I. Introduction

Continuing care retirement communities (CCRCs) are professionally managed retirement communities, many of which also function as long-term skilled nursing care facilities. CCRCs offer residents lifestyle amenities and coordinated social activities as well as various degrees of medical care and assisted-living services. CCRCs generally provide residents with progressive levels of care, ranging from independent living to assisted living to skilled nursing care. This tiered-care approach permits residents to increase their level of assistive services as needed, based on changes in their mental or physical health.

Not all CCRCs are operated in the same manner. For example, skilled nursing services may be offered either onsite or offsite and sometimes are provided through a referral agreement with a third party. The costs associated with residing at a CCRC may vary significantly depending on the continuing care agreement offered by the CCRC.1 Further, some CCRCs allow for sharing of the appreciation or risk of downside in the value of the unit. Thus, there is no one-size-fits-all model for CCRCs.2

Before entering a CCRC, residents generally execute a continuing care agreement setting forth the terms and conditions of their residence at the CCRC. Under a typical agreement, a resident is required to pay a one-time up-front entrance fee and recurring monthly fees in order to reside at the CCRC. Entrance fees may be refundable in whole or in part if a resident leaves the community or upon the resident's death. Monthly fees generally reflect the cost of operating the CCRC, and can cover items such as meals, housekeeping and laundry services, utilities, maintenance, appliances and emergency services. Unlike entrance fees, monthly fees are generally not refundable. Some states regulate the payment and use of entrance and monthly fees.3

The dual lifestyle and medical care aspects of many CCRCs lead to questions regarding the tax treatment of fees paid to the facility, both for residents and for the CCRCs. The tax treatment of these fees is discussed below.

II. Tax Consequences to the Resident

From the perspective of CCRC residents, the relevant questions are whether a resident is entitled to any deductions related to the payment of entrance and monthly fees and whether a resident paying an entrance fee is subject to the imputed interest rules under IRC § 7872. As explained below, it is well established that portions of such fees may be allowed as deductions; however, each situation is fact specific, and there is no clear-cut methodology for determining the appropriate deduction amount. With respect to IRC § 7872, the available guidance indicates that residents who pay entrance fees generally do not have imputed interest income.

A. Section 213 Medical Care Expenses

Section 213 allows a taxpayer to deduct any amounts of "medical care" expenses that exceed 7.5 percent of the taxpayer's adjusted gross income.4 "Medical care" is generally defined as amounts paid for the costs of (1) "diagnosis, cure, mitigation, treatment, or prevention of disease, or the for the purpose of affecting any structure or function of the body"; (2) medical-related transportation; (3) qualified long-term care services; and (4) insurance covering medical care or qualified long-term care.5 Several IRS rulings and cases have interpreted IRC § 213 in the context of CCRC fees.

IRS Guidance

The IRS first affirmed the appropriateness of IRC § 213 deductions of the medical-cost portions of CCRC fees in a 1966 General Counsel Memorandum,6 advising that it agreed with a proposed letter ruling holding that "[t]he portion of a 'lifetime care fee' allocable to medical care is deductible as a medical expense under section 213, Internal Revenue Code of 1954."7 The memorandum reasoned that the fee was paid pursuant to a legal obligation and assured the residents of lifetime care at no additional cost. The memorandum further advised that the possibility that a portion of the fee could be refunded upon the resident's termination of the contract was not important because any amount refunded would likely have to be included in gross income in the year of refund.

The following year, the IRS issued published guidance8 allowing a medical expense deduction for the portion of a monthly fee paid to a retirement home attributable to the costs of providing medical care, as calculated "on the basis of the home's experience."9 The IRS adopted the principle from a 1954 Revenue Ruling10 that, where a lump-sum fee is charged for several services and a breakdown can be provided showing the amount allocable to medical care, a deduction may be allowed based on that amount.

In 1975, the IRS expanded on these principles by publicly ruling that CCRC residents may deduct the medical portions of CCRC fees in the year of payment even if some amounts may be refunded in later years.11 In consideration for a CCRC's promise of lifetime care, the resident taxpayer made a lump-sum payment, which assured the resident lifetime care at no additional cost. In the event the resident terminated the agreement, the resident would have a conditional right to a partial refund of the life-care fee. Despite the potential for partial refund, the IRS ruled that a portion of the fee was an expense for medical care, because the CCRC demonstrated that it was to cover the obligation to provide medical care and gave the resident a separate statement to that effect. However, the IRS also ruled that any portion of the life-care fee actually refunded to and received by the taxpayer in a later year would have to be included in gross income to the extent attributable to prior deductions.12 The IRS reached the same conclusion the following year, ruling that taxpayers could deduct a portion of the fee that was made in return for the promise to provide lifetime care.13 It also reaffirmed the use of long-term experience of CCRC facilities in determining the appropriate percentage of entrance and monthly fees attributable to medical expenses.

Since 1975, the IRS has consistently ruled in private guidance that portions of monthly and entrance fees shown to be attributable to medical care and expenses are deductible to the extent allowed under IRC § 213.14 As discussed below, the dispute in recent years has turned to what costs are attributable to medical care and whether any portion of an entrance fee is attributable to such care.

1 Case Law

The Tax Court first addressed the deductibility of entrance fees in Est. of Smith.15 There, the taxpayer agreed to pay an entrance fee of $20,460 and a monthly fee of $280 in exchange for a lifetime lease of an apartment at a retirement facility. Pursuant to the terms of the residency agreement, the facility agreed to provide services such as medical insurance, carpets, laundry, appliances, maintenance and utilities. A resident was entitled to 30 days' standard care at a convalescent and rehabilitation center, plus 10 additional days of such care for each full year of continuous residency. The taxpayer moved into the facility in 1976, immediately became sick and was moved to the center for the next two years until he died. A medical expense deduction was claimed based on the full amount of the entrance fee. The IRS determined that no deduction was allowable with respect to the entrance fee, but that a small amount was deductible with respect to other payments that reflected the cost of providing medical insurance.

The Tax Court found that the retirement community provided no direct medical services, the convalescent center was a separate establishment, and the taxpayer did not move into the facility for medical care. It therefore concluded that, to the extent the entrance fee was for lodging and other services provided to residents of the retirement community, it was not deductible. However, the court found that 7 percent of the entrance fee, which the parties agreed was attributable to the promise to provide free days of care in the convalescent center, was deductible in the year of payment and not, as the IRS argued, in the year services were actually rendered. The court reasoned that the obligation to pay the fee was incurred at the time the agreement was entered into and was in return for the community's promise to provide not only lifetime lodging and various services, but also free medical care. The IRS has acquiesced in Est. of Smith.16

In Finzer,17 the Northern District of Illinois recently addressed the deductibility of entrance fees in a refund context. There, the taxpayers had originally deducted 18.9 percent of their 90 percent refundable entrance fee. They subsequently filed an amended return seeking a refund based on a deduction equal to 41 percent of the entrance fee. Because the limitations period for disallowing the amount deducted on the original return had expired, the sole issue was whether the taxpayers could prove that they were entitled to deduct any amount above what was claimed on their original return. The district court interpreted the residency agreement as providing that the entrance fee did not relate to medical care; rather, it was the monthly fee that covered the medical expenses. It found that the entrance fee was structured as a loan and that the CCRC "always" returned at least 90 percent of the entrance fee. The court ultimately concluded that "because the entrance fee is a loan, it cannot serve as the basis for a deduction for the Finzers," and therefore no additional medical expense deduction was allowable.18 The district court also distinguished prior rulings because it believed that portions of the entrance fees in those rulings "may" have been refundable, as opposed to the situation before it where a portion "would" have to be refunded.19

The Tax Court recently addressed the deductibility of monthly fees in Baker.20 Given the IRS's consistent position (which it adhered to in that case) that a medical expense deduction may be allowed for the portion of a monthly fee attributable to medical care, the issue in that case focused on the proper methodology for determining the deductible amount. That case is discussed in detail below.

