Overview

Failure to agree leads to delay

Solvency II

The text for the Solvency II Directive is largely known, with much of the detail likely to remain unchanged from drafts already in circulation. However, the Council of the European Union (representing national governments around the European Union), the European Commission and the European Parliament (the 'trialogue parties') have failed to agree on measures to address products with long term guarantees (a consensus is necessary for the Directive to go through). Subsequently, the European Parliament has amended the indicative date for the vote on the Directive, which will allow the trialogue parties more time to reach an agreement and will also make it virtually impossible for the Directive to go live on 1 January 2014 (due to the procedures required in the legislative process). At the time of publication, the exact delay is unclear however we understand that one to two years from 2014 is being considered.

The most contentious issue is how to deal with volatility in credit spreads in the valuation of products with long term guarantees. An impact assessment by the European Insurance and Occupational Pensions Authority (EIOPA) on the current proposals is expected this year. Due to uncertainties about what the results will show and how policymakers will react, it may be mid-2013 before the results are finalised and the implications can be assessed.

IFRS

The International Accounting Standards Board (IASB) is planning to publish a second exposure draft ('re-exposure') setting out its final proposals for IFRS Phase II in the first half of 2013. Since the first exposure draft in 2010, the IASB has made significant revisions to address the perceived 'artificial' earnings volatility in the original model. It has also attempted to achieve convergence with the US accounting standard setter, but this is now unlikely due to the divergence in views.

The re-exposure represents what may be the final opportunity for the industry to influence the new accounting standard and it is expected to be limited to five key areas:

- Treatment of unearned profit in contracts ('unlocking' the residual margin)

- Treatment of participating contracts

- Presentation of premiums in the income statement

- Presentation of the effect of changes in the discount rate in other comprehensive income

- Transition by retrospective application

Insurers also face changes to the classification and measurement requirements for financial instruments (the IASB is developing IFRS 9 which will replace the current IAS 39). IFRS 9 is expected to be effective from 1 January 2015, subject to a further exposure draft and subsequent endorsement for use in the European Union. This means there will now be a staggered adoption of this standard and the new insurance contracts standard.

Figure 1sets out the current known timeline for both Solvency II and IFRS.

Making the most of the breathing space

Solvency II

Whilst the expected delay in Solvency II creates further uncertainty over the final timeframe, the bulk of the framework is established creating an opportunity to focus on embedding Solvency II programmes into 'business as usual'.

Sustaining the momentum of Solvency II preparations will allow your business to prepare in good time and embed the framework, avoiding undue inefficiency and disruption. You would also benefit earlier from the payback on any planned restructuring, strategic realignment and investment in new information systems ahead of slower moving competitors. Some contingency planning for the remaining issues will be necessary, including gauging the impact of different outcomes from the long-term guarantees assessment. But the system requirements, organisational considerations and other 'heavy lifting' won't change. Giving greater focus to the practical challenges arising from the public and private disclosure requirements may also be beneficial as currently this is a common area of under investment in Solvency II preparations.

IFRS Phase II

Given the delay, it will be important to use this time to fully understand recent developments and respond to the reexposure draft. You can then look to begin more significant implementation planning activities in the second half of 2013 when the final requirements will be clearer. This should include a detailed impact assessment to understand the financial and operational impacts of the revised requirements on your business.

An important consideration in your impact assessment will be how to deal with the different timelines in IFRS and Solvency II, as we explore later in this publication (in the 'Mind the gap' section). There is a real opportunity to 'future-proof' Solvency II actuarial and reporting models for IFRS. With the potential for early adoption of IFRS Phase II and the likely delay to Solvency II, the possibility of a coordinated one time transition to Solvency II and the new IFRS standards re-emerges.

Bringing it all together

The breathing space provides a valuable opportunity to put the foundations in place for a finance function which is capable of meeting these new demands and providing the insights that will give your business an edge in the new commercial landscape.

Key priorities include closer collaboration between the risk, actuarial and finance functions and making sure that the underlying risk and capital models being developed for Solvency II are flexible enough to be adapted for IFRS Phase II, given the similarities.

However, there will be some significant differences in the detailed requirements between the Solvency II and IFRS Phase II frameworks. Your business will thus need to reconcile, or at least explain, these variations. Otherwise you may face awkward questions from analysts and investors.

You may also feel that Solvency II and the new IFRS basis will not fully explain the true performance and potential of your business, and the strategic rationale that underlies this. You should consider how to approach any supplementary reporting, such as embedded value (or equivalent) and cash generation disclosures, that may be needed in the new reporting world.

The box opposite sets out key questions for your organisation to consider in the coming months when planning for future IFRS Phase II implementation.

Outline of this Publication

This publication sets out the challenges in implementing the changes to IFRS, focusing on the proposed insurance contracts standard, in view of the significant Solvency II projects insurers are currently undertaking and considers the impact of the different expected implementation dates. It then examines the various technical challenges and key similarities and differences between IFRS and Solvency II in the areas of contract liabilities, disclosure and presentation, assets and other liabilities and group reporting. The appendices provide a more detailed point-by-point technical comparison.

