In 2018, the SEC continued to pursue many of the same initiatives and objectives it articulated in 2017, including emphasizing retail investor protections and keeping pace with technological change. While stand-alone enforcement actions increased in 2018, the number of financial reporting or disclosure cases continued to decline. Consistent with its public statements and despite its resource constraints in 2018, the SEC seems to be prioritizing financial reporting, internal controls, and disclosure cases impacting "Main Street" investors, particularly those involving other programmatic priorities such as crypto technologies and cybersecurity. Regardless, public companies should remain vigilant regarding potential risks, and continue to implement and maintain strong, robust controls.

We are pleased to present our semi-annual review of enforcement activity relating to financial reporting and issuer disclosures. Much like prior updates, this paper focuses principally on the Securities and Exchange Commission ("SEC") but also discusses other relevant trends and developments.

In 2018, the SEC continued to pursue many of the same initiatives and objectives it articulated in 2017, including initiatives to: (i) focus on the Main Street investor; (ii) focus on individual accountability; (iii) keep pace with technological change; (iv) impose remedies that the SEC believes most effectively further enforcement goals; and (v) constantly assess the allocation of its resources. According to the Division of Enforcement's ("Division") year-end overview, enforcement activity increased in 2018. Overall, the number of enforcement actions rose from 446 stand-alone actions the year prior to 490, a nearly 10 percent increase.1

As noted in our January 2018 update, 2017 was a transition year for the SEC, with the appointment of new SEC chairpersons and a shift in enforcement priorities. In their year-end overview, the Division's Co-Directors pointed out that the increased enforcement activity in 2018 was accomplished despite "significant challenges," including shrinking personnel resources and limitations on disgorgement remedies due to the Supreme Court's ruling in Kokesh v. SEC. In light of these challenges, the SEC's senior leaders reiterated on multiple occasions in the latter half of 2018 that the SEC is focused on the "quality" and deterrent effect of cases rather than quantity.2

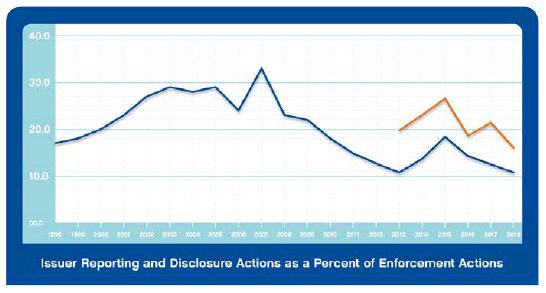

Though stand-alone enforcement actions increased in 2018, the number of financial reporting or disclosure cases continued to decline. Only 79 of the 490 stand-alone actions in 2018 were focused on issuer reporting and disclosure, as opposed to 95 of the 446 enforcement actions in 2017.3 Taking a longer historical perspective, financial reporting and disclosure matters as a percent of all enforcement matters (10.6%) or as a percent of independent enforcement matters4 (16%) were at their lowest level since 1998, and well below their averages of 20 percent and 21 percent, respectively.5 As noted in prior updates, this decrease may be attributable, in part, to the SEC's channeling of "enforcement resources to cases that may involve smaller penalty numbers, but really affect Main Street investors' lives."6 In other words, financial reporting and disclosure matters may just not be a priority right now, especially in the resource-constrained environment in which the SEC currently operates.

Importantly, however, even as the SEC takes a more circumspect approach to the allocation of its resources, changes in the number or types of enforcement actions should not be interpreted as signals that the SEC lacks the will or means to pursue its enforcement mandate. Public companies and their directors should continue to approach investigative risks in financial reporting and internal control effectiveness with the same caution as always. The robust control environments that companies have designed and implemented in the past continue to be as important as ever.

Footnotes

1. SEC Division of Enforcement, Annual Report 5 (Nov. 2, 2018).

2. Stephanie Avakian, Co-Director, SEC Division of Enforcement, "Measuring the Impact of the SEC's Enforcement Program" (Sept. 20, 2018); Hester M. Peirce, Commissioner, SEC, "Lies and Statistics: Remarks at the 26th Annual Securities Litigation and Regulatory Enforcement Seminar" (Oct. 26, 2018); Steven Peikin, Co-Director, SEC Division of Enforcement, "Remedies and Relief in SEC Enforcement Actions" (Oct. 3, 2018).

3. Annual Report, supra note 1, at 19.

4. A metric the SEC began reporting in 2013.

5. This data is as reported by the SEC and is maintained by the authors. There seem to be a number of different ways of counting cases, but, for these purposes, we rely on the data as reported and classified by the Division as "Issuer Reporting and Disclosure" in its year-end review.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.