B. Determining the Amount Attributable to Medical Expenses

Some CCRCs provide residents with an estimate of the percentages of entrance and monthly fees attributable to medical care.21 This percentage can be estimated in several ways, including prior experience, the experience and rates of comparable CCRCs, and the CCRC's particular expense structure. Historically, the IRS and the courts have accepted these methods of calculating individual medical expense percentages.22 Within the statutory law, no provision is made for any uniform method or system of calculation.

During the 1980s, the IRS turned its attention to the proper amount of medical expense deductions claimed by CCRC residents. Private letter rulings from this period considered determining the medical portion of a CCRC's entrance and monthly fees by dividing the facility's "directly related medical expenses," including items such as nursing salaries, maintenance, utilities, interest on indebtedness, housekeeping, real estate taxes, depreciation, administrative costs and marketing costs, by its total expenses.23 Some of these rulings addressed the use of the same percentage by CCRC residents in the same facility but occupying units of different size and price, suggesting that in such cases residents should be required to use a "weighted average" to properly allocate medical expenses.24 However, in 1989 the IRS appeared to retreat from any efforts at independently determining or imposing appropriate medical expense percentages on CCRCs. In PLR 8930024 (Apr. 27, 1989), the IRS stated:

The Service has no published position regarding the method of allocation of the fees between amounts properly deductible as medical expenses and nondeductible portions. Hence, there is no basis to favor one method of allocation over another method. Because this issue is currently under study, no opinion is expressed.

In Baker, the Tax Court was squarely faced with issues of what items constituted medical care and what allocation methods could be used. There, the taxpayers were required under a residence agreement to pay an entrance fee of $130,015 and a monthly fee of $1,418, subject to annual increases by the CCRC. The residence agreement did not indicate how the entrance fee would be used, but the report of the CCRC's auditor indicated that the nonrefundable portion of the entrance fee was recorded as deferred revenue and amortized into income while the refundable portion was reflected as a liability. The taxpayers deducted $34,541 of the entrance fee in 1989, the year they entered the CCRC and paid the entrance fee, and $4,488 and $5,142 of their monthly fees for 1997 and 1998, respectively, the years at issue.

The issue was the appropriate method of calculating the amount of monthly fees attributable to medical care. The CCRC employed a traditional percentage method in which residents claimed medical expense deductions equal to the same percentage of their monthly fees as the medical expenses incurred by the CCRC bore to its total costs. The IRS argued in favor of an actuarial method, in which the facility would first estimate the total operating and capital expenses incurred in relation to fixed assets and then estimate the medical costs each resident would incur, considering survivorship and life expectancy principles, to determine "lifetime total costs" of medical care. These figures would then be applied against monthly service fee amounts to render individualized amounts of prepaid medical care costs deductible under IRC § 213.

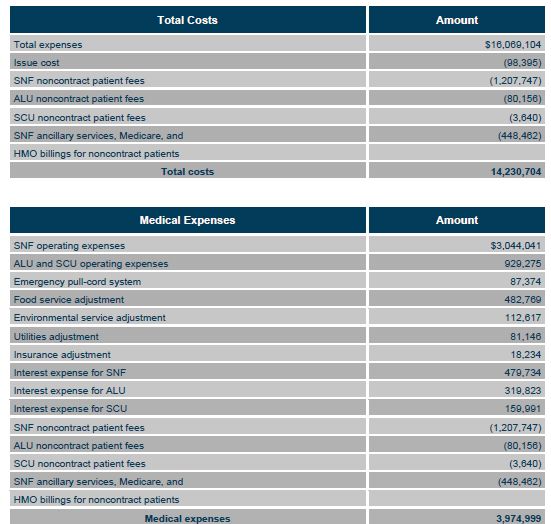

The Tax Court engaged in a lengthy discussion of IRS guidance, both published and private, dealing with the deductibility of entrance fees and monthly fees as medical expenses. The court noted that the public has a right to rely on positions taken by the IRS in published guidance; it cited a number of private rulings to show the IRS's practice and to confirm the IRS's interpretation of its published guidance. Based primarily on this public and private guidance, the Tax Court determined that the taxpayer could use a percentage method (as opposed to an actuarial method) to determine the portion of the monthly fees attributable to medical care. The court then engaged in a detailed analysis of the CCRC's operating expenses and determined the appropriate portion of the monthly fee to be allocated to medical care.25 Under the court's application of the percentage model, each resident would be allocated a standard percentage amount for the purposes of determining the appropriate IRC § 213 deduction; this percentage would be applied based on the number of residents and average weighted monthly service fees in the particular CCRC. Based on this methodology, the court, in an appendix, calculated the applicable medical care allocation for one of the years at issue as follows:

Medical expenses divided by total costs equals an allocation percentage of 27.93 percent.

The number of ILU residents was 574 and they paid a total annual service fee of $7,979,906, or an average of $13,902.

Applying the allocation percentage of 27.93 percent to the weighted average annual service fee of $13,902 results in a medical care allocation of $3,883 per resident.

C. Entrance Fees as Interest-Free and Below-Market Interest Rate Loans

Entrance fees are sometimes structured as loans; however, there is generally no interest element to the loan. In other words, if and when the refund obligation is triggered, the CCRC refunds an amount without any corresponding interest. Section 7872, enacted in 1984, addresses the tax treatment of loans without specified interest rates or bearing an interest rate less than the market rate.26 These loans are referred to as interest-free or below-market interest rate loans.

Section 7872 establishes five categories of below-market loans: gift loans, compensation-related loans, corporation-shareholder loans, tax-avoidance loans and significant-effect loans. In the case of a below-market loan to which the statute applies and which is a gift loan or a demand loan, foregone interest27 is treated as transferred from the lender to the borrower and retransferred by the borrower to the lender as interest.28 The transfer from the lender to the borrower is characterized according to their relationship.29 The corresponding transfers are deemed to have occurred on the last day of each calendar year in which the loan is outstanding.30 For below-market loans that are not gift or demand loans, the lender is treated as having transferred, on the date the loan was made, and the borrower is treated as having received on such date, an amount equal to the excess of the amount loaned over the present value of all payments required to be made under the terms of the loan, discounted to that date using the AFR.31 The lender, however, is treated as receiving the imputed interest amounts ratably over the term of the loan, as with an original issue discount o32

Congress delegated authority to the U.S. Treasury to determine whether a below-market loan was a significant-effect loan.33 Congress intended the term "loan" to be interpreted broadly; thus, "any transfer of money that provides the transferor with a right to repayment may be a loan. For example, advances or deposits of all kinds may be treated as loans."34 When IRC § 7872 was enacted in 1984, neither the statute nor the legislative history addressed or referenced payments to CCRCs. Consequently, it was unclear under the initial statute whether refundable CCRC entrance fee arrangements, characterized as "loans" for purposes of determining gross income, were subject to IRC § 7872. If so, the statute would require CCRCs to recognize as gross income any imputed interest on loan arrangements with residents bearing interest at less than the AFR.

Reactions to Congress' failure to specifically address CCRC entrance fees were swift. Two letters sent in October 1984 to Acting Assistant Treasury Secretary Ronald A. Pearlman, one signed by 21 senators and the other by 58 representatives, expressed concern that IRC § 7872 might require the elderly to pay federal income tax on imputed interest on entrance fees paid to CCRCs. Both letters expressed the view that, for the majority of CCRCs, entrances fees are "clearly not loans," but payments to provide reserves necessary to guarantee that future accommodations and medical care will be made available for the remainder of the residents' lives. The letters urged Treasury to act immediately to issue guidance exempting CCRCs from the application of IRC § 7872, and noted that additional congressional guidance might be necessary on the issue.

