The UK Government has introduced two new 'corporate criminal offences', enabling the easier prosecution of businesses which fail to prevent the facilitation of UK or overseas tax evasion. This legislation applies to all companies and partnerships ("businesses") that fail to prevent the facilitation of UK tax evasion by their employees, suppliers, contractors or other associates. The rules come into force in September 2017. It also extends to overseas tax evasion where this would have been a crime in the UK.

Putting tax offence on your radar

This latest legislation from the UK Government is one of an expanding list of domestic and international initiatives focussing on tax transparency and governance of tax risk.

Businesses will be automatically deemed liable for the facilitation of tax evasion by an associate, unless they can prove that they had 'reasonable procedures' to prevent such facilitation in place at the time the facilitation offence occurred. In addition to the risk of reputational damage, significant penalties accompany this legislation, including unlimited financial penalties, confiscation orders and serious crime prevention orders.

Establish your set of 'reasonable procedures'

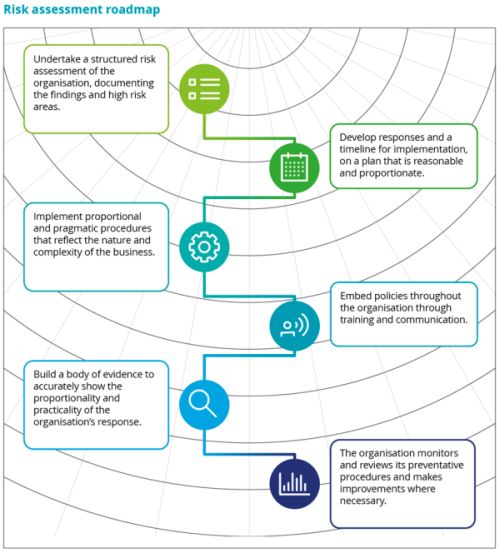

Before the legislation comes into force later this year, businesses should establish a set of 'reasonable procedures'. HMRC acknowledges what constitutes 'reasonable' will continually evolve over time, but currently there are six guiding principles which would underpin any defence. These are:

- Risk assessment

- Proportionate procedures

- Top level leadership

- Due diligence

- Training and communication

- Monitoring and review.

Complete your risk assessment now

Deloitte recommends that all businesses potentially within the scope of the rules complete a risk assessment in the first half of 2017 to help them better understand where they may be at risk of facilitating any tax evasion and to allow time to respond before the legislation comes into force.

Risk Assessment roadmap

Join us for a webcast on this new measure

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.