In a significant change for Swiss business, the recent revisions to the Code of Obligations (CO) impose potentially significant challenges on all Swiss companies. Companies must implement an appropriate internal control system and adequately document it.

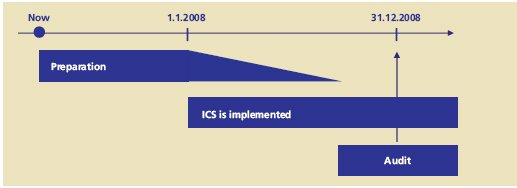

The effective date foreseen is 1 January 2008 – the rules will apply to financial years beginning on or after this date. The auditor must express an opinion on whether the internal control system (ICS) exists. For calendar year end companies, this means the report on the December 2008 financial statements. The vast majority of the companies in the Swiss trading and shipping industry are incorporated as local SAs or SARLs, and are therefore affected by these changes.

What's needed?

The requirements of the law are very brief (see panel). In addition to the law itself, position papers have been issued on behalf of Swiss business (by SwissHoldings) and the accounting profession (Chambre Fiduciare). These consider that an ICS is:

- proportionate to the size of, and nature of business conducted by the company;

- taking specific business risks of the company into consideration;

- suitable for audit;

- adequately documented;

- familiar to, and being applied by, the personnel involved; and

- ultimately the responsibility of the board of directors.

Whilst these outline requirements of the law are well known, however, the practical steps which businesses must take will vary from company to company. An effective ICS is more than merely complying with legal regulation. A well designed system can bring significant business benefits. It can support the board of directors and management through:

- effective management of the company's operations;

- easier compliance with laws and regulations;

- protection of assets;

- reaching company goals and objectives;

- identification of errors and irregularities or fraud; and

- maintenance of accurate accounting records and reliable financial reporting

This is critical in the trading and shipping industry. The "bread and butter" of the trading companies is management of the core trading transactions and their recording in the income statement. These are always closely managed. The complexities of accounting standards (particularly IAS 39 on financial instruments, or its US GAAP equivalent) can, however, cause significant balance sheet swings which may receive less day to day focus. Industry risks are generally understood and managed, but, in some organisations, the control processes are not necessarily formalised.

|

Key extracts from the Code of Obligations CO 716a

... 3. the structuring of the accounting system and of the financial controls as well as the financial planning insofar as this is necessary to manage the company. CO 728a

... 3. an internal control system exists |

What does this mean in practice?

The expected effective date of 1 January 2008 does not leave a lot of time to take the necessary steps. So, if you have not started already, do not delay. The implementation, adaptation and conversion of existing systems may require a significant amount of time.

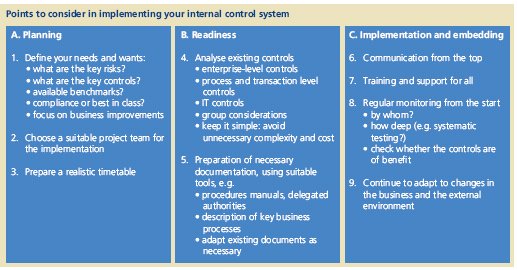

To use ICS implementation to bring business benefits, as well as compliance, it may help to consider the following points

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.