In August 1985, Treasury issued proposed regulations on below-market loans.35 Echoing the intent expressed in the congressional letters, Treasury defined the term "loan" broadly to include generally

any extension of credit (including, for example, a purchase money mortgage) and any transaction under which the owner of money permits another person to use the money for a period of time after which the money is to be transferred to the owner or applied according to an express or implied agreement with the owner. The term "loan" is interpreted broadly to implement the anti-abuse intent of the statute. An integrated series of transactions which is the equivalent of a loan is treated as a loan. A payment for property, goods, or services under a contract, however, is not a loan merely because one of the payor's remedies for breach of the contract is recovery of the payment. Similarly, a bona fide prepayment made in a manner consistent with normal commercial practices for services, property, or the use of property, generally, is not a loan; see section 461 and the regulations thereunder for the treatment of certain prepaid expenses and for the special rules of sections 461 (h) and (i). However, a taxpayer's characterization of a transaction as a prepayment or as a loan is not conclusive. Transactions will be characterized for tax purposes according to their economic substance, rather than the terms used to describe them. Thus, for example, receipt by a partner from a partnership of money is treated as a loan if it is so characterized under § 1.731-1(c)(2). Prop. Treas. Reg. § 1.7872-2(a)(1).

Treasury further provided that amounts that are refundable only for a certain period of time or only partially refundable are treated as a loan to the extent of the portion that is refundable and only for the period of time that it is refundable.36 Treasury specifically provided that refundable deposits are not considered loans only if the deposit is custodial in nature (i.e., the transferee is not entitled to the beneficial enjoyment of the deposit, such as when the amount is placed in escrow to secure a contractual obligation of the transferor and the escrow agreement provides that all interest is paid to the transferor).

The proposed regulations indicate that the IRS views entrance fee loans or deposits—clearly not gift, compensation-related or corporation-shareholder loans—as potentially qualifying as significant-effect loans. In discussing significant-effect loans, the IRS identified numerous situations in which below-market loans had the potential to convert nondeductible personal expenses into the equivalent of deductible expenses. One example it provided was "[l]oans to institutions providing meals, lodging, and/or medical services (e.g., continuing care facilities) in lieu of fees for such services." Although it noted that there could be a significant potential for distortion of tax liability, especially if the amounts loaned are relatively large, Treasury concluded that no transaction would be treated under the regulations as a significant-effect loan earlier than the date that future regulations under IRC § 7872(c)(1)(E) were published in proposed form.

In 1985, roughly three months after the issuance of the proposed regulations, Congress amended IRC § 7872 to clarify the application of the below-market loan rules with respect to CCRCs.37 In IRC § 7872(g), Congress excepted loans to qualified CCRCs from the imputed interest rules if the lender (resident) or his or her spouse attains age 65 before the close of the year in which the loan is made, but only to the extent the loan does not exceed a specified dollar amount.38 To the extent loans to CCRCs do not meet the specific criteria set forth in the statute, the below-market loan rules apply.

Following IRC § 7872's proposed regulations and the congressional amendment, the IRS issued limited and conservative guidance on the issue. In PLR 9252015 (Dec. 24, 1992), a CCRC requested a ruling that it was a "qualified continuing care facility" as defined in IRC § 7872(g)(4) and that bonds required to be purchased by residents upon execution of a residency contract were loans. After finding that the CCRC did qualify as a "qualified continuing care facility" because of the level of services provided, the IRS turned to the loan question. Under the residency agreement, a resident was required to purchase a bond and pay a monthly fee. The amount of the bond varied according to the size and type of apartment home chosen and, in the event the agreement was terminated, the CCRC was obligated to repay the face amount of the bond less a deferred fee of 5 percent. The bond was non-transferrable, non-amortizing and non-interest bearing. The resident could terminate the agreement at any time.

The IRS ruled that the bond was a "loan" for purposes of IRC § 7872. In doing so, it noted that the term was meant to be defined broadly and that advances or deposits of all kinds may be treated as loans. The IRS concluded that the bond was a "demand loan" because it was payable at any time on the demand of the resident, and that it was a below-market loan because no interest was required and no payment other than the repayment of principal was due on the amount loaned. The PLR noted that no opinion was expressed or implied as to the federal tax consequences of the transaction under any other provision of the Code.

The IRS reached the same conclusion in TAM 9521001 (May 26, 1995). There, the entrance fee was 90–100 percent refundable when the resident moved out. The CCRC's Resident Information Manual stated that residents paid lower monthly fees because of their entrance fee. There was no loan or deposit agreement, or any other document indicative of a loan. No interest was paid on the entrance fees, and the CCRC used them to repay loans for construction of the retirement facility. To broaden its market niche, the CCRC introduced two additional payment options. Under the first option, the resident would pay a lower entrance fee but an increased monthly fee. Under the second option, the resident would pay no monthly fee and sign a yearly lease for a higher monthly fee (double the amount charged when an entrance fee was also paid). More than 90 percent of the CCRC's residents selected the higher entrance fee option.

The issue was whether "residents who pay the refundable entrance fee [were] taxable on the effective interest earned on their deposits, measured by the difference between the higher monthly fee charged without the payment of an entrance fee, and the lower monthly fee charged with the payment of an entrance fee." The IRS concluded that "[c]learly, residents who pay the refundable entrance fee are in substance loaning the entrance fee to [the CCRC] on an interest-free basis to compensate [the CCRC] for services received, and in turn benefit from a lower monthly fee for those services." The IRS determined that the arrangement might be a "significant-effect" loan, but because it had not yet published final regulations on these types of loans "the loan cannot presently be classified" as such under IRC § 7872(c)(1)(E), and therefore residents were not presently taxable on imputed interest.

The Senate Finance Committee Report on the 1985 amendment, which the Conference Committee Report followed, reflects that Congress believed that it is desirable for individuals to be able to provide in advance for the potential need for increasing levels of personal care through arrangements in which substantial initial payments are refundable, hence providing the individual with greater flexibility than where the payment is not refundable. Congress acknowledged that the below-market loan provisions prescribe the treatment only of transactions that are loans for federal income tax purposes, and that such provisions do not define and did not alter prior law relating to what transactions are or are not to be treated as loans. Thus, Congress understood that payments that are wholly or partially refundable for a relatively brief period (e.g., six months) or refundable on a declining pro rata basis over a longer period (often up to eight years) "ordinarily would be treated as the advance payment of fees and not as loans under present law."

In 2006, Congress enacted IRC § 7872(h), which modified the exception for loans to CCRCs by eliminating the dollar cap on aggregate outstanding loans and lowering the qualifying age of the lender to 62.39 When enacted, IRC § 7872(h) was set to "sunset" at the end of 2010; Congress subsequently made it permanent.40 Thus, for most CCRC residents, payment of entrance fees should not give rise to interest income under IRC § 7872.

III. Tax Consequences to the CCRC

For most CCRCs, the relevant issue is whether the entrance and monthly fees received from residents should be included in gross income and, if so, when. With respect to monthly fees, it is generally established that such fees are includable in gross income in the appropriate year under the CCRC's method of accounting. For entrance fees, the issue is not as well settled, although IRS guidance and case law suggests that any refundable portion of an entrance fee need not be included in income and that any nonrefundable portion need not be included in income until the year in which such portion becomes nonrefundable.41

A. Entrance Fees – Includable or Excludable from Gross Income?

Under IRC § 61(a), gross income is "all income from whatever source derived," including sources such as rent; gross income derived from business; and compensation for services, such as "fees, commissions, fringe benefits, and similar items." Section 61 is purposely broad and meant to be broadly construed; subsection (a) specifically states that gross income includes but is not limited to the types of income enumerated within its text.

