Background

The regulatory regime governing foreign direct investment (FDI) in single brand retail trading (SBRT) sector is encapsulated in the Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations, 2000 read with the Consolidated FDI Policy, as amended from time to time by the Government of India (FDI Regulations). In terms of the FDI Regulations, FDI in SBRT is permitted up to 100% in the following manner:

- FDI up to 49% is permitted under the automatic route (i.e. such investment does not require the prior governmental approval); and

- FDI in excess of 49% falls under the approval route (i.e. such investment requires the prior approval of the government).

The proposals for FDI beyond 49% in the SBRT sector were processed and approved by the Department of Industrial Policy and Promotion (DIPP) and the Foreign Investment Promotion Board (FIPB). However, given the recent dissolution of FIPB by the Government of India on 24 May 2017, there has been an overhaul of the approval process for FDI proposals (falling under the approval route) across all sectors wherein FDI is permitted. Instead of FIPB acting as the nodal authority, such proposals will now be processed, scrutinised and approved by the concerned Department/ Ministry of the Government of India relevant to the particular sector in question (Competent Authority). In order to provide clarity on, and to streamline the mechanism related to the FDI approval process, the DIPP issued a standard operating procedure (SOP) on 29 June 2017. The SOP is meant to act as a guidance note for applicants and the officials of the Competent Authority and, amongst other things, sets out the procedure to be followed while (i) seeking the FDI approval; and (ii) processing the FDI applications, under the approval route.

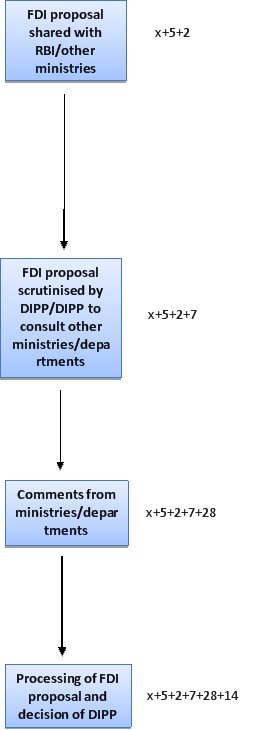

While the overhauled procedure and timelines for the processing of FDI proposals by DIPP is detailed in the SOP, a snapshot of such procedure and the underlying timelines is as follows:

|

STEPS TIMELINE

|

|

The FDI proposal is required to

be electronically filed on the existing Foreign Investment

Facilitation Portal along with the documents which are mentioned in

Annexure-1 of the SOP. If the electronic application is digitally

signed, then the applicant is not required to file a physical copy

of the application with the DIPP.

The FDI proposal is required to

be electronically filed on the existing Foreign Investment

Facilitation Portal along with the documents which are mentioned in

Annexure-1 of the SOP. If the electronic application is digitally

signed, then the applicant is not required to file a physical copy

of the application with the DIPP. Once the FDI proposal has been filed

with DIPP in the manner as set above, DIPP will share a copy of the

proposal with Reserve Bank of India (RBI) within 2 days in order to

seek its comments from the standpoint of Foreign Exchange

Management Act, 1999. All proposals are also required to be sent to

the Ministry of External Affairs and Department of Revenue for

information for their information and comments.

Once the FDI proposal has been filed

with DIPP in the manner as set above, DIPP will share a copy of the

proposal with Reserve Bank of India (RBI) within 2 days in order to

seek its comments from the standpoint of Foreign Exchange

Management Act, 1999. All proposals are also required to be sent to

the Ministry of External Affairs and Department of Revenue for

information for their information and comments.As is evident from the aforementioned new process, the total timeframe envisaged for the approval/rejection of the FDI proposal is now 8 - 10 weeks from the date of filing of the online application. However, any time expended in making corrections to the proposals or supplying additional information to DIPP by the applicants will extend the foregoing timelines accordingly. At the same time, where a physical copy of the application is also required to be filed, then the foregoing time limit is determined from the date of filing of the physical application.

The new regime is a welcome change as it now transparently sets out the approval process explicitly, which up until now was opaque. Further, the new timeline of 8 to 10 weeks (which has been significantly reduced from the erstwhile typical period of 5 to 6 months), even though not binding, provides a sense of clarity and certainty to the investors, which in our view reinforces the Government's commitment to attract more FDI in India and at the same time improves the ease of doing business in India. Nevertheless, in practice it remains to be seen how effectively this regime will function, and if the new timeline is adhered to by DIPP (more particularly in cases where security clearance is required from Ministry of Home Affairs).

The content of this document do not necessarily reflect the views/position of Khaitan & Co but remain solely those of the author(s). For any further queries or follow up please contact Khaitan & Co at legalalerts@khaitanco.com