The publication is based on our understanding of IFRS and Solvency II proposals as of October 2012, elements of which are in different phases of discussion and consultation. The final requirements of both IFRS and Solvency II may still evolve significantly up to their effective dates and, therefore, may differ from those set out in this publication. Given the recent challenges in finalising the requirements of the two regimes, it is also possible that the expected implementation timelines will change again in the future.

What you should be considering on IFRS

- Are concerns over 'artificial' earnings volatility being adequately addressed in the revised IFRS Phase II proposals?

- How much impact is the implementation of IFRS Phase II going to have on your organisation from a strategic and operational perspective?

- How can you make sure you secure the right resources for future implementation?

- Would there be any benefits from changing your current accounting approach before mandatory IFRS Phase II implementation?

- How can you take advantage of the parallels between Solvency II and IFRS Phase II and develop 'future-proof' actuarial and reporting models capable of dealing with both sets of demands?

- Should the impact of new IFRS on your financial results affect your current decision making?

Mind the gap!

The timelines for Solvency II and IFRS Phase II are not aligned and you will need to consider your options for reporting in this gap period. How can your business limit the cost and disruption of running separate systems? Which reporting options are feasible in the gap period and how will they be perceived and understood by investors?

There is a likelihood that the various new IFRS standards may come on stream at different times, resulting in multiple transitions and re-statements. Even with the expected delays, it still appears likely that Solvency II will be effective before IFRS Phase II.

The timing issues present a range of practical challenges and considerations, not least because the current IFRS reporting requirement for insurance contracts are often based on the current regulatory framework (Solvency I). If Solvency II does go live before IFRS Phase II, your business will have a number of potential options for IFRS reporting for insurance contracts in the interim ('gap') period. Effective stakeholder communication and explanation during this period of transition and uncertainty will be crucial.

A standard industry position may emerge over the coming years. Most insurers won't want multiple transitions between different approaches, not least to avoid the requirement for re-statements and potential artificial volatility in earnings. Other important considerations in assessing the options include the reported financial impact, actual cash cost (such as running two separate models), impact on distributable profit, ease of preparation, future proofing, 'first mover' risk and the future role and approach to supplementary reporting. The impact on your current tax position and future tax planning will also be important as in many countries tax regulations are based on accounting profit. Understanding investor preference for the basis of your reporting may help you to decide on your approach and to identify gaps where further effort will be required in your communication strategy.

The options to consider include:

(1) Maintain current approach

In this option, existing IFRS reporting would be maintained during the gap period. This would require the parallel running of current models and processes, in addition to those required by Solvency II, which is likely to be a drain on costs and resources. While the approach provides stability and consistency in reporting as Solvency II is introduced, many of the current communication challenges faced by insurers will remain. Some of these challenges could be addressed by enhancing external disclosure on matters such as the drivers of IFRS operating earnings and the change in free capital over the reporting period. The wider the gap between the effective date of Solvency II and IFRS Phase II, the more important the decision to continue to incur the costs of running two models will become.

"With the potential for early adoption of IFRS Phase II and the likely delay to Solvency II, the opportunity for a coordinated 'big-bang' exercise has re emerged."

(2) Adopt Solvency II (or a modified version)

Existing IFRS 4 permits changes to the accounting policies in respect of the measurement of contract liabilities if they meet certain criteria for improving 'relevance and reliability'. An option for IFRS reporting during the gap period may be to adopt Solvency II or a modified version as the basis of financial reporting for insurance contracts, subject to meeting the requirements of existing IFRS 4. Potential challenges in adopting this option would include:

- How does the approach compare to the expected IFRS Phase II model? IFRS Phase II will give context for judgements about whether the 'relevance and reliability' criteria of IFRS 4 are met.

- Does the approach introduce additional prudence? IFRS 4 prohibits changes in accounting policies which introduce additional prudence in the measurement of insurance contracts where there is already sufficient prudence.

- Does the approach introduce nonuniform accounting policies across insurance groups? IFRS 4 prohibits increasing the diversity in accounting policies across insurance groups.

Adopting a pure Solvency II approach to measure the contract liability would allow the recognition of a profit at inception of a contract and this is also permitted in some current GAAPs. However, in IFRS Phase II such a profit is spread over the period of coverage by the inclusion of a 'residual margin' within the liability. In this option, as a modification to Solvency II, an insurer may seek to include a residual margin depending on its circumstances. Practices for the calculation and amortisation of the residual margin would then be required.

Specific considerations will also be required for non-life insurers as the option to adopt the simplified model for short duration contracts in IFRS Phase II is not an option in Solvency II.

The option to adopt Solvency II (or a modified version) may remove the requirement to maintain two different models, though a further change would then be required to adopt IFRS Phase II. As a result, two sets of re statements (with comparatives) would be required. This approach is likely to be confusing to analysts and investors if not handled carefully.