In determining whether a particular item constitutes "income" to a taxpayer, the starting point is Glenshaw Glass,42 where the Supreme Court of the United States held that income is any undeniable accession to wealth that is clearly realized and over which the taxpayer has complete dominion. Loans and deposits do not constitute income under the Glenshaw Glass analysis; although the borrower acquires a temporary asset, this is offset by an equivalent liability in the form of the repayment obligation. Accordingly, a loan does not provide a taxpayer with a true accession to wealth and is not included in an individual's gross income for the purposes of calculating federal tax liability.43

From the perspective of CCRCs, the primary tax debate has been whether entrance fees should be characterized as gross income subject to federal tax liability or as non-taxable loans or deposits. As indicated above, the outcome often depends on whether the CCRC is obligated to refund the fee, in whole or part, to the resident or the resident's estate at a future date. The courts and the IRS have examined CCRC entrance fees in at least two discrete contexts: whether entrance fees are advance payments of rent taxable in full upon receipt, and whether entrance fees received by CCRCs funded with tax-exempt bonds are "replacement proceeds" that cause the bonds to be taxable "arbitrage bonds."

I Entrance Fees as Advance Rents

Section 1.61-8(b) of the regulations provides that "gross income includes advance rentals, which must be included in income for the year of receipt regardless of the period covered or the method of accounting employed by the taxpayer." This principle prohibits a landlord taxpayer from collecting rent amounts in advance of their contractual due date while simultaneously recognizing only the amount of rent actually due in the taxable year of receipt for the purposes of calculating federal income tax liability. The IRS has argued on several occasions that CCRC entrance fees represent advance rental payments and therefore constitute gross income when received.44

In July 1973, the IRS issued published guidance for the first time regarding whether certain entrance fees received by a CCRC were includable in gross income in the year of receipt as advance rentals.45 That ruling involved an accrual method CCRC that obtained apartment units and commons areas under long-term lease arrangements and then provided these residential facilities and supporting services to residents pursuant to two contracts. Under the first contract, the resident made a lump-sum payment based on the resident's age in consideration for the CCRC's providing the resident, for the remainder of his or her life, an apartment and the use of social and recreational facilities, laundry facilities, medical facilities and other common facilities. Under the second contract, the resident made monthly payments for services such as meals, laundry, housekeeping, and social and medical care. The ruling does not indicate whether the lump-sum payment was refundable in whole or in part. The specific question addressed in the ruling was whether the lump-sum payments were includable in gross income in the year of receipt or over the actuarially determined life expectancy of the residents. Relying on IRC § 61 and Treas. Reg. § 1.61-8(b), the IRS ruled that the lump-sum payments were includable in gross income in the year of receipt as advance rentals because the payment was "in consideration for an apartment unit and other facilities."

PLR 7307139830A (July 13, 1973) reached the same conclusion, while providing several additional facts. For example, the lump-sum contract is referred to as a "Residential Annuity Agreement" and the monthly-fee contract is referred to as the "Continuing Care Agreement." Additionally, the facts state that the lump-sum payment is refundable in part only (1) during the 90-day initial probationary period during which either party could terminate the contract without cause; (2) upon the resident's death within the first 12 months; (3) where the CCRC for good cause evicts the resident; or (4) where the resident requests to leave and gives 60 days notice. As in Rev. Rul. 73-549, the lump-sum payment was ruled to be consideration for an apartment unit and other facilities. The IRS therefore concluded, as it did in Rev. Rul. 73-549, that the lump-sum payment was an advance rental includible in gross income in the year of receipt.

Almost 20 years later, the IRS again advised that entrance fees had to be included in income in the year of receipt.46 The CCRC in question offered several types of accommodations and services to residents, including the lease of apartments or rooms in a lodge. Under a "Residential Rental Contract," the entrance fee was deemed "earned" (i.e., no longer refundable) by the CCRC as follows:

- 10 percent on the date of occupancy

- 10 percent during the first year, prorated on a monthly basis

- 20 percent each year for the next four years, prorated on a monthly basis

A resident who terminated occupancy was entitled to a refund of the "unearned portion" within 30 days of termination. The CCRC was entitled to offset against the unearned portion any amounts due under other terms of the contract (e.g., amounts owing for the nonpayment of monthly rent). The CCRC used the entrance fees for general repair, maintenance and construction. The taxpayer included the entrance fees in gross income pro rata according to the refund schedules. This tax reporting was consistent with the CCRC's financial reporting requirements.

The IRS stated that the entrance fees had certain characteristics associated with advance rent payments (e.g., based on size of unit, condition of "occupancy" of unit and declining refundability). It determined that the entrance fees were a form of "up-front consideration for the occupancy" of an apartment or a room and therefore were rental payments includible in gross income upon receipt without regard to the CCRC's method of accounting. The IRS rejected the argument that the refund provisions precluded the requisite dominion and control, finding cases on that theory distinguishable because the CCRC was entitled to retain the full entrance fee regardless of whether the resident breached any of his or her obligations under the contract or damaged the premises upon leaving the unit, and ultimately the resident would not be entitled to any refund.

TAM 9246006 appears to have been directed at the taxpayer that was the subject of the subsequent litigation in Highland Farms.47 The Tax Court in that case rejected the IRS's position and held instead that refundable portions of the CCRC entrance fee at issue were not advance payments for services or advance rents.

In Highland Farms, the taxpayer operated a continuing care community and provided different types of accommodations, including apartments. Apartments were available only upon payment of an entrance fee and a monthly fee. The entire entrance fee was paid before the resident moved into the apartment; the entrance fee was not placed in escrow. The monthly fee included the cost of utilities and emergency nursing services, and the taxpayer reserved the right to revise the monthly fee. Residents were charged separately for meals, medical costs and other special services, such as transportation, housekeeping and laundry.

The residency agreement did not specify the length of the agreement. Residents were required to give 120 days' notice before terminating their occupancy. The taxpayer had the right to evict an apartment resident in the following situations:

- The failure to keep financial accounts current

- The creation of an undue hazard to oneself or others

- The failure to abide by the taxpayer's rules and regulations

Under the residency agreement for an apartment, the entrance fee was deemed to have been earned over a period of five years. The first 10 percent of the entrance fee was earned at the time the resident took occupancy. The second 10 percent was earned during the first year of occupancy, prorated on a monthly basis (i.e., 0.83 percent per month). The remaining 80 percent was earned during the following four years, prorated on a monthly basis (i.e., 1.67 percent per month). If a resident terminated the residency contract or died within the first five years, the taxpayer refunded the portion of the entry fee deemed unearned to the resident or the resident's estate. The residency agreement did not provide for the payment of interest on any portion of the entrance fees refunded to residents. For federal income tax purposes, the taxpayer reported as income these same portions of the entrance fees as they became nonrefundable within that tax year and did not recognize as income any portions of entrance fees refunded to its residents.

The IRS challenged the taxpayer's reporting position, arguing that the entrance fees were prepaid rent includable as income in the year of receipt. The Tax Court disagreed. After reciting the applicable legal standards from Indianapolis Power48 and Oak Industries,49 the court succinctly held as follows:50

In the instant case, the residents of the apartments and the lodge, if they decided to move out of their units, had a right to a refund of a portion of their entry fees in accordance with the schedules stated in their respective rental contracts. The refunds were within the residents' control, and petitioner had "no unfettered 'dominion' over the money at the time of receipt." At the time the entry fees were paid, the only amounts petitioner was guaranteed to be allowed to keep were the nonrefundable portions. Thus, we hold that the refundable portions were not advance payments for services or prepaid rent.14 As a result, petitioner is not required to include the entire amount of the entry fees in income in the year of receipt. Only the nonrefundable or nonforfeitable amounts each year constitute income. Petitioner included in income for a specific taxable year those portions of the entry fees for the apartments and the lodge that became nonrefundable or nonforfeitable within that tax year. This method of accounting for the entry fees clearly reflects income. It was an abuse of discretion for respondent to conclude that the fees must be included in petitioner's income for the year of receipt. We hold for petitioner on this issue.

