From 1 January 2013, several crucial amendments to the mechanism for taxing oil and gas production will become effective. In particular, they will affect the current system of royalty payments and subsoil-use charges.

Oil and gas production is currently taxed using two principal mechanisms: monthly royalty payments on each type of produced hydrocarbons, and a second subsoil tax – the charge for subsoil use – paid quarterly. The subsoil-use charge sets charges for the extraction of oil, condensate, and natural gas, including solution gas (associated petroleum gas) ethane, propane, butane, coalbed methane, shale gas, basin-centred gas and tight gas.

On 24 May the Ukrainian parliament passed Law No. 4834-VI "On Amendments to the Tax Code of Ukraine to Improve Certain Tax Provisions", which came into force on 1 July 2012. From 1 January 2013, this law ends the system of royalty payments and changes the mechanism for calculating the charge for subsoil use, whilst also increasing the charge. There will also be a new payment mechanism and high penalties for non-compliance.

A second law was passed by the parliament on 5 July 2012, slightly amending the rates of the charge. This law – Law No. 5083-VI "On Amendments to the Tax Code of Ukraine and the State Tax Service in Connection with Administrative Reform" – came into force on 12 August 2012.

As a result of both laws, the charge for subsoil use will be calculated as:

the Volume multiplied by the Price (per unit) and the Rate and the Adjusting Index.

(a) The Volume is the volume of hydrocarbons extracted during the quarterly reporting period.

(b) The Price (per unit) is either the effective price or the estimated value, whichever is higher:

(i) The effective price for natural gas will be published by the Ministry of the Economy within 10 days following the end of the quarter and will be equal to the average customs value of the natural gas imported into Ukraine over the quarter.

(ii) The effective price for oil and condensate will be established and published by the Ministry of Economy as the average price of 1 barrel of Urals oil at the International Petroleum Exchange (London) over the quarter in UAH per ton, using the exchange rate set by the National Bank of Ukraine on the 1st day of the month following the quarter.

(iii) The estimated value for natural gas, oil and condensate will be calculated using the volume of extracted minerals, expenditures (calculated in a manner prescribed by the Tax Code of Ukraine) and the profitability ratio (indicated in the documents containing estimations of the minerals reserves approved by the State Commission on Minerals Reserves).

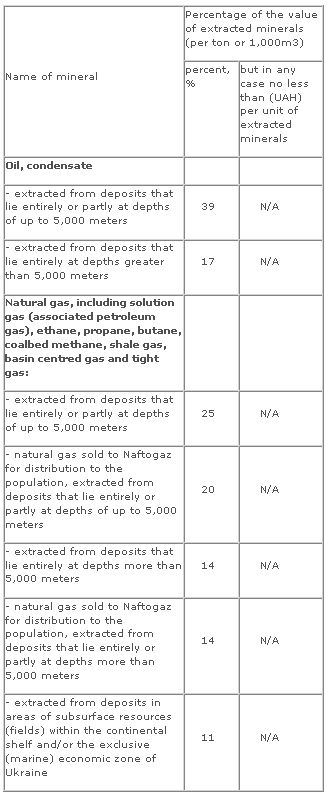

(c) The Rates for natural gas, oil and condensate will be as follows:

(d) Under production sharing agreements a rate of 2% will be applicable to the volumes of extracted oil and condensate, and a rate of 1.25% will be applicable to the volumes of the extracted natural gas (including solution gas (associated petroleum gas), ethane, propane, butane, coalbed methane, shale gas, basin centred gas and tight gas).

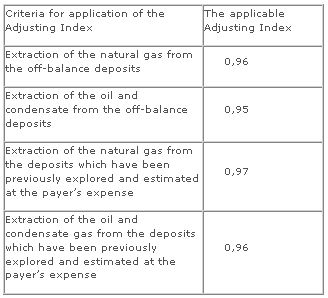

(e) The Adjusting Indexes depend on type of the deposit which is explored and/or developed and include the following:

LAW: the Law of Ukraine No. 4834-VI "On

Amendments to the Tax Code of Ukraine to Improve Certain Tax

Provisions" dated 24 May 2012 and the

Law of Ukraine No. 5083-VI "On

Amendments to the Tax Code of Ukraine and the State Tax

Service in Connection with Administrative Reform" dated 5 July

2012.

This article was written for Law-Now, CMS Cameron McKenna's free online information service. To register for Law-Now, please go to www.law-now.com/law-now/mondaq

Law-Now information is for general purposes and guidance only. The information and opinions expressed in all Law-Now articles are not necessarily comprehensive and do not purport to give professional or legal advice. All Law-Now information relates to circumstances prevailing at the date of its original publication and may not have been updated to reflect subsequent developments.

The original publication date for this article was 11/09/2012.