(3) Early adoption of the requirements of IFRS Phase II

In this option, the requirements of IFRS Phase II would be adopted in advance of the mandatory date. Either through early implementation of the standard itself (as expected to be permitted in IFRS, but subject to its endorsement in Europe) or by taking on board some of its key requirements as a way of improving existing accounting policies under IFRS 4.

Early adoption may be attractive as part of a co-ordinated 'big bang' exercise that brings together Solvency II and the transition to IFRS Phase II, IFRS 9 and other new IFRS standards. A big bang would limit the number of re-statements. It would also provide an opportunity to develop a single communication strategy and to resolve any legacy issues in one go. However, the complexities of a combined transition could introduce greater delivery risk to both Solvency II and IFRS projects. As with any early adoption, there are advantages and risks to being the 'first mover' including the risk of subsequent revisions to the accounting requirements.

There are clear advantages and disadvantages to each of these options. Time spent assessing the options now, to identify the best approach for your organisation, will not be wasted as the likely future path will become clearer over time.

Gearing up for an efficient transition

The move to IFRS Phase II presents significant implementation and investor relations challenges. How can your business ensure an efficient transition?

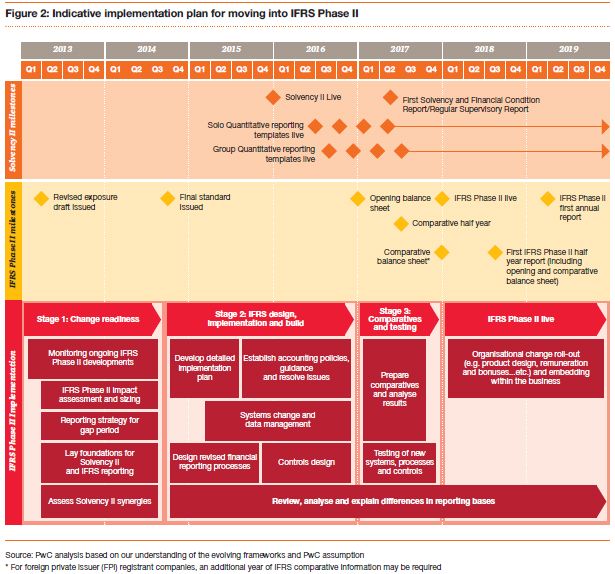

Figure 2 sets out an indicative plan for the implementation and phasing-in of IFRS Phase II. This is under the working assumptions that IFRS Phase II is mandatory from 1 January 2018, Solvency II is effective from 1 January 2016 and that during the 'gap' period the existing approach to IFRS reporting for insurance contracts is maintained. In planning to implement IFRS Phase II initial considerations include:

- Size of project: Investigate the potential size of the project at an early stage (especially if your business currently reports under a mixture of GAAPs) so that budget requirements can be estimated in advance and sufficient time can be built in to secure resources.

- Leveraging Solvency II: It is likely that the starting point for implementing IFRS Phase II will be the Solvency II models which insurers have recently developed. Understanding the differences between the two frameworks and whether your Solvency II models are flexible enough to be adapted for IFRS Phase II will be important.

- Priority areas: It will be important at an early stage to scope the most critical areas of the project. This includes the practical complexities such as full retrospective transition, so that your approach can be tailored to allow sufficient focus on these areas.

- Scenario planning: Investigate the different scenarios that could apply and understand the practical impact of each scenario as changes may be expected following the IASB reexposure and as industry practice develops.

- Disclosure and communication: Don't underestimate the time neededto prepare and industrialise disclosurerequirements and the importance ofexternal communication. Experiencefrom IFRS conversions in 2005demonstrates the importance of earlystakeholder management. Theimplementation of IFRS Phase II andSolvency II will lead to fundamentalchanges in how insurers evaluate andcommunicate performance, risk andcapital both internally and externally.Investors will also value insurers andassess financial and capital flexibilitydifferently. These changes represent aone-time opportunity for a 'root andbranch' reform of reporting to addressa number of the externalcommunication challenges theindustry has faced in recent years.The challenges for insurers will includebridging between the new and oldmetrics in a coherent manner. All thevalue gained from implementationcould be lost during this phase.

Overcoming the technical challenges

Both Solvency II and IFRS Phase II include significant departures from current reporting. A number of issues are also yet to be resolved. Further challenges come from the differences in approach between the two frameworks. How can you assess the potential synergies and the practical challenges that IFRS Phase II will bring?

Overview

As a prudential regulatory regime, the focus of Solvency II reporting is on the financial strength (capital resources) of the insurer as opposed to its performance during the year. As such, the Solvency II balance sheet is intended to reflect an economic valuation of all assets and liabilities at the balance sheet date. As a financial reporting regime, IFRS is focused not only on reporting financial position at the balance sheet date but also on reporting performance in the period. This gives rise to some of the differences between reporting under Solvency II and IFRS; in particular:

- Under IFRS Phase II the recognition of the profit arising from an insurance contract is spread over the period of coverage – this is achieved by the inclusion of a 'residual margin' liability which is not present under Solvency II. The valuation of insurance contract liabilities under IFRS Phase II and Solvency II is discussed in the 'Contract Liabilities' section with Appendix A providing a comparison by component.

