simple case procedure plays an active role in enhancing the efficiency of concentration filing, particularly in the sense of reducing reviewing time.

However, in practice, strict rules concerning the material and data required by the SAMR still apply. In particular, during the pre-review stage (ie, before official case acceptance), notified parties must often submit detailed materials. Therefore, this requirement may also extend the wait time before case filing.

The Revised Draft introduces a 'stop-clock' clause that specifies the following conditions to discontinue the timelines for merger review:

- on application or consent by the notifying parties;

- supplementary submissions of documents and materials at the request of the authority; or

- remedy discussions with the authority.

This proposed 'stop-clock' clause would tackle the problem that in its absence, the notifying parties can only withdraw and refile the case when the statutory review period is running out.

Conditionally cleared cases

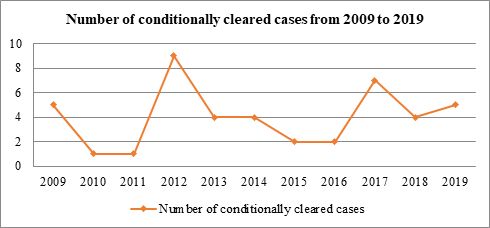

In 2019 the SAMR conditionally approved five cases, a relatively stable number compared with 2018 (four cases). Figure 1 (below) illustrates the number of cases conditionally cleared between 2009 and 2019.

Figure 1

In 2019 four conditionally cleared cases were approved with behavioural conditions and the remaining one was approved with both structural and behavioural conditions. All of the five conditionally approved cases in 2019 were withdrawn and resubmitted before the expiry of the first statutory merger review period (ie, 180 days). This shows that the SAMR is becoming more prudent in reviewing mega mergers which may raise competition concerns. Withdrawal of the filing also provides notifying parties with certain flexibility and more time to communicate with the SAMR. From the first submission of filing materials to a case being conditionally concluded, the review process for the above five cases lasted a minimum of 263 days3 and a maximum of 562 days4.

Novelis' acquisition of Aleris

On 12 December 2019 the SAMR conditionally approved Novelis's acquisition of Aleris5. Novelis is a leading producer of aluminium rolled products and the world's largest recycler of aluminium. Aleris is a global leader in manufacturing and sales of aluminium rolled products.

In this case, the parties overlapped in two markets - namely, the interior aluminium autobody sheets market and the exterior aluminium autobody sheets market. Since the relevant product markets' competition structure in China was different from that in other jurisdictions, and the main foreign-invested operators all have local production in China, the relevant geographic market was defined as China.

Novelis was the largest player in the abovementioned markets and Aleris ranked third in both markets. After transaction, the market share of Novelis and Aleris would reach 70% to 75% in the interior aluminium autobody sheets market and 75% to 80% in the exterior aluminium autobody sheets market. Further, the level of market concentration would be highly increased. After transaction, there would be only four main competitors in the interior aluminium autobody sheets market and two main competitors remaining in the exterior aluminium autobody sheets market. Apart from that, the SAMR also assessed factors such as:

- the elimination of Aleris's competition restraints on Novelis;

- the incentive of the merged entity to eliminate or restrict competition after the transaction;

- the entry barriers to the relevant markets; and

- the recognition of downstream customers.

The SAMR approved the proposed concentration with both structural and behavioural conditions. Given that the relevant products that Aleris sold in China were mainly exported from Europe, Aleris was required to divest its entire business relating to interior and exterior aluminium autobody sheets in the European Economic Area. Further, the merged entity was prohibited from supplying cold-rolled sheet to its business partners in order to maintain market competition.

In addition, the proposed acquisition was initially filed for a review under the simplified procedure, and the SAMR accepted the case on 30 September 2018. Due to an objection raised by a third party during the public consultation period, the SAMR found that the proposed acquisition did not meet the standards for the simplified procedure and thus revoked the acceptance of the case and asked the notifying party to re-file it under the regular procedure. The notifying party resubmitted the case under regular procedure on 1 November 2018 and it was formally accepted on 13 December 2018. This back and forth shows that the notifying party should choose the most appropriate procedure to file in order to avoid waste of time. The merger control review could be delayed for months if the SAMR revokes the case acceptance when the notified concentration does not meet the standards for the simplified procedure.

Cargotec's acquisition of TTS Group

On 5 July 2019 the SAMR conditionally approved Cargotec's acquisition of TTS Group6. The acquirer of the transaction was MacGregor Group, a subsidiary of Cargotec. The MacGregor Group is principally engaged in the sale and service of products in the marine transportation cargo handling sector. The TTS Group is mainly engaged in the sale and service of hatch covers, ro-ro equipment for commercial vessels, ship cranes and winches. The transaction was filed on 15 June 2018, following which the parties were required to provide supplemental material. The SAMR formally accepted the case on 26 July 2018 and decided to conduct further review on 22 August 2018. Before the expiry of the review period, the parties withdrew the filing on 11 January 2019. The SAMR accepted the refiling on 14 January 2019 and the review process was prolonged until 9 July 2019.

In this case, the parties had overlaps in several markets, including hatch covers, ro-ro equipment for commercial vessels, ship cranes, winches and related after-sale services. The SAMR conditionally approved the proposed acquisition with behavioural remedies, including:

- ensuring the independence of relevant businesses;

- maintaining respective competition;

- not raising the prices of related products in the Chinese market; and

- not refusing or restricting supplies of the products to Chinese customers.

