1. The reform and its drivers

We are witnessing an unprecedented review of Spanish Law 22/2003 on Insolvency Proceedings (Spanish Insolvency Act or "IA"). With the recent approval of three Royal Decree-Laws ("RDLs"), namely RDL 4/2014, of 7 March, RDL 11/2014, of 5 September and RDL 1/2015, of 27 February), the Spanish legislator seeks to achieve three main goals:

- Allow debtors to get rid of excessive financial burden, by turning it into sustainable debt that can be repaid in a realistic scenario, thus enabling the survival of viable companies. Lawmakers foster one of the three key objectives of Spanish insolvency proceedings: the so-called "business continuity" ("función de continuidad"). To date, IA provisions focused almost exclusively on the other two objectives: repayment of creditors ("función solutoria") and, to a lesser extent, civil punishment of those liable for insolvency ("función represora"). With the new amendments, these three principles are more evenly balanced.

- Honor an inspiring principle of Spanish Insolvency legislation, "par conditio creditorum" (ie, all creditors should be treated equally), and adjust the value of special privileges granted by in rem securities to actual prices in the real estate sector after the economic downturn.

- Facilitate a "second chance" for individual creditors, which has been a social demand in the last years; individuals declared insolvent may benefit now from the same "fresh start" as shareholders of insolvent companies that are wound-up and liquidated.

Nature of the new rules

RDLs are specific regulations issued by the Government "in cases of urgent need". They come into force upon publication in the Official State Gazzette ("Boletín Oficial del Estado") and have the status of "law" ("rango de ley"), but need to be validated by the Parliament within 1 month of publication.

RDLs implementing these amendments to the IA have been duly issued and are currently in force. RDL 4/2014 has already become Law 17/2014, of 30 September. Currently, both RDL 11/2014 and RDL 1/2015 are being processed as new draft bills ("Proyectos de Ley") so they are subject to new amendments in the coming weeks or months.

Scope of this note

This note focuses on two of the main innovations in the IA, namely (i) cram-down majorities and (ii) reduction of the value of secured claims in insolvency. The new amendments contain other ancillary provisions, but we focus now on the two novelties which may affect more the position of "specially privileged creditors" or "acreedores con privilegio especial" (ie, those secured by mortgages or pledges; "Secured Creditors").

2. Cram-down majorities

During its first decade of application, IA has not proved effective to avoid companies with liquidity or solvency problems ending up liquidated. Over 90% of insolvency proceedings in Spain in the last years went into the liquidation phase. One of the main reasons is that refinancing agreements ("acuerdos de refinanciación") and composition agreements ("convenios de acreedores") were not binding on Secured Creditors, who just had to wait until either (i) the 1-year "freeze period" elapsed; or (ii) the approval of a composition agreement to initiate (or continue with) separate enforcements over their collaterals, regardless of any terms or payment plans agreed by the other creditors.

This indifference of Secured Creditors made irrelevant any settlement among creditors in general, and rendered impossible the continuation of the debtor's business. This issue is addressed now with the new division of creditors into "classes" and the implementation of cram-down majorities ("mayorías de arrastre") that cause Secured Creditors to be bound by creditors' agreements (refinancing or composition).

Cram-down in refinancing agreements: the "Spanish Scheme of Arrangement" (Royal Decree-Law 4/2014)

Some scholars have described the new situation resulting from one of the amendments at hand as the "Spanish Scheme of Arrangement". Schemes of arrangement in anglo-saxon jurisdictions are defined as "a statutory procedure which permits a company to make an arrangement or compromise with creditors (or any class of them) which, if approved and sanctioned by the Court, will be binding on all of them, whether or not they vote in favor of it". Royal Decree-Law 4/2014 amended Article 5 bis and Additional Provision IV of the IA so dissident creditors who vote against a pre-insolvency refinancing agreement or do not vote at all may be crammed down (ie, bound by the agreement), even if their credits are secured.