- Solvency II applies a consistent valuation approach to all contracts issued by insurers. Under IFRS 'investment contracts' issued by insurers which do not transfer significant insurance risk (and that do not contain a discretionary participation feature) are accounted for as financial instruments, not insurance contracts (see Appendix B).

- The focus on reporting of performance under IFRS leads to changes in the value of insurance liabilities (and certain financial assets) resulting from changes in interest rates not being reported within profit or loss (as discussed in the 'Contract Liabilities' section).

- IFRS contains specific requirements regarding the reporting of volume measures in the income statement and there will be differences between the disclosures required under Solvency II and IFRS (as discussed in the 'External Reporting: Presentation and Disclosure' section).

- Under Solvency II all assets and other liabilities will be reported at economic (fair) value. Where the IFRS valuation is also based on fair value the valuation bases will be aligned. However, in some areas Solvency II introduces different valuation bases where IFRS is not viewed as representing an economic valuation (as discussed in the 'Assets and Other Liabilities' section, with Appendix C providing a comparison by component).

- In both Solvency II and IFRS, reporting is required at the level of the group as well as at the level of the individual insurer. However, there are differences in the scope and approach to group reporting (as discussed in the 'Group Reporting' section, with Appendix D providing a comparison by component).

A key aspect of the Solvency II regime is the requirement for an insurer to have sufficient financial strength to absorb future adverse developments. This is achieved through the requirement for insurers to hold a solvency capital requirement (SCR). There is no equivalent concept to the SCR within IFRS, and this paper does not consider Solvency II's requirements around calculating and reporting the SCR.

Contract liabilities

Measurement model

Both Solvency II and IFRS Phase II base the measurement of insurance contract liabilities on the concepts of a probability weighted estimate of future cash flows, the time value of money and an additional allowance for risk. In IFRS Phase II, an additional contract liability known as the residual margin is included to eliminate a gain on day one (while all day-one losses are recognised as incurred). There is no equivalent concept to the residual margin in Solvency II or in many current GAAPs. For short duration insurance contracts, which make up the majority of non-life contracts, a simplified unearned premium approach is permitted but not required under certain circumstances for pre-claims contract liabilities in IFRS. There is no equivalent concept in Solvency II.

In addition, there is a requirement to unbundle certain components of contracts and measure them under different IFRS standards, though these situations in practice are expected to be limited.

In IFRS, the measurement of contracts depends on their classification as either insurance or investment, while Solvency II makes no such distinction. The IFRS classification depends on the level of insurance risk transferred to the insurer and this definition is expected to be largely unchanged from IFRS 4. In addition, investment contracts with a discretionary participating feature (participating investment contracts), where issued by an insurer, are expected to be in the scope of the new insurance contracts standard.

Non-participating investment contracts, for example, a pure unit-linked savings contract, are similar in nature to instruments found in other markets and sectors and, as a result, are subject to the IFRS financial instruments and revenue standards. The contract liability is typically measured at fair value or at amortised cost.

Figure 3 illustrates a comparison of the Solvency II and IFRS requirements for measuring contract liabilities.

Figure 4 presents a summary of the main differences between IFRS Phase II and Solvency II contract liabilities based on our understanding of the evolving frameworks.

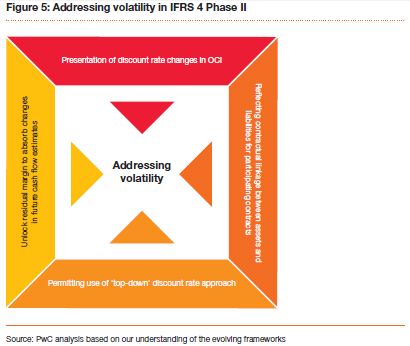

Addressing volatility

Since the original IASB exposure draft in 2010, significant revisions have been made to the IFRS Phase II measurement model. A number of these changes go some way to address the concern of stakeholders on what is perceived to be the 'artificial' earnings volatility in the original model (see Figure 5). The changes include:

- Requiring the residual margin to absorb certain changes in estimates of future cash flows.

- Clarifying that a 'top-down' approach can be adopted to determine the discount rate.

- Requiring that the effect of changes in the discount rate be presented in Other Comprehensive Income (OCI) to address the interaction with the presentation and measurement of assets (when at fair value through OCI or amortised cost).

- Reflecting the contractual links between assets and liabilities in the measurement of participating contracts.

The benefits of these refinements are accompanied by increased operational complexities that are not mirrored in Solvency II due to its focus on balance sheet strength. It is also unclear whether the proposed changes will fully address all stakeholders' concerns.

The following subsections of this publication explore in more detail the main difference between IFRS Phase II and Solvency II contract liabilities and the proposals to address the perceived 'artificial' earnings volatility in IFRS.

"The use of estimated future cash flows is the foundation of both frameworks. However, there are some potential differences which will present practical difficulties."

