Reduced VAT on short-term yacht charters starting in Malta

On 29 July 2013, the VAT Department published guidelines in relation to the Malta VAT treatment of short-term yacht charters starting in Malta. These guidelines follow to a large extent the interpretation currently being applied to long-term yacht leases. Our latest VAT Insight aims to provide an overview of the functioning, conditions and implications of this interpretation.

Guidelines

In terms of the guidelines, a short-term charter of a yacht is an agreement whereby the yacht owner / operator contracts the use of the yacht, for a consideration, with a crew or on a bare boat basis for not more than 90 days. In the absence of the new interpretation, where such yacht is put at the disposal of the customer in Malta and will be used for leisure purposes, 18% Malta VAT would have been due on the charter fees charged. As a result of the VAT Department's interpretation, however, the Malta VAT chargeable on the charter is limited to that portion of the use of the yacht within the territorial waters of the EU.

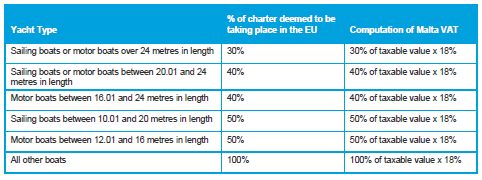

For the purposes thereof, the guidelines set out to establish the estimated percentage VAT taxable portion of the charter fees based on the time that the yacht is made use of within the territorial waters of the EU. The percentages are set according to the length of the yacht and its means of propulsion (power or sailing). 18% VAT is then applied only on the established percentage of the charter deemed to be related to the use of the yacht within EU territorial waters. The table below indicates the applicable established percentage portions:

Conditions

Prior to applying the above VAT treatment, the owner / operator of the yacht must seek approval in writing from the Malta VAT Department. The latter may grant such approval provided the following conditions are satisfied:

- The supplier of the yacht is a person registered for VAT in Malta;

- The yacht charter contract indicates the place where the charter commences (i.e. Malta), the charter price and a statement that the yacht shall sail outside EU waters;

- Upon application, the supplier of the charter produces sufficient documentation to identify the yacht with regards to hull number, port of registry, registration number, and any further documentation confirming the size and type of yacht.

The VAT Department may request proof of any payment in connection with the charter.

Recovery of input tax

The guidelines confirm that the owner / operator may reclaim input tax incurred on the fuelling and provisioning of the yacht, in so far as such costs are recharged to the client at the standard VAT rate. If, on the other hand, the owner / operator pays fuelling, provisioning and similar costs on behalf of the client and merely recharges such costs at no mark up (as is typically the case where the client pays an Advance Provisioning Allowance before the charter starts), no input tax may be claimed by the owner / operator and no VAT would be chargeable on the relative claim for reimbursement of such expenses.

The supplier of the charter would, subject to the normal provisions of the law, be entitled to claim input tax incurred on fuel purchased for the outward journey of the yacht to its next port of destination after completion of the charter.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.