Background

The Oman Government has published the VAT law in the official Gazette on 18 October 2020. Oman is the fourth GCC country to implement VAT after KSA, UAE and Bahrain. This law will come into effect 180 days from the date of publication. i.e. 16 April 2021.

It is expected that the Executive Regulations to the abovementioned law can be issued by Tax Authority (not cabinet) by December 2020. Considering the timeline of VAT implementation, businesses would have roughly six months to prepare.

The main milestones to be noted and acted upon would be as below:

- December 2020: Publication Executive Regulations

- January 2021: Opening Registrations

- April 2021: Implementation of VAT

- 30 June 2021 (expected): Filing of the first VAT return

Considering the above timeline, a crucial role would be to identify a Partner that can manage the following activities.

- Forming an internal VAT project group;

- Creating VAT Awareness internally;

- Conducting detailed VAT Impact Assessment;

- Ensuring correct IT infrastructure including ERP is setup; and

- Review of vendor, customer and internal contracts.

VAT in Oman, similar across the globe, would be a tax on consumption that would require to be paid and collected at every stage of the supply chain.

VAT would be imposed on a taxable person1 in accordance with the Agreement.

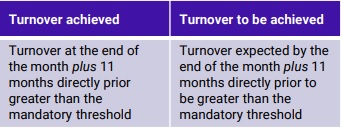

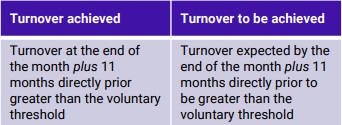

Determine the registration criteria and thereafter, assess the nature of registration to be obtained. Businesses would have to determine the application of threshold from October 2020 itself.

Liability to obtain registration

Mandatory (OMR 38,500 ~ USD 100,000)

Turnover greater than Mandatory Registration threshold:

Voluntary (OMR 19,250 ~ USD 50,000)

Turnover greater than Voluntary Registration threshold:

Businesses should undertake a feasibility study before proceeding to register for VAT Group Registration

Registration as a VAT group

- Two or more persons may register with the Authority as a tax group, according to the conditions determined by the Regulation;

- The tax group is treated, for the purposes of implementing the provisions of this Law, as a separate Taxable Person from the members of the group;

- The members of the tax group shall be jointly responsible for the tax obligations of the group which arise during the period of their joining.

Identify the nature of transactions carried out and determine whether they are Goods or Services

Transaction taxable under Oman VAT law

Taxable Transaction:

- The supply of Goods or Services by a Taxable Person in the Sultanate;

- Deemed supply of Goods/Services;

- Goods or Services received by a Taxable Customer supplied by a Non-Resident who is not a Taxable Person in the Sultanate (i.e. cases wherein the Reverse Charge Mechanism applies);

- Import of Goods.

The following are considered as a Supply of Goods:

- Alienation of Goods, for purposes other than Economic Activity, whether subject to Consideration or not;

- Changing the use of Goods to use them for nontaxable Supplies;

- Retaining Goods after ceasing to carry on an Economic Activity; and

- Supplying Goods without Consideration, unless these are supplied with a connection to the activity, such as gifts or free samples, as determined by each Member State.

The following is considered a Supply of Services:

- The use by a Taxable Person of Goods that form part of his assets, without Consideration, for purposes other than those of an Economic Activity; and

- Supplying Services without Consideration.

To examine whether Goods or Services supplied shall classify as an exempt supply

Transaction exempt from levy of VAT under Oman VAT law

The following shall be considered as Exempt supplies:

- Financial services

- Provision of healthcare and associated Goods and Services

- Provision of education and associated Goods and Services

- Undeveloped lands (bare lands)

- Resale of residential real estate

- Local passenger transport

- Renting real estate for residential purposes

The above shall be exempt from the Tax, in accordance with the conditions and controls determined in the Regulation:

Imported goods which are exempted:

- The Import of Goods in cases in which the supply of these Goods is exempt from Tax; or

- Subject to Tax at a zero rate in the Country of Final Destination;

- Imported Goods for the use of diplomatic and consular bodies and international organizations, and for the heads and members of the diplomatic and consular corps accredited by the Sultanate, on the condition of reciprocity;

- Goods imported for the armed and security forces in all sectors, such as ammunition, weapons and military transportation means and equipment;

- Used personal items and household appliances brought by citizens residing abroad, and foreigners who are coming to reside in the country for the first time;

- Necessities of non-profit associations;

- Returned Goods.

The exemption is in accordance with the conditions and controls stipulated in the Common VAT Agreement.

Footnotes

1 Person would include an individual, company, joint venture, or partnership etc.

To read the full article click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.