Cash flows

The use of estimated future cash flows is the foundation for the measurement model for Solvency II and IFRS Phase II. However, there are some differences which may present practical difficulties, necessitating either separate models or greater flexibility within a single model. We highlight three specific areas:

Scope of cash flows

In both Solvency II and IFRS Phase II, there is expected to be explicit guidance as to which cash flows are to be included in the measurement of the liabilities. Many of the cash flows will be the same in the two models, such as premiums and claims. However, not all the cash flows are expected to be fully aligned. For example, the inclusion of certain overheads costs may be different. This may trigger changes in your expense allocation process and lead to two sets of expense assumptions.

Acquisition costs

In IFRS Phase II, the cash flow model includes directly attributable acquisition expenses and so there is 'implicit' deferral of these expenses through a reduction in the residual margin. Many current GAAPs permit an explicit deferral of acquisition costs as an asset on the balance sheet, so while the exact definition of acquisition costs permitted to be deferred may be different you may well have the systems already in place to capture this data. For non-participating investment contracts in IFRS, there is explicit deferral of acquisition costs as an asset on the balance sheet, but with a narrower definition of the costs permitted to be deferred compared to insurance contracts (broadly costs that are incremental at the contract rather than portfolio level). There is no equivalent concept of deferring revenue or costs over the life of the contract in Solvency II.

Boundary of a contract

The boundary of a contract represents the point beyond which any cash flows relating to a contract are no longer recognised in the measurement of the liability. The boundary will be the same in the two frameworks for many contracts however there is a risk that some differences may exist. For example, there is a requirement in Solvency II to separate contracts into components, where the contract boundary differs between components. There is no equivalent requirement in IFRS.

In Solvency II, there is a separate contract boundary for those contracts which would typically be non participating investment contracts in IFRS. The boundary is defined so that no future premiums are included in the cash flows, and as a consequence, embedded profits arising from these future premiums are not included on the balance sheet. In IFRS, as these contracts are often unit linked, there is no estimation of future cash flows and the liability is measured at fair value or amortised cost which is usually the unit balance.

Insurers will require data and cash flow model developments to deal with these implications.

Discount rate

For insurers writing long-term savings products, the valuation of contract liabilities and resulting solvency ratios and accounting profit are highly sensitive to the selection of the discount rate.

There remains considerable uncertainty over the discount rate in Solvency II pending the proposed long-term guarantees impact assessment. It is expected that the discount rate to be used will be determined by the regulator based on the swap curve plus either a matching adjustment (applicable to certain contracts) or a counter-cyclical premium (only applicable in certain extreme market conditions). These adjustments to the swap curve are designed to address the impact of volatility in credit spreads on the solvency balance sheet. The matching adjustment is designed to reflect the possibility that there may be no (or limited) exposure to spread risk (excluding default risk) due to the characteristics of the liabilities and the asset-liability matching strategies adopted. The scope of liabilities to which the matching adjustment is applied (narrow versus wider) and the calibration of the adjustment remain uncertain. The counter-cyclical premium is designed, when triggered (by the regulator), to provide short-term relief during periods of 'excess' spread widening in sovereign and corporate bond markets. The calibration of the premium and the criteria as to when the premium is permitted remain uncertain.

In IFRS Phase II, the approach to the discount rate is principle-based and it must reflect the characteristics of the liabilities. You can use a 'top-down' approach, starting with the yield on the supporting or reference assets with deductions for default and mismatch risk (to adjust for differences in the timing of asset and liability cash flows), or a 'bottom-up' approach starting with the risk-free reference rate plus an illiquidity premium. A top-down approach is likely to be applied for 'spread-based' insurance contracts, notably annuities in payment.

In IFRS Phase II, it is proposed that the impact of all changes in the discount rate over time are to be presented in OCI rather than through profit or loss. There is no equivalent concept in Solvency II. The approach will require the contract liability to be measured based on both the current and 'locked-in' (at inception) rates. This will introduce additional data and system requirements and will result in an accounting mismatch in the income statement for those contracts with supporting assets measured at fair value through profit or loss. However, where contacts are backed by debt securities measured at fair value through OCI the presentation of the discount rate will reduce accounting mismatch in the income statement.

"There remains considerable uncertainty over the discount rate in Solvency II. Differences in approach between Solvency II and IFRS, including the requirement for current and locked-in rates in IFRS, introduce a number of operational challenges."

Figure 6 illustrates the different approach in Solvency II compared to IFRS and raises a number of questions, including whether a wider application of the matching adjustment would be equivalent to a top-down approach in IFRS. The answers won't be known until Solvency II is finalised. Conceptually, there are similarities between the matching adjustment and the top-down approach. However, to include the counter-cyclical premium (triggered by a regulator's assessment of market events) in IFRS would appear challenging given the requirement to reflect the characteristics of the liabilities, which are typically independent of market events.

In addition, there is the possibility that a transitional arrangement on the discount rate may exist in Solvency II. For example, use of Solvency I rules may be allowed or phased out gradually over a period of time for existing contracts on implementation of Solvency II. This could result in liabilities with the same characteristics having different discount rates in Solvency II, which would be challenging to justify in IFRS.

