In the wake of the financial crisis, the US Securities and Exchange Commission adopted detailed data reporting rules for private funds on both Form ADV (2010) and Form PF (2011). In its continuing push to gather more asset management industry data, agency officials have been hinting for months that portfolio-level reports on investment adviser separate accounts and registered investment companies would be next. The agency now intends to close these perceived gaps through a pair of rule proposals that it announced on May 20, 2015.

What does the SEC do with the data it collects? The agency says better data allows it to more effectively monitor industry trends and assess risk, focus its examinations, conduct investigations and, when necessary, bring enforcement actions. Collecting more industry data also serves the SEC's political interest in protecting its position against other financial regulators. Lest anyone miss that point, the agency opens the registered investment company reporting proposal with the unqualified assertion that "the Commission is the primary regulator of the asset management industry."

This alert describes the proposed separate account reporting requirements, which the SEC packaged with a series of related investment adviser disclosure requirements, a proposed codification of SEC staff positions that provide for so-called "umbrella registrations" by closely related advisory firms, and proposed recordkeeping rule changes for communications that include statements of investment performance. A companion alert describes the SEC's proposed registered investment company reporting rules.

The SEC is soliciting comments on its rulemaking proposals. Comments are due within 60 days following publication of the proposals in the Federal Register.

New Separate Account Data Reporting

Currently, the SEC collects only limited data from investment advisers regarding their separately managed client accounts.1 Under proposed amendments to Form ADV, which is the SEC's registration form used by investment adviser firms,2 an SEC-registered adviser would provide certain aggregate information on separately managed accounts it advises, including information on regulatory assets under management (RAUM), types of investments, and use of derivatives and borrowings. For purposes of the new reports, the SEC will consider as a separately managed account any advisory account that is not a pooled investment vehicle.

The proposed amendments would capture information that the SEC says is comparable to information the agency already collects on Form PF regarding private funds.3 Specifically, registered investment advisers are proposed to:

- Report the approximate percentage of separately managed account RAUM invested in ten broad asset categories, such as exchange-traded equity securities and US government/agency bonds.

- Identify any custodians that account for at least 10% of separately managed account RAUM and the amount of the adviser's RAUM attributable to separately managed accounts held at each custodian.

- Report on the use of borrowings and derivatives in any separately managed account having a net asset value of at least $10 million, as follows.

- All advisers would report the percentage of these separately managed account assets held in derivatives.

- Advisers with at least $150 million but less than $10 billion in RAUM attributable to separately managed accounts would report the number of accounts that correspond to certain categories of gross notional exposure,4 and the weighted average amount of borrowings (as a percentage of net asset value) in those accounts.

- Advisers with at least $10 billion in RAUM attributable to separately managed accounts would report the gross notional exposure and borrowing information described above, as well as the weighted average gross notional value of derivatives (as a percentage of the net asset value) in each of six different categories of derivatives.

All advisers would report this separate account information annually. Advisers with at least $10 billion in RAUM would report both mid-year and year-end information, but only as part of their annual filing. While no separate semi-annual filing is proposed, the agency requests comment on whether to require updated separate account information each time that an amended Form ADV is filed – a requirement that, if part of the final rules package, could add significantly to the burden associated with the non-ordinary course update filing that most advisers find necessary from time to time.

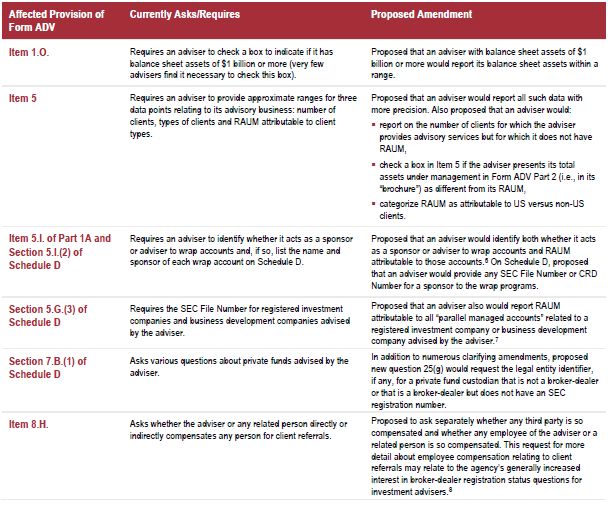

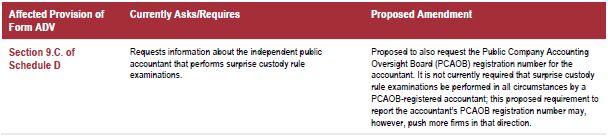

Other Proposed Additions to Form ADV

In addition to the proposals above concerning separate account information, the SEC's revisions to Form ADV would add new questions and amend existing questions on Part 1A of the form. Unlike the separate account information proposals, which appear to affect only registered investment advisers and not "exempt reporting advisers" (because exempt reporting advisers do not complete Item 5 of Form ADV, where the new requirements will be housed, the remaining changes to the form will affect all Form ADV filers.