14 The parties submitted expert reports that purported to show the fair market rental value of the units. Neither expert was called to testify, the parties having represented to the Court that their experts had met and reached agreement as to the fair market rental value of the units. A joint exhibit embodying their joint conclusions was prepared and filed with the Court at the conclusion of the trial. That joint exhibit is neither clear nor helpful to the Court, and on brief the parties seem unable to agree as to what their experts supposedly agreed to. The Court has disregarded both parties' expert reports and the experts' joint exhibit. After notice petitioner could increase the monthly rental payments for the apartment or lodge units, without regard to the entry fees. The Court rejects Respondent's suggestion that the entry fees represent prepaid rent that somehow makes up for supposed below market rental rates.

Since its earlier interactions with the tax-related characteristics of entrance fees, the IRS has undergone an apparent shift in its original position on the nature of entrance fees, moving to adopt a stance more consistent with that of the Tax Court in Highland Farms. TAM 9307007 (Oct. 28, 1992), for example, was issued in the same year as TAM 9246006, but approaches the tax consequences of CCRC entrance fees in a manner more consistent with Highland Farms, and with a similar result. TAM 9307007 asked whether a purported loan portion of an entrance fee was a true loan or instead an advance payment for rent under Treas. Reg. § 1.61-8(b). The CCRC required a resident, as part of the consideration to obtain occupancy, to pay a "fixed resident fee" which entitled him or her to lifetime use of the residential unit and access to an adjacent health care center. The amount of the fee varied with the size of the unit. The fee consisted of two portions: an initial non-refundable residence and care fee that constituted 10 percent of the fixed resident fee, and the balance of the fee, which was cast as a loan. The CCRC included the 10 percent initial non-refundable piece in gross income in the year of receipt. A resident also paid a monthly service fee for utilities, limited medical services, one meal per day, maid service, interior and exterior maintenance of the premises, and emergency and security services. The CCRC could increase the amount of the monthly fee.

The portion cast as a loan was evidenced by a non-interest-bearing promissory note that incorporated the terms of the residency agreement. Under the residency agreement, the principal amount of the note was reduced each year for the first three years by a sum equal to the initial residence and care fee. Under these terms, the balance of the note could be reduced to 60 percent of its original amount, but not below that amount. The principal amount of the note became due to the resident upon one of the following events:

- The resident died or decided for any reason not to accept the unit prior to taking possession of it.

- The resident died or left after having taken possession of the unit.

- The CCRC was obligated to repay the loan either 120 days after the foregoing events or on the date a replacement occupant was secured for a vacated unit, whichever occurred first.

The IRS concluded that the non-refundable initial residence and care fee, which was 10 percent of the fixed resident fee, was an advance rental and that the CCRC had properly included it in gross income in the year of receipt. The IRS then broke the remaining portion of the fixed resident fee into two components—the additional residence and care fee, which reduced the principal amount of the note by 10 percent each year for three years, and the remaining fee. Looking at all the facts and circumstances, particularly whether there was an intent to make a loan and repayment was contemplated by the parties, the IRS concluded that "the parties to the loan clearly intend that the entire two-thirds portion [the fully refundable fee] is to be paid back when the loan becomes due and payable." Accordingly, this portion was a loan to the CCRC. With respect to the additional residence and care fee, which could become nonrefundable over the first three years, the IRS held that the entire 30 percent portion had to be included in gross income in the initial year that the entire fixed entrance fee was paid, because the fact that some portion might be refunded was a contingency that did not prevent immediate accrual.51

Similarly, in TAM 9842001 (Oct. 16, 1998), the IRS ruled that refundable entrance fees were "not in substance sales" and were "properly characterized as a loan." Residents were required to pay entrance fees upon admission to the CCRC, which could then use the fees at its discretion. The entrance fee was evidenced by an "Entrance Deposit Certificate" and was 90 percent refundable (without interest) after the agreement was terminated. The refund was payable on the earlier of one year after the unit was vacated or the date on which CCRC had received an entrance fee from a new resident of the unit. A resident could terminate the agreement for any reason; the agreement would also terminate on the resident's death or the CCRC's termination for a number of reasons, all essentially reflecting good cause. Legal title was not transferred to the resident, and all property taxes, insurance and utilities were paid by the CCRC.

Citing Highland Farms, the IRS first ruled that the entrance fees were not proceeds from a taxable sale or exchange. Instead, the facts supported the characterization of the transaction as a loan—legal title did not pass, a deed was not delivered, the CCRC continued to pay taxes and bore the risk of loss, the CCRC received the profits from the sale of property and the benefit of appreciation and risk of a decline in value, the residents could not assign or transfer occupancy rights, and the residents did not acquire an equity interest in the property. Conversely, although no interest was paid, the deposit certificate promised to pay the resident at least 90 percent of the entrance fee, and such obligation was unconditional. Moreover, the refundable portion was secured by the CCRC's property, although this was subordinate to other indebtedness.

The IRS next ruled that the entrance fees were not includable in gross income. The IRS stated that "in this case the requirement that [the CCRC] refund the fees precludes including the fees in income." The fact that the obligation was unconditional distinguished the ruling from situations where "the refund requirement is not absolute."

Recently, the IRS seemingly backed away from the Tax Court's decision in Highland Farms and its own subsequent administrative practice when it asserted in three separate instances that CCRCs were required to include the refundable portion of entrance fees paid by residents in income in the year of receipt. Remarkably, the IRS even asserted a 20 percent penalty, claiming that the CCRCs in question did not have a reasonable basis for excluding the refundable portion of the entrance fees from income. After the CCRCs filed their petitions with the Tax Court, the IRS admitted that it had erred in increasing the CCRCs' taxable incomes and asserting penalties. Notably, however, the IRS did not specifically concede that its underlying legal position—that entrance fees are properly characterized as advance rental income and therefore taxable upon receipt—was wrong.52

2 Guidance Regarding Analogous One-Time Membership Fees

The treatment of one-time, refundable membership fees made to private "club" entities supports the "loan" treatment of CCRC entrance fees and their exclusion from gross income. In this analogous context, the IRS has consistently ruled that one-time, refundable membership fees are properly characterized as loans and are excludable from gross income in the year of receipt.

More than 50 years ago, the IRS addressed whether admission fees paid to a members-only recreational club were includable in gross income in the year of receipt.53 A private swimming club charged each admitted member a one-time membership fee. The fees were used to fund construction of a new swimming pool and club facilities. Under the membership contract, members were entitled to a full refund of the membership fee within the earlier of (1) six months after the date of contract, if club membership did not reach a designated level within that time, or (2) five years after the date on which the new pool facilities first became operative. The contract also obligated members to pay annual dues. If a member became and remained delinquent in dues payments for 30 days, the club was entitled to deduct any delinquent amount from his or her membership fee.

The IRS ruled that the membership fee was not gross income. Under the terms of the contract, the membership fee was "in the nature of a loan to the extent that the [club] ha[d] a continuing obligation to refund [it]." If this continuing obligation ceased with respect to any portion of the membership fee—e.g., if any portion of the fee was later used to cure delinquency in the member's annual dues—that amount would constitute gross income to the club in the year of reduction.54

Similarly, the IRS in a 1997 TAM55 addressed whether a country club properly excluded membership deposits from its gross income. The country club required applicants to pay a membership deposit through installments corresponding to construction of club facilities, with the final installment due upon completion of the clubhouse. The club had discretion to use deposit proceeds "for any purpose." Deposits were paid in installments but fully and unconditionally refundable once paid in full.56 The membership contract obligated the club to refund the deposit upon the earlier of (1) 30 years from the date of acceptance for membership and full payment of the membership deposit, (2) 30 days after the member's resignation and the club's repurchase of the membership, or (3) 30 days after the club's termination of the member's membership. Before refunding a membership deposit for any reason, the club was entitled to deduct amounts still owed by the member to the club, if any. The club treated the membership deposits as liabilities and excluded them from gross income.

