Introduction

The Irish investment limited partnership (the "ILP"), now re-shaped as a flexible fund investment vehicle following amendments made to the existing Investment Limited Partnership Act, 1994 (the "ILP Act"), is expected to become the fund structure of choice for many international investment managers, particularly those in the private equity and real assets sectors.

In this key features document, we briefly consider the ability to structure the ILP as an umbrella fund, which is considered to be one of the most innovative features of the Irish ILP. A more detailed analysis of the ILP is available here.

Key Points

- An ILP can be established as umbrella fund which is divided into a number of sub-funds;

- Each sub-fund within the umbrella fund pursues a separate investment strategy;

- While the majority of service providers are appointed to the umbrella ILP, different Investment Managers can be appointed to individual sub-funds within the umbrella ILP to manage the assets of those sub-funds on a discretionary basison;

- Umbrella ILPs offer significant economies of scale and increased speed to market;

- The ILP Act sets down specific statutory provisions dealing with segregated liability between individual sub-funds established within the umbrella ILP.

What is an umbrella ILP?

It is a collective investment scheme which is divided into a number of sub-funds, each of which has a separate pool of assets and is treated as a separate entity from a regulatory perspective.

Can sub-funds within the umbrella ILP pursue different investment strategies?

Yes. There is nothing precluding an umbrella ILP housing a number of different sub-funds which pursue very different investment strategies. This is because each sub-fund within the umbrella has its own separate pool of assets and is subject to its own investment and borrowing limits1.

Furthermore, while certain of the service providers (including the General Partner (the "GP"), the AIFM and the Depositary) must be appointed to the umbrella ILP, it is possible to appoint separate Investment Managers with specialised expertise to different sub-funds within the ILP.

What are some of the other advantages of the ILP?

Because the majority of service providers are appointed to the umbrella ILP, the structure offers significant economies of scale and increased speed to market when compared with costings and timing implications involved in establishing separate limited partnerships for each strategy/category of investor or for each successor, parallel or co-investment funds.

This is largely due to the fact that contracts with such service providers do not need to be re-negotiated for each sub-fund which is established within the umbrella ILP.

Furthermore, the umbrella ILP structure removes the need to establish and operate a separate GP for each new structure or category of investor.

Is there segregated liability between sub-funds?

The ILP Act sets down specific statutory provisions dealing with segregated liability between individual sub-funds established within the umbrella ILP.

Under the ILP Act, the assets and liabilities of each sub-fund in the umbrella ILP are segregated from the assets and liabilities of other sub-funds. This segregation between sub-funds is typically further ring-fenced by contractual arrangement.

Is it possible to have separate offering memoranda for each sub-fund within an umbrella ILP?

Provided that all other sub-funds established within the umbrella ILP are named in each offering memorandum, a separate offering memorandum can be prepared for each sub-fund in the umbrella, so investors will not need to be provided with the details of the other sub-funds.

Is it possible for one sub-fund within an umbrella ILP to invest in another sub-fund of the ILP umbrella?

Yes, provided that this is contemplated under the LPA and offering memorandum of the ILP. There are also certain rules imposed by the Central Bank to ensure no double-charging of the annual management fee2 to the investing sub-fund as a result of its investment in the receiving sub-fund. The annual report of the ILP must disclose any such cross-investment during the relevant period and the policies adopted to disclose such cross-investments must be explained in a note to the accounts.

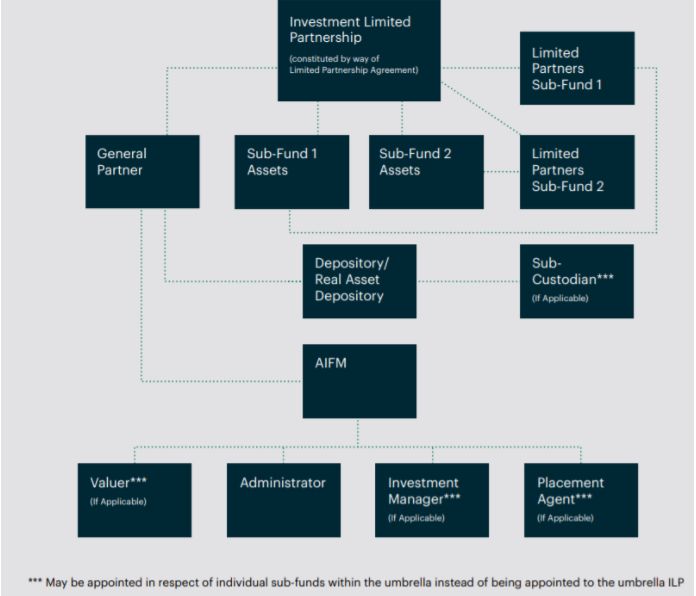

What does an umbrella ILP look like?

The basic arrangement for an umbrella ILP - without considering additional structure features such as feeder vehicles, parallel vehicles, co-investments or subsidiaries - is illustrated in the diagram below.

Footnotes:

1 While it is possible to create both open-ended sub-funds and closed-ended sub-funds within the same umbrella ILP, in practice we typically see sub-funds with the same liquidity profile being established within an umbrella fund due to difficulties which arise when drafting the limited partnership agreement for an umbrella ILP which houses both open-ended and closed-ended sub-funds.

2 This will include any investment management fee which is discharged directly out of the assets of the relevant sub-fund.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.