Where there are differences between the discount rate in Solvency II and IFRS, including the requirement for two rates in IFRS, this will introduce a number of operational challenges, including dual assumption and valuation processes, potentially different asset data requirements, multiple economic scenario calibrations and additional reconciliations.

For short duration insurance contracts, the issue of discounting is less significant for the pre-claims liability. However, it is important to be aware of the implications for the liability for incurred claims (postclaims) particularly long tailed claims liabilities, notably, periodic payment orders and latent claims (such as asbestosis).

Allowance for risk

The concept of an explicit adjustment for risk is fundamental to both Solvency II and IFRS Phase II. In Solvency II, the allowance for risk is determined following a 'cost of capital' approach with a prescribed calibration, for example, a 6% assumed cost. In IFRS Phase II there is no prescribed method and the calibration must conform to a principle: 'the compensation the insurer requires for bearing the uncertainty inherent in the cash flows that arise as the insurer fulfils the contract'. If you are governed by Solvency II, it is likely that you will want to make use of the models you have developed for this purpose and are therefore likely to adopt a cost of capital approach under IFRS. However, there is the potential in IFRS to have a different cost of capital calibration from that used in Solvency II. For example differences could exist in respect of the assumed cost rate, the level of diversification benefit and the treatment of tax losses in the capital assessment. There are also practical considerations, including whether the Solvency II models can be adapted, model run times and how any differences will be reconciled and communicated to stakeholders.

As the results from the Solvency II Fifth Quantitative Study (QIS 5) highlighted, the risk margin in Solvency II is expected to be a relatively small percentage of the technical provisions (see Figure 7), so any differences in the calibration for IFRS Phase II may not be that significant.

At inception of a contract, a difference in the calibration of the allowance for risk between IFRS and Solvency II does not impact IFRS profit or loss as it is offset by the calculation of the residual margin (to the extent that there is a gain at inception). However, the difference will impact the future recognition of profit due to the different patterns of releasing the risk adjustment and residual margin to profit or loss.

Residual margin

As the residual margin is a concept with no direct comparison in Solvency II and many current GAAPs, you will need to develop a new model or separate system to determine this element of the liability and its release to profit or loss during the lifetime of the contracts.

The residual margin is determined at a 'portfolio level'. The release of the residual margin is to the period in which the service is provided and there is no prescribed level (unit of account). It is unclear how this will be interpreted in practice by insurers.

In addition, the margin is increased for interest at each reporting period at the locked-in rate (as considered in the discount rate section). Changes in estimates of future cash flows are not recorded in profit or loss, but are offset in the residual margin ('unlocking'), subject to the residual margin not becoming negative. You will still need to monitor a negative residual margin as changes in the estimates of future cash flows could result in the residual margin becoming positive in future periods and presented as a liability on the balance sheet. Changes in the valuation of options and guarantees, discount rate and risk adjustment are not offset by the residual margin. The requirement to unlock the residual margin and charge interest introduces greater complexity and more granular data requirements.

Key questions to be considered in developing a residual margin model:

1. What is the definition of your portfolios and do your existing cash flow models provide the required information at this level?

2. How will you release the residual margin to profit or loss, including both pattern and unit of account?

3. Can you identify in your models the impact from changes in estimates of future cash flows to unlock the residual margin?

4. What are the system options for modelling the residual margin?

5. A reconciliation of the residual margin between each reporting period has to be disclosed. How will you prepare this analysis?

6. Once established, the residual margin will be a significant component of profit in each period. How will you explain and analyse this internally?

The answers to these questions (among others) will help to determine the model requirements for managing the residual margin process following transition.

"Full retrospective application will be challenging under IFRS as the residual margin on transition will require an assessment of contract profitability at outset and then reassessed to the current date, a period of over 20 years on some contracts."

Participating contracts

The basic definition of a participating feature is similar in Solvency II and IFRS Phase II. All participating contracts issued by an insurer are expected to be in the scope of IFRS Phase II. In both frameworks, certain cash flows arising from the participating feature are included in the same way as any other contractual cash flows, that is, on an expected present value basis with a risk adjustment.

In IFRS, the cash flows relating to the policyholder's participation are measured and presented mirroring the underlying assets in which the policyholder participates, so at cost or fair value (through OCI or profit or loss); while options and guarantees are measured at their current value. There is no equivalent concept of mirroring in Solvency II as all assets are at economic (fair) value.

In IFRS, all expected payments to current or future policyholders are treated as a liability, even when at the insurer's discretion. In Solvency II, there is no directly equivalent concept, however, no liability is required for 'surplus funds' where this has been authorised under national law. The implications of these approaches will depend on the specific nature of the participating contracts and the approved national law.

The treatment of participating contracts in IFRS Phase II, including the practical application, remains an area of uncertainty as the IASB continues its deliberations. In comparison to many current GAAPs, it is expected that IFRS Phase II may introduce greater investment volatility in IFRS earnings.