Relying on IRC § 61, case law,57 and Rev. Rul. 58-17, the IRS ruled that the membership deposit was a nontaxable loan to the extent that the club was absolutely and unconditionally obligated to refund it. Accordingly, membership deposits were not includable in gross income in their year of receipt. Only amounts by which the deposit was reduced in order to cure an account delinquency, if any, would constitute gross income, and then in the year of reduction.

In a 1966 Rev. Rul., the IRS held that a private club's one-time membership fees must be included as gross income in the year of receipt when only subject to a contingent obligation of repayment.58 A private swimming club charged its members a one-time membership fee as well as monthly dues. If moving out of the locality within five years of joining the club, members were entitled to a partial refund of the membership fee in a declining amount based on the length of membership. After five years, members were not entitled to a refund of their membership fee under any circumstances. The club was unrestricted in its use of the membership funds, once received.

Distinguishing these circumstances from those in Rev. Rul. 58-17, the IRS concluded that here the membership fees were not "in the nature of a loan." The club earned membership fees when it admitted members to the club; it had only a limited and contingent obligation to refund the membership fee, and its liability to do so was not fixed. Accordingly, the membership fee constituted gross income in the taxable year received or accrued. In the event the club later refunded any amount of a membership fee, it would be entitled to a deduction in that amount in the year of repayment or accrued liability for repayment.

These rulings parallel the IRS's published position in Rev. Rul. 73-549 and its administrative practice in PLR 7307139830A, TAM 9307007 and TAM 9842001. Taken together, the authorities support two general propositions, both consistent with the summary conclusions drawn above. Where a private entity requires members to pay a one-time, advance admission that is unconditionally refundable in full or large part, the refundable portion of the fee will not constitute gross income in the year it is received. In contrast, where a private entity requires members to pay a one-time, advance admission that is nonrefundable or refundable only subject to limited contingencies, the fee may constitute gross income for the taxable year in which it is received or accrued.

B. Entrance Fees as Replacement Proceeds

Another question regarding the tax treatment of entrance fees arises in connection with the tax-exempt status of certain CCRCs,59 which often rely on tax-exempt bond proceeds to finance construction, remodeling and expansion of their facilities. Under IRC § 103(a), gross income does not include interest on any state or local bond, except as provided in IRC § 103(b). Section 103(b)(2) provides that gross income does include interest on "arbitrage bonds" as defined in IRC § 148. Citing the tax-exempt status of the CCRC at issue, the IRS recently questioned whether entrance fees used as part of a facility's collateral pledge to secure new or outstanding bonds represented "replacement proceeds" for the bonds, thereby causing them to be "arbitrage bonds" under IRC § 148. If correct, this finding would cause the bonds to lose their tax-exempt status, thereby requiring holders of the bonds to include any interest earned on the bonds in income.60

Section 148 accords arbitrage treatment to any bond issued as part of a tax-exempt issue if any portion of the issue's proceeds is reasonably expected to be used to acquire higher-yielding investments. A higher-yielding investment is any investment property that, over the term of the issue, produces a "materially higher" yield than that of the issue.61 A bond will also be treated as an arbitrage bond if any amount of the issue's proceeds is used as "replacement proceeds." Replacement proceeds are amounts substituted for other funds that were used to acquire higher yielding investments. Treas. Reg. § 1.148-1(c) provides that generally, amounts are replacement proceeds if the amounts have a "sufficiently direct nexus to the issue or to the governmental purpose of the issue to conclude that the amounts would have been used for that governmental purpose if the proceeds of the issue were not [so used]." The IRS has ruled that a pledge of collateral may constitute replacement proceeds if there is "reasonable assurance" that the collateral will be available if needed to pay debt service on the bonds.62

In TAM 201118012 (Feb. 8, 2011), the IRS addressed whether entrance fees constitute replacement proceeds under IRC § 148 when collected by a CCRC and then pledged as part of its general revenue as collateral to secure a loan of tax-exempt bond proceeds. The CCRC used the bond proceeds to expand its facilities and to refund a prior series of tax-exempt bonds, the proceeds of which had been used to build the facility. The CCRC secured the loan by granting the issuer a first priority security interest in its general revenue, including entrance fees received from incoming residents. One source of the CCRC's general revenue was a mandatory entrance fee charged to residents prior to their occupation; thus, pledging the CCRC's general revenue as collateral gave the third-party issuer an indirect security interest in the entrance fees as one facet of that total revenue. The collateral agreement did not restrict the CCRC's ability to commingle the entrance fees with the balance of its general revenue, and it was the CCRC's practice to do so. The CCRC also maintained actual possession and unrestricted use of the entrance fees absent issuer action to perfect the security interest. The CCRC was not required to hold entrance fees in trust for the residents, and the CCRC's residence contract permitted the CCRC to use entrance fees for its own purposes, including investment. Accordingly, over the course of business and under both the collateral agreements and its resident contracts, the CCRC routinely used entrance fees and other cash revenue to cover operating costs, deficits and various capital needs.

The IRS found that, under these circumstances, the entrance fees were not replacement proceeds. The ruling acknowledged that the CCRC's pledge of its general revenue as collateral for the bonds created a nexus between the entrance fees and the bond issue. However, the IRS concluded that under the facts of this case, the collateral pledge of the CCRC's general revenue did not constitute "reasonable assurance" that the entrance fees would be available to pay debt service on the bonds. The CCRC commingled revenue from all sources in its general accounts; no provisions in the indenture or financing documents required the entrance fees to be held in reserve for debt service; and the CCRC's residence agreement did not restrict it from spending the entrance fees. Further, it could be inferred from the facts and timing of the case that the CCRC had actually spent a substantial portion of its entrance fee revenue after issuance of the bonds without objection by any party involved. There was also no showing that the issuer had reasonably relied on any expectation that the CCRC would maintain a particular level of revenue, from entrance fees or other sources, while the bonds were outstanding. These facts outweighed the technical nexus between the CCRC's entrance fees (and other revenues) and the bonds. Consequently, the entrance fees were "not properly characterized as replacement proceeds" under the facts of the TAM.

The ruling resulted from a much-publicized audit of Mission Ridge, a tax-exempt CCRC in Montana. An adverse ruling in that case could have threatened the viability of all CCRCs financed with tax-exempt bonds. While CCRCs with similar financing structures may be breathing easier, other audits are ongoing on this issue, and it is possible that the IRS may reach a different result if presented with different facts.63

C. Depreciation Deductions for CCRC Facilities

Another potential issue for CCRCs is the recovery period for depreciating facilities. In ILM 201147025 (Aug. 4, 2011),64 the IRS advised that CCRC facilities are residential rental property, subject to a 27.5-year recovery period, and not nonresidential real property, which is subject to a 39-year recovery period. The IRS internal memorandum involved a CCRC that provided two types of accommodations at various communities it owned. Type One communities operated under the typical entrance and monthly fee model. Type Two communities involved renewal annual leases with no upfront entrance fees, with additional charges for any onsite assisted living, personal care or Alzheimer's disease care. In reporting income for both types of communities, the CCRC described the monthly fees as life care services income and not as rent. For tax purposes, the CCRC treated both types of communities as residential rental property with a recovery period of 27.5 years for purposes of IRC § 168(a).

Under IRC § 168, residential real property is generally defined as any building if 80 percent or more of the gross rental income from such building is from "dwelling units." The numerator is the portion of the fees allocable to residential rent, and the denominator is the total rent received (both residential and non-residential rents).