- Majorities required for refinancing agreements to be binding on

Secured Creditors

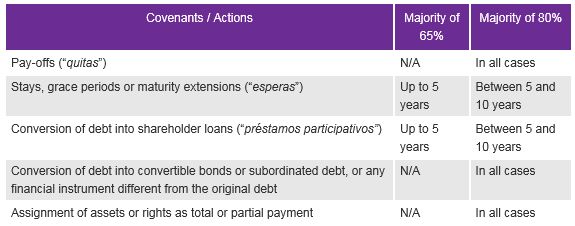

Cram-down majorities in refinancing agreements prior to insolvency are calculated as the % of "financial" debt covered by securities in relation to the total amount of secured debt. The required majority depends on the nature of the covenants / actions agreed:

- Different majorities for approval

The above majorities are those required for Secured Creditors to be bound by the agreement. A refinancing agreement may be otherwise validated ("homologado") by the Judge if it is approved by creditors owning at least 51% of the financial liabilities (without being binding on Secured Creditors if the above majorities are not met). This threshold has been set by RDL 4/2014, down from the previous thresholds of 75% and 55%.

Cram-down in composition agreements (Royal Decree-Law 11/2014):

The recent amendments have been extended to composition agreements (within the insolvency). For the purposes of the approval of composition agreements, Secured Creditors are divided now into four classes: (i) labor creditors (employees), (ii) public bodies (eg. Tax Authorities and Social Security), (iii) financial creditors (ie, banks and other financial lenders, etc.); and (iv) others (which include suppliers and commercial creditors). Cram-down majorities operate within each of these classes; so if for instance 60% of the secured debt corresponding to financial creditors agrees to a composition agreement, all dissident financial creditors shall be bound by it.

- Majorities required for composition agreements to be binding on

Secured Creditors

Cram-down majorities depend on the covenants/actions to be voted under the proposed composition agreement:

- Different majorities for approval

The above majorities are those required for Secured Creditors to be bound by the composition agreement. A composition agreement may be approved otherwise by the Judge if it is voted by creditors holding at least 50% or 65% of the ordinary debt, depending on whether it refers to the covenants / actions set out in the second or third column above, respectively (without being binding on Secured Creditors if the above majorities are not met).

3. Reduction of privileged claims

Upon the amendments carried out by RDLs 4/2014, 11/2014 and 1/2015, the IA foresees a potential reduction to the legal privileges attributed to Secured Creditors:

The "9/10 rule"

- Royal Decree-Law 4/2014

The RDL included for the first time a provision whereby the credit rights or claims held by a Secured Creditor against an insolvent company shall be calculated as 9/10 of the fair value ("valor razonable") of the collateral minus all other debts with a higher-ranking security over that same collateral, if any. The purpose of this amendment is to reduce the leverage of non-bound Secured Creditors whose right to a separate enforcement may jeopardize the effectiveness of a refinancing agreement. - Royal Decree-Law 11/2014

The 9/10 rule described above has been extended to composition agreements, and to any other situation where a non-bound Secured Creditor makes use of its secured claim over the collateral. The value of the security taken on any collateralized asset ("VofS") is set at 90% of the fair value ("valor razonable") of the collateral at hand, once all securities ranking ahead, if any, have been deducted. In no event shall the adjusted VofS exceed the overall mortgage / pledge liability, and it shall never be lower than 0:

VofS = Min [SC; (0.9 x FV – PS)] ≥ 0

Where:- "SC" means the lower of (i) the value of the secured claim (the total outstanding principal balance or OPB, in the case of an accelerated loan); or (ii) the maximum mortgage-secured amount noted in the Land Registry or "Registro de la Propiedad");

- "FV" means the fair value ("valor razonable") of the collateralized asset; and

- "PS" means the value of any claims with a higher-ranking security over the same asset (eg., mortgages ranking ahead).

The 10% adjustment over the fair value accounts (as a provision

or "cushion") for the foreclosure and other costs to be

borne by the insolvent debtor.

VofS is set out by receivers in their report ("informe de

la administración concursal"). Secured Creditors

are only entitled to credit-bid for up to the amount recognized as

VofS in the receivers' report, either at auction in the context

of mortgage enforcement proceedings or under a liquidation

plan.

- Royal Decree-Law 1/2015

This latest RDL includes some changes in the calculation of VofS from the previous RDLs. In a nutshell, for real estate assets the procedure is now as follows:- The asset must be appraised by an independent expert registered with Bank of Spain. This appraisal is not required if the value has been determined in the year prior to the declaration of insolvency by a valuation company registered with Bank of Spain;

- If new circumstances arise that may modify materially the fair value of the asset, a new appraisal will be required;

- In the case of finished dwellings or "viviendas terminadas", the appraisal may be replaced at the discretion of the receiver by an update of an existing one, provided that the latter is not older than 6 years. This update of an existing appraisal shall be based on the average variation (increase or decrease) observed in the fair value of similar dwellings within the same area;

- If such benchmarks are not available, or cannot be deemed as representative, the update may be based on the accumulated variation set by the National Institute of Statistics ("INE") for the Autonomous Community where the asset is located, provided that the base appraisal is not older than 3 years.

