FOREWARD

We are pleased to present Nexdigm (SKP) Investment Chronicle – our periodic update that focuses on the deal-making landscape in India, comprising Mergers and Acquisitions (M&A), equity investments, and exits. In this report, we look at India's transactions arena in the first half of 2020.

Mergers and Acquisitions comprised 58% of the total USD 42 billion deal landscape in H1 2020, followed by private equity investments comprising 40%. The investment market at the beginning of FY20 was seller-friendly with attractive valuations and multiple exit routes. However, the COVID-19 pandemic made the market more cautious, with the scales tipped in favor of buyers and cash-rich companies. Private equity exits merely contributed to the total deal value in this period, as discounted valuations have revented investors to market their investments.

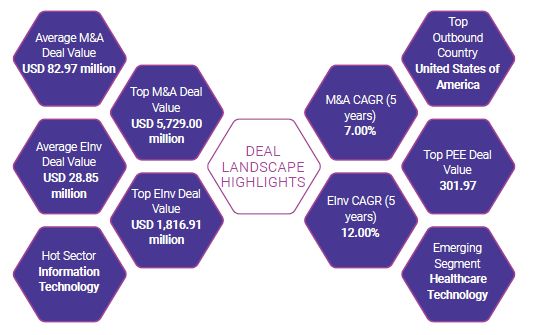

As customary, the Information Technology sector took a lead in terms of deal volume. However, H1 2020 has marked 100 deals in the Healthcare sector, fuelled by an intent to work collaboratively on the prevailing pandemic. The broadening scope of telecom and technological infrastructure to facilitate remote management during the COVID-19 outbreak, as well as the announcement of the consolidation of public sector banks, creates further anticipation for deals in these value dominating sectors.

The escalated transmission of COVID-19 has led to a harsh dilemma for the capital markets causing vulnerable business risk worldwide. Stringent restrictions on travel and physical proximity have made the execution of deals challenging. The government rules are constantly changing with regards to employment, workspace safety, data privacy, and sector specific regulations. The uncertainty around business projections, discord on the valuation of companies, and diversion of cash flows to operational needs have hampered deal success. Nevertheless, the government and businesses are undertaking relentless efforts to tackle the crises and ensure long term potential of investments remain intact.

With India determined to become a 'self reliant' country, the government has curbed corporate tax rates and assured further changes in the 'Make in India' initiative, to emerge as a favorable investment destination compared to its South Asian peers. This coupled with companies exploring restructuring of businesses and supply chain due to change in geo-economic dynamics, is expected to encourage transaction opportunities in the approaching years. While deal activity could be subdued in the coming quarters on account of challenges in execution and economic slowdown, the India growth story may remain attractive for investors with a long term horizon.

DEAL TRENDS

M&A - Merger & Acquisitions

EInv - Equity Investments

PEE - Private Equity Exits

MERGERS AND ACQUISITIONS

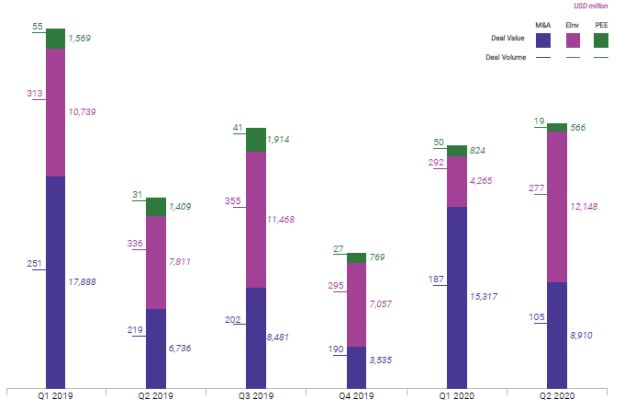

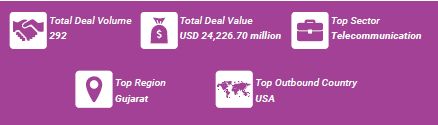

2019 observed a cautious drift in M&A activity, basis the political uncertainty and economic slowdown. Although deal momentum was expected to improve in 2020, the initial half of the year followed stead at USD 24,227 million from 292 deals, owing to the rapid outbreak of COVID-19 worldwide. However, the average deal size increased by 1.6x in H1 2020 vs H1 2019 due to a corresponding fall in deal volume.

Keeping with the trend, Information Technology outnumbered other sectors in terms of deal volume. Financials, Telecommunication, and Industrials are the predominant sectors for H1 2020, bagging the big-ticket transactions, making up 70% of the total deal value. Reforms in the regulatory regime such as the reduction in tax rates and softening of compliance norms, are aimed to allure foreign investments.

The advent of the COVID-19 pandemic and the worldwide lockdown has caused operational hindrance in several industries. A short term fundamental shift in consumer behavior and supply chain could be observed. The ongoing deals have also been obstructed due to travel restrictions, shift in interpersonal interactions, and infrastructure constraints. The financial strain and ambiguity on business performance have also forced companies to re-evaluate their growth plans.

In the current ambivalent situation, companies on the brink of insolvency may consider cash consolidation through mergers to safeguard continuity. Conglomerates may also consider demergers and asset transfers for business stability. M&A activity is expected to be steered by industry consolidation, companies focused on survival, and acquisition of fairly valued stressed assets through spare cash reserves.

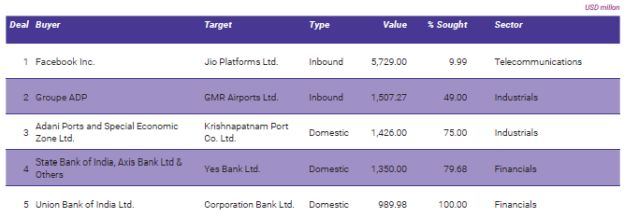

PRIME DEALS

ADP acquired 49% stake in GMR Airports for USD1.51 billion.

The consideration comprises USD1.37 billion towards the secondary sale of shares by GMR Infrastructure Ltd and equity infusion of USD 139.82 million in the company.

Earlier ,a consortium consisting of Tata group, SSG Capital and GIC Capital had signed the definitive agreement for investment in GMR Airports. However, the deal fell through due to Tata's conflict of interest in Vistara and AirAsia India.

There will be two portions to this transaction, the first stake of 24.99% as an immediate aid to improve profitability and cash flows, and to lower its debts while the remaining 24.01% stake is subject to regulatory approvals.

In order to achieve further synergy, Group ADP has pegged earn-outs worth USD 625.70 million, which are linked to pre-agreed performance metrics along with clearance on regulations over a span of 5 years.

Together, these companies have the largest portfolio of 336.5 million passengers, this deal structure will allow both the companies to widen its scope of access to global airports, opening up new opportunities for development.

Adani Ports and Special Economic Zone Ltd (Adani Ports) acquired a major stake in Krishnapatnam Port Co Ltd (KPCL) for USD 1.43 billion. The board of Adani Ports has approved a fundraising of $1.25 billion through dollar bonds.

However, Adani Port may consider re-negotiation of the pricing from the original deal announced in January 2020, owing to the significant change in the short to medium term economic conditions triggered by the COVID-19 outbreak and the resulting lockdown.

KPCL is the largest port in Andhra Pradesh and currently handles 54 MMT of cargo. Adani Port sees a potential to boost the cargo handled to 100 MMT within the next 7 years. This acquisition will also accelerate Adani Port's expansion plan.

Through this deal, Adani will increase its market share in India to 27% enhancing its position on the eastern coast of the country.

Click here to continue reading ...

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.