The IRS concluded that the various types of residential units (independent living, assisted living, Alzheimer's and memory support care, and skilled nursing care units) were used to provide living accommodations and therefore were "dwelling units." Because the right to occupy such a unit was provided under the residency agreement, some allocable portion of the monthly fee was for the use of, or the right to use, a dwelling unit, and constituted rental income for purposes of the 80 percent test. The IRS found that the taxpayer's subjective characterization of the monthly fees as not rent was not dispositive. Thus, because nothing in the facts provided indicated that the CCRC received non-residential rental income from third parties, or that the CCRC conducted commercial activities in a significant enough portion to cause failure of the 80 percent test, the buildings utilized to provide the living accommodations qualified as residential rental property. Accordingly, the taxpayer was permitted to depreciate the buildings under the shorter recovery period.

IV. Conclusion

CCRCs provide valuable lifestyle and medical options for the elderly in a tax-efficient manner. For residents, portions of entrance and membership fees paid to these facilities may be deductible under IRC § 213 to the extent they are attributable to medical expenses. As business entities, CCRCs may gain temporary increases in liquidity through receipt of entrance and membership fees, which the CCRC may be obligated to refund in whole or part at a future date. Under precedent discussed above, the CCRC may not have to recognize amounts of any refundable portion of charged fees as gross income in the year of receipt, depending on how the entrance fee is structured.

It remains to be seen if the IRS will continue to closely scrutinize, both at the resident and CCRC level, the deduction and income issues described above. But, in light of the recent developments discussed in this article, both residents and CCRCs would be well advised to review their current tax reporting positions to protect against any future examination by the IRS.

Footnotes

1 Four types of contracts are commonly used in the industry: (1) Type A, or extensive or Life Care contracts; (2) Type B, or modified contracts; (3) Type C, or fee-for-service contracts; and (4) Type D, or rental agreements. See "Continuing Care Retirement Communities Can Provide Benefits, but Not Without Some Risk," General Accounting Office Report, GAO-10-611 (June 2010).

2 It is said in some circles that, if you have seen one CCRC, you have seen one CCRC.

3 A discussion of state regulatory issues is beyond the scope of this article. For more information, see GAO-10-611.

4 This deduction applies only to individual taxpayers who elect to itemize their deductions rather than take the standard deduction. Medical expenses must exceed 10 percent of adjusted gross income to be deductible in tax years beginning after December 31, 2012. Patient Protection and Affordable Care Act, P.L. 111-148, § 9013(a).

IRC § 213(d)(1)(A)-(D); Treas. Reg. § 1.213-1(e)(1); IRS Publication 502.

5 IRC § 213(d)(1)(A)-(D); Treas. Reg. § 1.213-1(e)(1); IRS Publication 502.

6 General Counsel Memoranda (GCMs) and Technical Advice Memoranda (TAMs) are internal memoranda from the IRS's Chief Counsel's Office providing technical guidance to IRS personnel. Private Letter Rulings (PLRs) are rulings addressed to individual taxpayers relating to proposed transactions; they are generally based upon facts submitted by the taxpayers. Although these rulings are not precedential (IRC § 6110(k)(3)), courts often consider them as indications of the IRS's position on an issue. See, e.g., Baker v. Commissioner, 122 T.C. 143, 167 n.25 (2004) (collecting cases).

7 GCM 33259 (June 10, 1966).

8 The IRS publishes Revenue Rulings (Rev. Ruls.), which "represent the conclusions of the Service on the application of the law to the pivotal facts stated in the revenue ruling." See Treas. Reg. § 601.201(a)(6). IRS personnel and taxpayers "are cautioned against reaching the same conclusions in other cases unless the facts and circumstances are substantially the same." See, e.g., 2011-39 I.R.B. (introductory language).

9 Rev. Rul. 67-185, 1967-1 C.B. 70. In 1968, the IRS again stated this principle in Rev. Rul. 68-525, 1968-2 C.B. 112, but denied a deduction for the portion of an entrance fee used solely to build an infirmary, finding it was not a qualifying medical expense under IRC § 213. However, the ruling did allow a partial deduction under IRC § 213 for the portion of the taxpayers' monthly fees attributable to lifetime care.

10 See Rev. Rul. 54-457, 1954-2 C.B. 100.

11 Rev. Rul. 75-302, 1975-2 C.B. 86.

12 In Rev. Rul. 75-303, 1975-2 C.B. 87, the IRS addressed a similar issue, this time in the context of nonrefundable payments made to a private institution for lifetime care of a handicapped person. Under the contract, the taxpayers made a lump-sum payment upon signing the contract, monthly payments over a period of years, and a final payment upon entry into the institution. The IRS ruled that the payments were deductible under IRC § 213 because they were made in order to secure medical services, despite the fact that such services were not to be performed until a future time, if at all. See also PLR 8410057 (Dec. 6, 1983) (refundable payments to institution for the mentally handicapped partially deductible as medical expense).

13 Rev. Rul. 76-481, 1976-2 C.B. 82.

14 See, e.g., PLR 8930024 (July 28, 1989); PLR 8930023 (July 28, 1989); PLR 8748026 (Aug. 31, 1987); PLR 8651028 (Sept. 19, 1986); PLR 8630005 (Apr. 4, 1986); PLR 8641037 (July 11, 1986); PLR 8213102 (Dec. 30, 1981); PLR 7807093 (Nov. 21, 1977); PLR 7608300510A (Aug. 30, 1976).

15 Est. of Smith v. Commissioner, 79 T.C. 313 (1982).

16 1984-2 C.B. 1 ("Acquiescence in a decision means acceptance by the Service of the conclusion reached, and does not necessarily mean acceptance and approval of any or all of the reasons assigned by the court for its conclusions.")

17 Finzer v. United States, 496 F.Supp.2d 954 (N.D. Ill. 2007)., 496 F.Supp.2d 954 (N.D. Ill. 2007).

18 Id. at 958.

19 The IRS, in its own rulings, has not made such a distinction. See, e.g., PLR 8221134 ("in the event a person terminates his or her residency a portion of their entrance fee is refunded") (emphasis added). Further, the district court's interpretation of the rulings appears inconsistent with the plain language of the rulings; in essence, it replaced the term "would" with "may," and concluded that there was no guarantee that any portion would be refunded.

20 Baker v. Commissioner, 122 T.C. 143 (2004).

21 Historically, the IRS and courts have shown deference to CCRCs' independent determinations of percentages of fees used to fulfill medical expense obligations. See, e.g., PLR 8009030 (Nov. 29, 1979) (addressing a CCRC's reporting medical costs equaling 45 percent of its total expenses); PLR 8011123 (Dec. 16, 1980) (addressing a CCRC's reporting medical costs equaling 48 percent of its total expenses).

22 For example, in PLR 7608300510A (Aug. 30, 1976), the IRS observed that a facility's prior experience "is a reasonable method to determine [medical expense fee allocation]."

23 See, e.g., PLR 8651028 (Sept. 19, 1986); PLR 8641037 (July 11, 1986); PLR 8630005 (Apr. 4, 1986); PLR 8213102 (Dec. 30, 1981); PLR 8213102 (Dec. 30, 1981).

24 See, e.g., PLR 8630005; PLR 8651028.

25 Because the Tax Court held that the IRS bore the burden of proof, it only addressed those cost items that the IRS challenged, treating any unaddressed items as concessions by the IRS without expressing any opinion as to the substantive validity or accuracy of those items.