The following table lists these proposed changes. 5

Umbrella Registration

For a variety of tax, legal and regulatory reasons, investment adviser firms may be organized as a group of related advisers that are separate legal entities but effectively operate as a unified advisory business. Recognizing that a single group registration often will be less confusing and more efficient than would multiple, repetitive filings, SEC staff positions allow related entities to share a single SEC registration, subject to certain conditions.9

The SEC now proposes to codify the existing staff guidance. The proposed group registration rules would use the same terminology used by the staff to date, which refers to a "filing adviser" filing a single Form ADV on behalf of itself and other so-called "relying advisers" in the group that are controlled by or under common control with the filing adviser and that effectively conduct a single advisory business (collectively an "umbrella registration").10 Conditions to rely on an umbrella registration would be as follows:

- The filing adviser and each relying adviser advise only private funds and clients in separately managed accounts that are qualified clients (as defined in rule 205-3 under the Advisers Act) and are otherwise eligible to invest in the private funds advised by the filing adviser or a relying adviser and whose accounts pursue investment objectives and strategies that are substantially similar or otherwise related to those private funds;

- The filing adviser has its principal office and place of business in the United States and, therefore, all of the substantive provisions of the Advisers Act and the rules thereunder apply to the filing adviser's and each relying adviser's dealings with each of its clients, regardless of whether any client or the filing adviser or relying adviser providing the advice is a United States person;11

- Each relying adviser, its employees and the persons acting on its behalf are subject to the filing adviser's supervision and control and, therefore, each relying adviser, its employees and the persons acting on its behalf are "persons associated with" the filing adviser (as defined in section 202(a)(17) of the Advisers Act);

- The advisory activities of each relying adviser are subject to the Advisers Act and the rules thereunder, and each relying adviser is subject to examination by the Commission; and

- The filing adviser and each relying adviser operate under a single code of ethics adopted in accordance with rule 204A-1 under the Advisers Act and a single set of written policies and procedures adopted and implemented in accordance with rule 206(4)-(7) under the Advisers Act and administered by a single chief compliance officer in accordance with that rule.12

These conditions track SEC staff guidance from the 2012 ABA Letter. The SEC also makes several points in the current rulemaking that address areas in which there has been mixed industry practice to date. Notably, the SEC is clear that umbrella registration as proposed is available only to fully registered advisers and not to "exempt reporting advisers."

Currently, Form ADV does not contemplate the group registration model, leaving group filers to develop ad hoc reporting formats as they complete the form. To address this lack of standardization, the SEC proposes to add a new Schedule R to Form ADV, which would request the following, to be completed separately for each relying adviser:

- Name(s) and address(es)

- CRD, CIK and legal identifier numbers

- Basis for being a registered investment adviser (that each relying adviser must either independently meet the minimum assets under management requirements for SEC registration or share an address with a related registered adviser is not a new requirement, but having to affirmatively check a box on the form to that effect highlights it)

- Form of organization

- Fiscal year-end

- Officers, owners and other control persons (each relying adviser will now complete its own version of Form ADV Schedules A and B, representing another potentially significant change from current practice).

Proposed Amendments to Investment Advisers Act Rules

The SEC proposes two amendments to Advisers Act Rule 204-2, the books and records rule, which would require investment advisers to maintain additional materials related to the calculation and distribution of performance information.

Rule 204-2(a)(16) currently requires registered advisers to maintain records supporting performance claims in communications that are distributed or circulated to ten or more persons. The proposal removes the "ten or more persons" condition, such that supporting records would be required for any such communication, even if used with a single person.

Rule 204-2(a)(7) currently requires registered advisers to maintain certain categories of written communications received and copies of written communications sent by such advisers.13 The proposed amendments would require advisers to also maintain originals of all written communications received and copies of written communications sent by an investment adviser relating to the performance or rate of return of any or all managed accounts or securities recommendations.

