The Luxembourg draft law N° 7020 (the "Draft Law") submitted by the Luxembourg government to the Luxembourg Parliament on 26 July 2016 foresees the introduction of tax measures affecting both individual and corporate taxpayers.

The Luxembourg law on tax reform was passed on 14 December 2016. In terms of process, the Council of State should provide its exemption of the second vote by next week around the 23 December. The Grand Duke has to sign the law in order for it to be published in the Official Journal. Once the Draft Law enacted, most of the measures are expected to enter into force from 1 January 2017 onwards with exception to certain measures that would be applicable for the current fiscal year. You will find the key measures foreseen by the Draft Law summarized below.

FOCUS ON TAX MEASURES FOR INDIVIDUALS - WHAT IS GOING TO CHANGE FOR YOU?

The individual income tax measures aim to reinforce households' spending powers and can be summed up in 3 words: "Durability, Justice and Selectivity ". (Source : CES – analyse des données fiscales)

1. Employment income: two main changes

The changes affect notably 2 subjects : Lunch vouchers (art. 140 LIR) and company cars

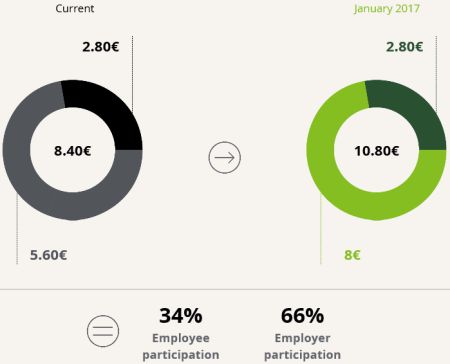

- Luncheon

Vouchers

This would have a positive net impact on purchasing power for employees.

- Benefit in kind for Company

cars

This new measure would aim to reinforce sustainable mobility, to reduce carbon emission with the aim to protect our environment by reducing the taxable benefit in kind for "more green" cars and to increase it for more polluting cars.

Major Objectives:

To read this article in full, please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.