26 Deficit Reduction Act of 1984, Pub. L. 98-369, § 172, 98 Stat. 494, 699-703.

27 For a gift or demand loan, foregone interest for any period is the amount by which the interest that would have been due on the loan, had interest been charged at the Applicable Federal Rate (AFR), exceeds the interest, if any, actually charged on the loan. IRC § 7872(a)(1). For a term loan, foregone interest is the amount by which the amount of the loan exceeds the present value of all payments on the loan, discounted to the issue date using the AFR. IRC § 7872(b)(1).

28 IRC § 7872(a)(1).

29 For example, on a below-market loan from a corporation to a shareholder, the deemed transfer to the shareholder is treated as a dividend. On a below-market loan from an employer to an employee, the deemed transfer to the employee is treated as compensation.

30 IRC § 7872(a)(2).

31 IRC § 7872(b)(1).

32 IRC § 7872(b)(2).

33 IRC § 7872(c)(1)(E).

34 Conf. Report, 1984-3 C.B. (Vol. 2) 272.

35 50 Fed. Reg. 33553-01, 1985-2 C.B. 812.

36 Prop. Treas. Reg. § 1.7872-2(a)(b)(1); see also 1985-2 C.B. at 813 (stating in the preamble to the proposed regulations that the term "loan" includes "a refundable deposit").

37 Simplification of Imputed Interest Rules, Pub. L. 99-121, § 201, 99 Stat. 511-14.

38 IRC § 7872(g)(2). This dollar limit was subject to adjustment to reflect inflation. IRC § 7872(g)(5). See Rev. Rul. 2005-75, 2005-2 C.B. 1073 (providing dollar amounts for from pre-1987 to 2006).

39 Tax Increase Prevention and Reconciliation Act of 2005, Pub. L. 109-222, § 209, 120 Stat. 345, 351-52 (effective for calendar years beginning after December 31, 2005, "with respect to loans made before, on, or after such date"). Congress also modified the definition of "qualified continuing care facility." See IRC § 7872(h)(3).

40 Tax Relief and Health Care Act of 2006, P.L. 109-432.

41 For GAAP purposes, guidance on the treatment of refundable entrance fees is set forth in Chapter 14 of the Audit and Accounting Guide for Health Care Organization. According to this guide, under GAAP the refundable portion is reported as a liability and, upon actual refund to the resident, is disclosed in the statement of cash flows as a financing transaction. In contrast, nonrefundable portions of entrance fees represent payments for future services and are accounted for as deferred revenue and amortized to income over future periods based on the estimated life of the resident or the contract term. For SEC registrants, the SEC has ruled that refundable portions of entrance fees should be reported as current liabilities, pursuant to FASB Statement No. 78.

42 Commissioner v. Glenshaw Glass, 348 U.S. 426 (1955).

43 See Commissioner v. Tufts, 461 U.S. 300, 307 (1983) ("When a taxpayer receives a loan, he incurs an obligation to repay that loan at some future date. Because of this obligation, the loan proceeds do not qualify as income to the taxpayer. When he fulfills the obligation, the repayment of the loan likewise has no effect on his tax liability."); see also Commissioner v. Indianapolis Power & Light Company, 493 U.S. 203, 207 (1990).

44 The characterization of entrance fees as advance payments of rent is at odds with a number of state court holdings regarding the nature of the relationship between a CCRC and its residents. See, e.g., Jackim v. CC-Lake, Inc., 363 Ill. App. 3d 759, 843 N.E. 2d 1113 (Ill. App. Ct., 1st Dist. 2005) (life care agreement is not a lease; life care provider and resident do not have a landlord-tenant relationship); Starns v. American Baptist Estates of Red Bank, 352 N.J. Super. 327, 800 A. 2d 182 (N.J. Super. Ct. 2002) (citing "notable differences" between a CCRC and an apartment building); Antler v. Classic Residence Mgt. Ltd. Part'p, 315 Ill. App. 3d 259, 733 N.E. 2d 393 (Ill. App. Ct., 1st Dist. 2000) (distinguishing operator-resident relationship from landlord-tenant); Freedom Village of Holland v. City of Holland, 1998 Mich. App. LEXIS 1372 (Mich. Ct. App. 1998) (entrance fee is not income from rental or lease of property unless and until it is actually used to pay unit rental fees); M&I First Nat'l Bank v. Episcopal Homes Mgt., Inc., 195 Wis. 2d 485, 536 N.W. 2d 175 (Wisc. Ct. App. 1995) (although residency agreement is a rental agreement, entrance fee is a security deposit); Guthmann v. La Vida Llena, 103 N.M. 506; 708 P. 2d 675 (Sup. Ct. N.M. 1985) (services and contracted obligations of operator are not comparable to those provided by landlords of apartments); American Nat'l Bank and Trust of N.J. v. Presbyterian Homes of N.J., 148 N.J. Super. 465; 372 A. 2d 1147 (N.J. Super. Ct. 1977) (residence agreement is not a lease).; but see Markham v. John Knox Village of Florida, Inc., 547 So. 2d 1044 (Fla. Dist. Ct. App. 1989) (residency agreement is "a form of long-term rental contract").

45 Rev. Rul. 73-549, 1973-2 C.B. 17.

46 TAM 9246006 (Nov. 13, 1992).

47 Highland Farms, Inc. v. Commissioner, 106 T.C. 237 (1996).

48 Commissioner v. Indianapolis Power & Light, 493 U.S. 203 (1990).

49 Oak Indus., Inc. v. Commissioner, 96 T.C. 559 (1991).

50 Highland Farms, 106 T.C. at 252 (emphasis added).

51 Presumably, the CCRC would be entitled to a deduction for any part of the 30 percent portion that was actually refunded to a resident who moved out or died before the passing of three years.

52 See Amy S. Elliott, "IRS Backs Down in Standoff on Retirement Community Fee Taxation," 2010 TNT 129-1 (July 7, 2010).

53 Rev. Rul. 58-17, 1958-1 C.B. 11.

54 See also PLR 7921039 (Feb. 23, 1979) (holding that where a private club had an unconditional obligation to refund members' one-time membership fees in full upon the earlier of 25 years or the club's option, the membership fees were excludable from the club's gross income to the extent they had not been used to offset delinquencies in members' annual dues).

55 TAM 9735002 (Aug. 29, 1997).

56 At the time, the clubhouse had not yet been completed and thus no deposits had been "fully paid." However, under the signed membership plan, both the club and its members had contractually agreed to be bound by the terms of repayment for membership deposits. At the time of the TAM, every member who had resigned from the club had received a full refund of his or her deposit, less any deductions for amounts owed to the club.

57 The TAM cited Indianapolis Power and Tufts for the proposition that "[a] taxpayer generally does not have an accession to wealth, nor complete dominion over an item, when the item is received subject to an obligation to repay, as with a refundable deposit or a loan."

58 Rev. Rul. 66-347, 1966-2 C.B. 196. This treatment is inconsistent with the Tax Court's treatment of the entrance fee in Highland Farms.

59 It is not uncommon for CCRCs to have tax-exempt status under IRC § 501(c)(3).

60 In a typical tax-exempt bond issue, this could trigger indemnities in the bond indentures.

61 For investments allocable to replacement proceeds, "materially higher" means one-thousandth of 1 percentage point (i.e., 0.001 percent) higher than the issue's yield. Treas. Reg. § 1.148-2(d)(2)(ii).

62 Rev. Rul. 73-348, 1978-2 C.B. 95.

63 See Stephen Maag, "Mission Ridge Prevails in IRS Audit," (Feb. 10, 2011) (available at http://www.leadingage.org/Article.aspx?id=1057 ); Sam Young, "Unreleased Bond Memorandum Shows Replacement Proceed Treatment Difficulty," 2011 TNT 44-3 (Mar. 7, 2011).

64 An "ILM" is a legal memorandum issued by the IRS Office of Chief Counsel. Like GCMs, TAMs and PLRs, ILMs are not precedential but can be considered evidence of the IRS's administrative position.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.