Some of the key recommendations of the Council vide the 48th GST Council Meeting held virtually on 17 November 2022, are as follows:

- Certain offences under the GST law viz. obstruction or preventing any officer in discharge of his duties; deliberate tempering of material evidence; failure to supply the information, are proposed to be decriminalized. Further, the minimum threshold for initiating prosecution is recommended to be increased from INR 1 crore to INR 2 crores (except for fake invoice cases). The legislative changes are expected to be introduced in the Union Budget 2023-24. The move is aimed at reducing disputes and chances of taxpayer harassment.

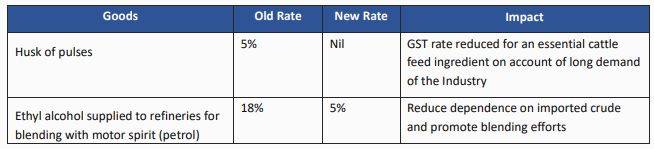

- The GST rates largely remain unchanged. In only two cases, the GST rates have been proposed to be reduced:

- In order to resolve ambiguity, the GST Council shall also clarify on a few key industry issues:

-

- Incentives paid by Central Government for promotion of RuPay Debit Cards and low value BHIM UPI transactions are not taxable. This clarification will bring relief to the banking industry.

- 22% Compensation Cess is applicable to SUVs [engine capacity > 1500 cc; length > 4000 mm and ground clearance >= 170 mm]. This is applicable to motor vehicles fulfilling all four conditions.

- No Claim Bonus offered by the insurance companies to the insured is an admissible deduction for valuation of insurance services.

- Pursuant to the Delhi High Court judgment in the case of Seema Gupta Vs Union of India [2022 142 taxmann.com 564 (Del)], it has been clarified that no GST is payable where the residential dwelling is rented to a registered person in his/her personal capacity for use as his/her own residence and on his own account and not on account of his business.

- Goods falling in lower rate category of 5% under schedule I of Notification No. 1/2017-CTR imported for petroleum operations will attract lower rate of 5% and the rate of 12% shall be applicable only if the general rate is more than 12%. The clarification appears to be limited to goods imported for petroleum operation. The other issue being faced by the oil & gas industry viz. taxability of support services, provided for the petroleum operations, remains unaddressed.

- With effect from 1 Feb 2019, certain activities such as supplies of goods from a place outside the taxable territory to another place outside the taxable territory, high sea sales and supply of warehoused goods before their home clearance, were excluded from GST (neither qualifying as supply of goods nor services). Doubts were raised regarding retrospective application of these amendments. It has now been clarified that no GST would be payable even for the intervening period from 1 July 2017 to 1 Feb 2019 (intervening period). However, no refund would be granted where tax has been paid in respect of such transactions for the intervening period.

- GST Rules would be amended retrospectively (from 1 Oct 2022) to clarify that ITC reversal would be required proportionate to the amount not paid to the supplier vis a vis the value of the supply, including tax payable. Full reversal of ITC may not be required in cases where partial payment has been made towards the inward invoice. In this context, a mechanism shall also be prescribed for re-availment of credit, if the supplier pays tax subsequently.

- Certain amendments/clarifications are expected in context of

the following :

- Place of supply of services of transportation of goods to a place outside India. It has also been recommended that proviso to sub-section (8) of section 12 of the IGST Act, 2017 may be omitted.

- Treatment of statutory dues in respect of the taxpayers under Insolvency and Bankruptcy Code, 2016.

- Verification of ITC in case of mismatch between FORM GSTR-3B and FORM GSTR-2A during FY 2017-18 and 2018-19.

- Applicability of E-invoicing.

- Amendment in definition of "non-taxable online recipient" and "Online Information and Database Access or Retrieval Services (OIDAR)" would be introduced so as to reduce interpretation issues and litigation on taxation of OIDAR Services.

- Other measures for streamlining compliances in GST have been proposed particularly to tackle the menace of fake and fraudulent registrations.

ELP comments

It is not in doubt that the above-mentioned clarification would offer certainty on the disputed tax positions. Further, despite being an important item in the Agenda, no decision has been taken on a few important issues such as setting up of GST Tribunal, taxability of online gaming and mechanism to curb tax evasion in pan masala and gutkha business. It is hoped that the next Council Meeting would be held shortly and decision on these critical issues are taken at the earliest.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.