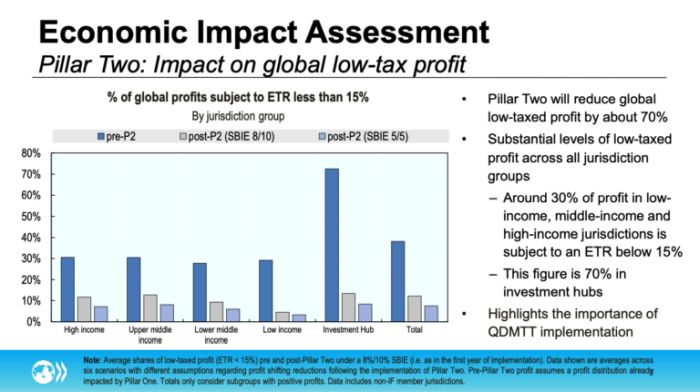

In a new economic impact assessment, the OECD expects that the global minimum corporation tax will significantly reduce corporate profits that are taxed at an effective tax rate of less than 15% by more than two-thirds.

David Bradbury, deputy director at the OECD's Centre for Tax Policy, said a new impact assessment of the so-called Pillar 2 rules showed that low-taxed profits would decline by 70%.

Speaking during the OECD Tax Talks on Monday, Bradbury said the full analysis would be published before the end of the year.

The OECD official noted that "substantial levels" of low-taxed profits can be observed across all jurisdiction groups.

Although the volume of such profits was higher in investment hubs, about 30% of profits in all other jurisdictions, regardless of whether they are high-, medium- or low-income, were taxed at a rate of less than 15%.

Even when considering the substance-based income exclusion, such low-taxed profits would be effectively reduced, he said.

"All of this is to highlight the simple fact that all jurisdictions we observe, have substantial pockets of low tax profit and that means that the global minimum tax is of critical importance to all jurisdictions, including developing countries, even countries that have higher statutory tax rates," Bradbury said.

The analysis, he said, highlighted the importance of putting in place a domestic minimum top up tax (QDMTT), to "ensure not only that the source jurisdiction is able to collect that additional tax that is going to be collected somewhere, but that it will be able to do that in a way that does not have any adverse impact on its competitiveness when it comes to attracting foreign direct investment".

Previous economic impact assessments by the OECD are likely to overestimate tax revenue gains from the global minimum tax.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.