In addition, the SAMR adopted the 'firewall guidance handbook and training' remedy proposed by the filing parties. The parties committed to create an internal firewall between their respective employees, separate their competition-sensitive information and workplaces, issue a detailed firewall guidance handbook and conduct training. Setting up an internal firewall and the application of related remedies will improve the efficiency and feasibility of the implementation as well as the supervision of the behavioural remedies. Although these types of measure have been adopted in previous behavioural remedy cases, the Cargotec case provides guidance on the practical aspects of implementing them.

The abovementioned measures on the firewall management were proposed again in a subsequent case in 2019 - namely, II-VI's acquisition of Finisar7. In this case, the SAMR imposed the behaviour conditions on the parties of setting up a firewall and supplying the product in accordance with fair, reasonable and non-discriminatory (FRAND) principles. Particularly, the SAMR put forward the requirement of 'firewall guidance handbook and training' on the implementation of behavioural remedies.

In the five cases that were conditionally approved in 2019, most of the conditions attached were only behavioural remedies. In contrast to structural remedies, behavioural remedies have a high degree of flexibility, which can avoid excessive intervention of the antitrust agencies in concentration. However, it also requires more regulatory supervision post merger. Compared with EU and US antitrust enforcement agencies' preference for structural remedies, the Chinese antitrust enforcement agency seems more comfortable imposing behavioural conditions to address competition concerns.

Penalties on non-filers

In recent years, the antitrust authorities have never relaxed their supervision of non-filing cases. By the end of 2019, the SAMR had released 46 non-filing cases and imposed total fines of Rmb16.1 million on 68 undertakings. In 2019, the SAMR significantly strengthened its supervision of and penalties on non-filing parties. Sixteen cases were published and 21 undertakings were punished with a total fine of Rmb6.25 million. The largest fine issued was Rmb400,000, while the smallest was Rmb200,000. The SAMR initiates investigations on non-filing cases by means of self-observation, third-party reporting and voluntary reporting by notifiable parties.

Notably, the SAMR has been going after non-filers even where their failure of notification occurred many years ago. Each of Pierburg and Xingfu Motorcycle was fined Rmb350,000 for their failure to notify a proposed joint venture before its establishment8, while the joint venture was established in 2013. This case shows that the SAMR shows no mercy for non-filers that failed to fulfil their notification obligations a long time ago.

The SAMR also investigated several non-filing cases involving minority equity investments in 2019. For instance, MBK Partners, LP (MBK) was fined Rmb350,000 for its failure to notify its acquisition of a 23.53% stake in Shanghai Siyanli Industrial Co Ltd. Further, Dejin Enterprise was fined Rmb300,000 for its failure to notify its acquisition of a 29.99% stake in Huitong Energy. Whether an acquisition of relatively small equity (eg, less than 30% equity) constitutes a change of control must be determined on a case-by-case basis. According to Article 23 of the Revised Draft, 'control' refers to an undertaking's rights or actual status to, directly or indirectly, individually or jointly, exert or potentially exert a decisive influence on another undertaking's production and operation activities or other major decisions. Given the remarkable increase of non-filing fines and the robust enforcement towards non-filings in recent years, undertakings should consider whether there is a change of control in each transaction.

At present, the maximum amount of fines imposed on non-filers is Rmb500,000, which is clearly insufficient to deter non-filers. In accordance with Article 55 of the Revised Draft9, the proposed penalty will be up to 10% of the non-filer's annual sales in previous year. This adjustment will greatly increase the deterrence of illegal acts in relation to the violation of merger filing regulations if the proposed change is adopted in future.

Comment

The SAMR has become more stringent and detail oriented with respect to its analysis of relevant markets and the competition impact of mergers. It is expected that the SAMR's merger control enforcement will maintain its professionalism and stability in 2020.

Further, the large number of non-filing cases and the increased fines indicate that the SAMR is gradually strengthening its enforcement crackdown on non-filers. Moreover, the proposed revision of the Anti-monopoly Law is expected to increase the size of penalties for non-filers. Enterprises should acknowledge the thresholds and criteria of merger filing in order to fulfil their obligations to avoid penalties and any adverse consequences of closing a transaction.

Footnotes

1. The original Chinese version is available at the SAMR's website: www.samr.gov.cn/fldj/tzgg/zqyj/202001/ t20200107_310322.html.

2. The original Chinese version is available at the SAMR's website: www.samr.gov.cn/hd/zjdc/202001/ t20200102_310120.html.

3. II-VI's acquisition of Finisar case, the announcement is available at the SAMR's website: www.samr.gov.cn/ fldj/tzgg/ftjpz/201909/t20190920_306948.html.

4. JV between DSM and Zhejiang Garden Biochemical case, the announcement is available at the SAMR's website: http://gkml.samr.gov.cn/nsjg/fldj/201910/t20191018_307458.html.

5. The announcement is available at the SAMR's website: http://www.samr.gov.cn/fldj/tzgg/ftjpz/201912/t20191220_309365.html

6. The announcement is available at the SAMR's website: http://www.samr.gov.cn/fldj/tzgg/ftjpz/201907/t20190712_303428.html

7. The announcement is available at the SAMR's website: www.samr.gov.cn/fldj/tzgg/ftjpz/201909/ t20190920_306948.html.

8. The original Chinese penalty decision is available at the SAMR's website: www.samr.gov.cn/fldj/tzgg/ xzcf/201911/t20191114_308483.html.

9. The original Chinese version is available at the SAMR's website: www.samr.gov.cn/hd/zjdc/202001/ t20200102_310120.html.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.