Conclusion

These proposed changes are significant and can be expected to be the subject of a broad range of public comments. We will continue to track and report on the rulemaking as it progresses.

Footnotes

1 Form PF collects data on private fund parallel managed accounts. Form PF and its instructions are available at https://www.sec.gov/about/forms/formpf.pdf .

2 Form ADV filings are available to the public through the Investment Adviser Public Disclosure System (IAPD) at http://www.adviserinfo.sec.gov .

3 While the requested data may be broadly similar, Form PF filings are non-public, whereas the data now proposed to be collected on managed accounts on Form ADV would be publicly available.

4 Gross notional exposure is the percentage obtained by dividing (i) the sum of (a) the dollar amount of any borrowings and (b) the gross notional value of all derivatives, by (ii) the net asset value of the account.

5 The SEC also proposes to add a number of clarifying instructions to various questions in Form ADV. We generally do not summarize those proposed clarifications in this alert.

6 Form ADV, Glossary defines a wrap fee program as "[a]ny advisory program under which a specified fee or fees not based directly upon transactions in a client's account is charged for investment advisory services (which may include portfolio management or advice concerning the selection of other investment advisers) and the execution of client transactions." The SEC does not propose any changes to this definition.

7 Proposed Form ADV, Part 1A, Section 5.G.(3) of Schedule D. "Parallel managed account" would be defined as: "With respect to any registered investment company or business development company, a parallel managed account is any managed account or other pool of assets that you advise and that pursues substantially the same investment objective and strategy and invests side by side in substantially the same positions as the identified investment company or business development company that you advise." See Proposed Form ADV Glossary.

8 We previously reported on a widely-cited SEC staff speech in this area. See our 2013 alert available at http://www.shearman.com/en/newsinsights/publications/2013/04/sec-lawyer-speaks-to-brokerdealer-registration-s__.

9 See American Bar Association Business Law Section, SEC Staff Letter (Jan. 18, 2012), available at https://www.sec.gov/divisions/investment/noaction/2012/aba011812.htm (the 2012 ABA Letter). The Division of Investment Management also provided earlier no-action relief to enable a special purpose vehicle that acts as a private fund's general partner or managing member to essentially rely upon its parent adviser's registration with the Commission rather than separately register. See American Bar Association Subcommittee on Private Investment Entities, SEC Staff Letter (Dec. 8, 2005), available at http://www.sec.gov/divisions/investment/noaction/aba120805.htm (the 2005 ABA Letter). The 2005 ABA Letter is understood to provide its own basis for not separately registering entities. It was not superseded by the later 2012 ABA Letter and also does not appear to be affected by the current rulemaking.

10 "Filing Adviser" would mean: "An investment adviser eligible to register with the SEC that files (and amends) a single umbrella registration on behalf of itself and each of its relying advisers." "Relying Adviser" would mean: "An investment adviser eligible to register with the SEC that relies on a filing adviser to file (and amend) a single umbrella registration on its behalf." "Umbrella Registration" would mean: "A single registration by a filing adviser and one or more relying advisers who collectively conduct a single advisory business and that meet the conditions set forth in General Instruction 5." See Proposed Form ADV Glossary.

11 The SEC does not apply most of the substantive provisions of the Advisers Act to the non-US clients of a non-US adviser registered with the Commission. See Exemptions for Advisers to Venture Capital Funds, Private Fund Advisers With Less Than $150 Million in Assets Under Management, and Foreign Private Advisers, Investment Advisers Act Release No. 3222 (June 22, 2011) [76 FR 39646 (July 6, 2011)], at section II.D. The Glossary to Form ADV provides that "United States person" has the same meaning as in rule 203(m)-1 under the Advisers Act, which includes any natural person that is resident in the United States.

12 Under this approach, the code of ethics and written policies and procedures must be administered as if the filing adviser and each relying adviser are part of a single entity, although they may take into account, for example, that a relying adviser operating in a different jurisdiction may have obligations that differ from the filing adviser or another relying adviser.

13 Rule 204-2(a)(7) currently requires advisers to make and keep: "Originals of all written communications received and copies of all written communications sent by such investment adviser relating to (i) any recommendation made or proposed to be made and any advice given or proposed to be given, (ii) any receipt, disbursement or delivery of funds or securities, or (iii) the placing or execution of any order to purchase or sell any security."

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.