- Costs and expenses

The cost of appraisals and updates shall be borne by the insolvency estate and deducted from the receiver's retribution. Therefore, receivers will be generally reluctant to request these appraisals. If a creditor requests an appraisal, said creditor shall bear the cost of the appraisal (which, in practice, may be unchallenged by an alternative one that the receiver has to pay for). - Exception to the rule: third-party mortgagors

The 9/10 rule does not apply to credits secured with real estate assets owned by a third-party mortgagor in the case said mortgagor files for insolvency, since the liabilities (ie, the debt) are not with the insolvent mortgagor (ie, it remains with the third-party borrower or debtor).

Second opportunity for individual debtors

Royal Decree 1/2015 introduces a reform in insolvency of individuals, which, although possible with the legislation to date, has not been common to date. With the amendment, individual debtors in good faith (a much undetermined concept), may be exempted from all outstanding debts (eg., deficiency claims and the sort).

- Conditions for the "fresh start"

As conditions precedent, the insolvency proceedings must be finished, and not qualified as "guilty". The debtor may apply for the exemption (it is not automatic) if the following requirements are met:- The debtor must not have a criminal record for economic offences, forgery or fraud against the Tax or Social Security Authorities or workers' rights committed in the 10 years prior to the insolvency;

- The debtor must have applied for an out-of-court payment agreement ("acuerdo extrajudicial de pagos") during the insolvency proceedings; and

- Debts of the insolvency estate ("créditos contra la masa") must have been fully paid, together with those held by Secured Creditors (calculated pursuant to the 9/10 rule) and at least 25% of the ordinary credits.

If all the conditions above are complied with, the judge will agree to the "fresh start" of the debtor and it shall be exonerated from all outstanding debts.

- Risk for Secured Creditors

There is a clear risk that Secured Creditors against insolvent individuals now have the value of the claims reduced, since the debtor may only be liable for 90% of the fair value of the security and 25% of the debt ranked as "ordinary".

Creditors still have the right to claim the outstanding debt from any third-party guarantors. Also, during the 5 years following the judicial validation of the "fresh start", the creditor may apply for its revocation if the economic situation of the debtor improves. Once this term has elapsed, the exoneration of debts shall be definitive.

4. Allocation of voting rights

An important amendment imposed by RDL 11/2014 is the allocation of voting rights for the composition agreement at the creditors meeting to assignees of credits (except for persons especially related to the debtor). This is an important advantage in the debt market, since it removes a considerable restriction that limited the marketability of distressed debt (and grants the possibility for a new lender to vote for or against a composition agreement which may be detrimental for the new lender).

5. Further amendments to the law

As stated before, RDL 11/2014 and RDL 1/2015 are currently being processed as draft bills, and several amendments to the final text have been submitted by the different political parties in the Parliament. One of the most relevant is the filed by the People's Party ("Partido Popular"), whereby the proceeds from enforcement of real estate assets (or any sale of the property) should be applied to payment of the outstanding debt of Secured Creditors (not to the insolvency estate, as it may be inferred from the current wording of the IA). The rationale for this proposed amendment is to ensure that secured claims in insolvency are not reduced or impaired, and creditors are entitled to the full amount of their credit. If this amendment is finally approved, the only negative consequences of the 9/10 rule for Secured Creditors would be that: (i) they would only be entitled to credit-bid in an auction with the 9/10 of the fair value (not with their total outstanding claim); and (ii) the amount secured for voting purposes in refinancing and composition agreements would be calculated pursuant to the 9/10 rule.

Many other amendments of lesser relevance have been submitted so far. For instance, the People's Party has proposed to recognize as valid the appraisals of real estate assets issued within the 18 months prior to the declaration of insolvency, and UPyD has proposed that the appraisal may not necessarily be carried out by an expert shortlisted by Bank of Spain, in order to avoid distorted competence in the appraisal market, etc.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.