Facts of the case:

Refer below a balance sheet for XYZ Limited, based on the balance sheet and additional information provided provide a working for outcome to different class of creditors.

Additional information:

Secured Creditors:

- Term loan is secured against fixed charge on land & building and fixtures & fittings. Bank A with INR 1,000 million term loan outstanding has first charge on the assets and Bank B with INR 400 million outstanding has second charge on the assets.

- Working capital loan is provided by Bank B and secured against a floating charge on stock, debtors and other current assets of the Company.

Other Liabilities:

- Workmen dues include amount payable for up to last 15 Months

- Employee liability include provision for bonus payable of Rs.50 million, which was discretionary based on performance of the company and not yet announced to the employees. Also, INR 25 million is outstanding for employees for more than 12 months

- Last three years of tax assessment pending and total demand raised by the department is INR 1,200 million. This has not been included in the balance sheet. However, liquidator has manged to get an assessment completion certificate and agreed a final liability of Rs.400 million.

Fixed assets and other assets:

- Land & building realised 65% of book value and there would be a cost of INR.100 million in realising the assets.

- Fixtures and fitting would realise 25% of book value, net of any realisation cost. Stock, debtors and other current assets would realise 60% of book value.

Other information:

- There was a pending insurance claim filled by the Company for a quality breach by a supplier, which was not recorded in the books. Liquidator has manged to recover INR 150 million from the insurance company. Lease for the office premises had a lock in period of 10 years, out of which three years have expired. Landlord has submitted a claim of Rs.120 million for the remaining seven years of the lease period.

- Based on amount realised and distributed cost of liquidation is computed to be Rs.175 million.

- Pending insolvency period cost was Rs.75 million mainly including interim funding, remuneration of the IP, unpaid cost for running the company during the period etc.

- The secured creditors have decided to relinquish their security interest to the liquidation estate and receive proceeds from the sale of assets by the liquidator in the manner specified in Section 53.

Response:

Table 1: Total value realized by liquidator

Note 1:

- Rs.100 million of cost for realising fixed assets has been deducted from the amount realised. Alternatively, it could also be included in the liquidation cost.

- In case the value realised is less than the insolvency and liquidation cost amount realised would be distributed between the all the cost pari passu.

Note 2:

- Claim recovered from insurance company of Rs.150 million has added to total value realised. It could be argued to use this realisation against unsecured creditors, since this is not realised from a secured assets.

Note 3:

- Workmen dues and secured creditors have pari passu claim on the amount available after liquidation and Insolvency cost.

- Bank A has a first charge on the secured fixed assets, in case of a situation where amount realised from secured fixed assets was less than the total outstanding of term loan of Rs.1,400 million, Bank A with first charge should be given preference over the Bank B. To the extent Bank B was not paid under sec 53 (1) (b) (ii), they should be paid under section 53 (1) (d).

- In case of working capital loan, Bank B has charge over the floating assets i.e Stock, debtor and other current assets of the Company. In the current situation, floating assets realised Rs. 965 million. Shortfall of Rs.35 million is set off against the excess realisation from the secured fixed assets. However, it could be argued to treat the shortfall as unsecured financial creditor under section 53 (1) (d).

Note4:

- Employee liability for more than 12 months has been included under section 53 (1) (f) as other debts.

- Bonus of Rs.50 million is not included in the employee liability as it is not declared and hence not due to the employees.

Note 5:

- Rent claim for unexpired lease period has been included under section 53 (1) (f) as other debts at nil value. As based on draft regulation 36, payment of periodic nature can only be claimed till the time order for liquidation is passed under section 33 of the IBC. This may, however be subject to further clarification by appropriate authorities.

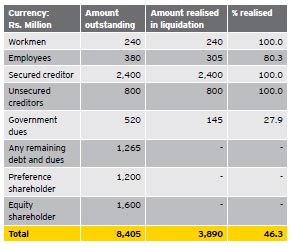

Table 3: Outcome to different class of creditors

To view the article in full click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.