Transition

Both Solvency II and IFRS Phase II require retrospective application on transition. This represents a significant change for IFRS compared to the exposure draft in 2010, where it was assumed that no residual margin would be allowed on existing contracts, effectively writing off this future profit to equity on adoption of the new standard. In Solvency II transitional provisions (such as potentially for the discount rate discussed earlier) may remove in certain respects the requirement for a retrospective application.

As Solvency II is a full prospective measure there is limited additional complexity from retrospective application. However, it will be challenging under IFRS, as the residual margin on transition will require an assessment of contract profitability at outset which is then reassessed to the current date, a period of over 20 years on some contracts. The importance of this assessment cannot be understated given the significant impact the margin will have on IFRS earnings following implementation.

For IFRS Phase II, transition is effectively on a 'best endeavours' basis, as estimation methods will be permitted to determine the residual margin on transition when there is insufficient objective data for certain years. Examples of estimate methods could include adjusting embedded value new business margins for differences to IFRS or adapting other legacy reporting metrics. There is added data complexity from the unlocking of the residual margin and the requirement for a discount rate at inception. Gathering data in the right format and at the right level of granularity is likely to be a substantial exercise, which should not be underestimated. An assessment on a product by product basis will help tailor the approach to those products where the most significant profit margins have existed. For some products, the margin may be clearly zero (or negative) due to age or adverse demographic assumption changes in the past. Whichever approach is adopted, it will need to be robust and capable of being audited.

Insurers are expected to adopt a similar approach to disclosing the impact of transition as was adopted for the

implementation of IFRS 4 in 2005.

The residual margin on transition has the potential to create some surprising results, which will need to be explained, particularly for products written back in past decades when the market conditions and underwriting practices were different from those of today.

External reporting: presentation and disclosure

Disclosures

The IFRS Phase II package of disclosures is largely known, and includes a number of additional requirements beyond those currently required for IFRS 4. Insurers may find the requirements onerous, such as detailed opening to closing balance sheet reconciliations and the confidence level disclosures for the risk adjustment. Solvency II also creates a significant number of private and public reporting and disclosure requirements. In both frameworks, the required level of detail is expected to be more onerous than current accounting and regulatory requirements. In Solvency II, there is also increased frequency of reporting.

Given the status of the disclosure packages, it should be possible to carry out an initial comparison of the requirements and judge what could be brought together. For example, could the Solvency II analysis of change in technical provisions and claims development tables be used for equivalent IFRS disclosures? Automating the production will reduce reporting time frames and save on related costs. In addition, with separate accounting and regulatory reporting requirements, it will be important to explain and reconcile the two balance sheets.

Presentation of the income statement

IFRS Phase II will prescribe the approach to income statement presentation. In a change from the original exposure draft, it will include premium, claim and expense information ('volume measures') on the face of the income statement. An 'earned premium' method is to be followed, where premiums are allocated to each period in proportion to the relative value of the insurance coverage and other services expected to be provided in that period. In addition, the measurement of premiums, claims and benefits presented in the income statement excludes receipts and payments from certain investment components within contracts (typically expected to be many policyholder account balances). These changes represent substantial difference to many current GAAPs for insurers who write long-duration business, and so will impact significantly data and system requirements. How the volume measures are explained to stakeholders will need to be considered.

There are no equivalent concepts in Solvency II due to its focus on the balance sheet strength rather than performance reporting.

Assets and other liabilities

The valuation of assets and other liabilities under Solvency II is, where possible, intended to be consistent with IFRS as endorsed by the European Union. It is therefore likely that there will be significant overlap between the two approaches, although there will be some measurement differences where IFRS is not considered to provide a suitable valuation for regulatory purposes.

Financial assets and financial liabilities

Under IAS 39 and its replacement IFRS 9, financial assets are valued either at amortised cost or at fair value (either in OCI or through profit or loss). Where valued at amortised cost, insurers will need to convert them to fair value for Solvency II. Under IFRS, financial liabilities are valued at either fair value or amortised cost. Solvency II requires that financial liabilities should be valued in conformity with IFRS upon initial recognition however subsequent adjustments are made for changes in the risk-free rate. This deviates from a fair value valuation because changes arising from changes in the insurer's own credit standing are excluded from the Solvency II valuation.

Participations (subsidiaries, associates, joint ventures and special purpose vehicles)

Under IFRS in solo financial statements, investments in participations are valued at either cost or fair value. This may differ for Solvency II, where listed participations are valued using quoted market prices, unlisted subsidiaries on an 'adjusted equity method' (being the share of net assets valued in accordance with Solvency II valuation principles or, when Solvency II valuation is not practicable, valued based on IFRS excluding intangibles and goodwill) and other undertakings (not subsidiaries) on an adjusted equity method (with an option to mark to model if an adjusted equity valuation is not possible).

Property plant and equipment (PPE)

Solvency II proposes that PPE (excluding investment property) should be at fair value where these items are not otherwise measured at economic value. The revaluation model in IFRS is considered as a reasonable proxy for fair value. However IFRS also allows a more commonly used alternative method of valuing PPE at cost less depreciation. The shift to economic valuation in Solvency II is likely to be a change for most.

