Telcos seeking to go "beyond connectivity" isn't new. Over the last 10 to 15 years, telcos have made a push into ICT, lifestyle services, utility / insurance resell, fintech, marketplaces and even healthcare. The motivation for such diversification was always clear - to find new growth sources as the connectivity business becomes increasingly commoditized and to monetize the B2C and B2B relationships. A number of telcos globally had made it a centerpiece of their strategy but have had mixed results over the years. Even while some of the telcos have been successful at revenue diversification, translating that into margins and sustained shareholder returns has been difficult.

The recently evolving vision of telcos seeking to become techcos

seems fundamentally no different from the endeavors in the past,

except it has an added objective of seeking better valuations. Tech

companies currently have 5 - 15x market cap to revenue multiples

versus the telcos at 0.5x - 1.5x. While the "why" for

such a shift is clear, the "what" and "how"

seems missing in the current narrative. Tech is a highly

competitive sector (given the number of startups, pace of

innovation and VC investments) and, therefore, there is a need to

drive clarity on the telco's proposition in the sector and on

their right to play. Further, tech companies are set up and operate

very differently from telcos. Therefore, discussion is also

required on how telcos can change their DNA sufficiently and

quickly.

What is holding the telcos back?

We had conversations with telco leaders across geographic markets testing our hypothesis on the key challenges the telcos are facing to go "beyond connectivity". A few common themes emerged:

- Making the tough choices on the

"what": Telcos are hard pressed to find silver

bullets or highly profitable whitespaces in the tech sector.

Currently, telcos have a healthy EBITDA margin on connectivity

services as they seek to monetize heavy capex investments into

profits. New technology services, on the other hand, will have

lower EBITDA margins, which is due to the nature of the products

themselves and also the requirement for highly skilled workforce

across the value chain.

- Funding the transformation: Telcos are cash

constrained as the topline is flat or just recovering to

pre-pandemic levels. On the other hand, the new fiber deployments

and 5G capex have been onerous. Markets have been unforgiving too.

Telco global stocks have fallen over 15% in the last five years.

Current dividends (both Verizon and AT&T's dividends were

about 7.8% at the time of writing this article) are already

difficult to meet. Telco stocks are largely owned by pension funds,

state sovereign funds, and retail investors who seek consistent

dividend income. In such a situation, convincing the Boards and the

shareholders on channeling the dividends to fund a new

diversification push will face strong resistance.

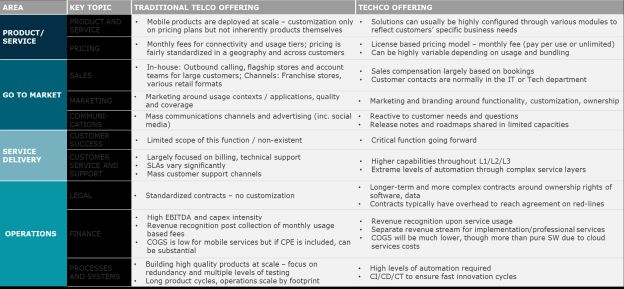

- Figuring the path to the tech operating model

: Telco operating model is fundamentally different from

that of a techco. Telcos are setup for massive infrastructure

deployment, field intensive operations and to deliver highly

reliable services. On the other hand, tech services require high

level of opex, advanced skills, extreme agility / innovation and

copious risk-taking and iterative builds. Here are a few ways how

both the operating models are different.

- Other priorities: Telcos are in the midst of more urgent and already delayed initiatives. Complexity reduction, asset divestments, driving convergence, 5G monetization etc., are still on the anvil. The organizational bandwidth to drive a large "techco" transformation is fragmented or simply, is not present.

What needs to be different this time around?

The telco to techco journey is risky, complex, and painstaking but not entirely impossible. Besides addressing the above roadblocks, we see four elements that telcos will need in their transformation recipe to improve the odds - prioritization, product centricity, partnerships, and persistence.

Prioritization: A massive shift of this magnitude requires ruthless prioritization and value orientation - from crafting the vision to day to day execution. Tech companies prioritize significantly and go to market initially with one product. Only after they taste success and sense other market gaps or unaddressed customer pain points, they expand to other product lines. Therefore, keeping the starting point of the journey simple and practical is essential. Secondly, it is important to ask what legacy business / operations the telco needs to give up as it gets into the new tech business. Finally, adopting a Private Equity lens to value orientation throughout the transformation helps efficient scoping and use of resources.

Product centricity: Software development and tech product launch is a critical different skill than network builds and operations. Telcos will need to create a separate product-centric and high performance organization that is staffed with very different capabilities - teams working in an agile manner, focused on high velocity and iterative product releases, and able to gravitate towards a niche that the company can successfully fill and differentiate from competition.

Partnerships: Partnerships are widespread in the tech industry for a good reason. They offset R&D costs and facilitate access to skillsets / markets and accelerate the time to cash. As per Harvard Business Review, 94% of tech sector executives consider partnerships as imperative. Telcos will face a number of "make vs buy" decisions as they manifest on the techco journey. In the past, they have been challenged to effectively make the trade-offs and to take a cross-ecosystem perspective in building partnerships.

Persistence: A techco transformation is a multi-year commitment from all stakeholders including the telco's Board. Becoming aware of the magnitude of change and committing to the transformation is only the initial step. Being persistent and executing on a set of micro transformations provides for a better chance of success than a burst of large-scale enthusiasm.

A lean and efficient connectivity service operations is a must-achieve and an early milestone in the telco's ambitious journey on "beyond connectivity". Not only are the savings from efficiency programs needed to fund the growth aspiration, but a leaner organization is also easier to navigate in what can be choppy waters here. Telcos may not have time on their side to revisit the age-old "beyond connectivity" question in yet another new framing in the future. It is time now to decide and execute!

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.