Goodwill and intangibles

Under IFRS goodwill is recognised as a specific asset when an acquisition takes place and there is a positive difference between the purchase consideration paid and the fair value of the net assets acquired. Solvency II proposes that no value be ascribed to acquired goodwill.

Under IFRS intangible assets that qualify for recognition are measured under either a cost model or, where there is an active market for the asset, a revaluation model. Solvency II proposes that intangible assets are assigned a value only when they can be sold separately and a valuation can be derived from a quoted market price in an active market for the same or similar intangible. In practice most intangible assets of insurers are not traded in active markets and so no value will be assigned under Solvency II.

Leases

Under Solvency II, finance lease assets are measured at fair value. This differs from the present value of the minimum lease payment under IAS 17, which is considered inconsistent with Solvency II valuation principles.

Contingent liabilities

Under Solvency II material contingent liabilities are recognised as liabilities in the balance sheet and they are valued based on the discounted expected present value of the cash flows needed to settle the liability. Under IFRS, contingent liabilities are disclosed but not recognised on the balance sheet (except when arising upon an acquisition).

Employee and termination benefits

Following the recent amendment to IAS 19, the treatment of employee and termination benefits under Solvency II and IFRS are closely aligned. Under QIS 5 it was possible for insurers to apply their own internal model to the valuation of employee benefits. Under most recent technical specifications from EIOPA published in October 2012, this approach is not mentioned. It is not clear whether this means the use of an internal model for the valuation of defined benefit pension obligations will no longer be permitted under the Solvency II regime.

Group reporting

Both Solvency II and IFRS require reporting at group as well as at the entity level. For Solvency II, group reporting allows the insurer to make an assessment of its group capital position, and under IFRS consolidated accounts are prepared to present a single picture of the results of the group. Reflecting these different purposes, the scope, level and method of consolidation differs between IFRS and Solvency II, and the results prepared for each purpose may therefore be significantly different.

Level at which group reporting applies

IFRS requires group reporting at the level of the top company (the ultimate parent company) of the group, regardless of the activities of the entities within the group. In addition consolidation may be required at a sub-group level either by IFRS (for example, where an intermediate parent has listed debt) or by requirements of national law.

Under Solvency II group reporting is only applicable at the level of an insurance group which could be a subset of a larger group also conducting significant noninsurance activities. The level at which Solvency II group supervision applies depends on the location of the ultimate insurance parent and whether its regulatory regime is deemed equivalent to Solvency II:

- Where the ultimate insurance parent of the group is within the European Economic Area (EEA), Solvency II group reporting will be at this level.

- Where the ultimate insurance parent is outside the EEA, the group is subject to Solvency II group supervision at the ultimate EEA insurance parent level (that is at the sub-group level) and the requirement for any additional supervision will depend on whether the regulatory regime of the ultimate parent entity is deemed equivalent to Solvency II. If the regulatory regime of the ultimate parent is deemed to be non-equivalent it is possible that the ultimate group parent will also be subject to Solvency II group supervision.

The level of Solvency II group reporting may therefore differ from IFRS either because Solvency II reporting is required at an EEA level where IFRS reporting may not be; or because the insurance group subject to Solvency II group reporting is a sub-group of a larger group subject to IFRS group reporting.

Scope of consolidation

Another potential source of differences between Solvency II and IFRS group reporting lies in the definition of the group and as a result, which entities will be part of a group. Under IFRS a group is comprised of subsidiaries, joint ventures and associates. Under Solvency II the group is defined as the parent, its subsidiaries and participations. The definition of the entities comprising the Solvency II group is based on definitions contained in EU Accounting Directives; although these definitions are broadly consistent with IFRS, there are some differences that could potentially lead to a different scope of consolidation. In addition, supervisors are able to include other entities in the scope of Solvency II group supervision where they conclude that dominant or significant influence is exercised.

Method of consolidation

IFRS requires a single approach to consolidation, which involves combining all the results of the parent and its subsidiaries in the group on an individual line item basis, then applying consolidation adjustments, for example to eliminate inconsistencies in accounting policies and intra-group transactions. Associated undertakings are accounted for using the equity method of accounting.

Solvency II has two methods by which the group results may be prepared. The default approach under Solvency II is the 'accounting consolidation-based method', using the consolidated accounts as a starting point. Although it is called the accounting consolidation method, in reality the mechanism of consolidation depends on the type of entities being consolidated. For example, insurance subsidiaries are consolidated on a full line by line basis; other financial institutions within the group are incorporated on the basis of the proportional share of their own funds; and non financial sector unlisted subsidiaries will be incorporated on an adjusted equity method. As a result, although there may be opportunities for synergies where a group prepares IFRS consolidated accounts at the same level as the Solvency II group calculation, it is clear that the Solvency II consolidation mechanism is quite different to IFRS. Alternatively under Solvency II, the 'deduction and aggregation' method may be used at the discretion of the group supervisor, which calculates group solvency based on the aggregation of the individual entities in the group on a Solvency II or equivalent basis.

To view the original article, please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.