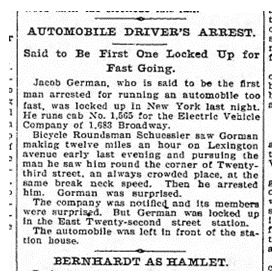

It is May 20, 1899. New York City taxicab driver Jacob German is the recipient of the United States' first-ever speeding ticket. He whizzed by at 12 miles per hour on Lexington Avenue and was then pursued and remanded by a patrol officer on a bicycle. Perhaps more surprising though, is that Mr. German was driving an electric vehicle – the same model that made up the majority of the NYC taxi fleet in the late 1800s until Henry Ford's Model T was introduced to the masses in 1908.

The introduction of the Model T, better roads, and cheap petroleum effectively ended the heyday experienced by the first electric vehicles in the early 1900s and electric vehicle production was largely quiet until the early 1990s when the EV1 and the Prius "bolted" onto the scene. More recently, governmental investment, legislative requirements, and technological advances have led to the largest deployment of electric vehicles in history.

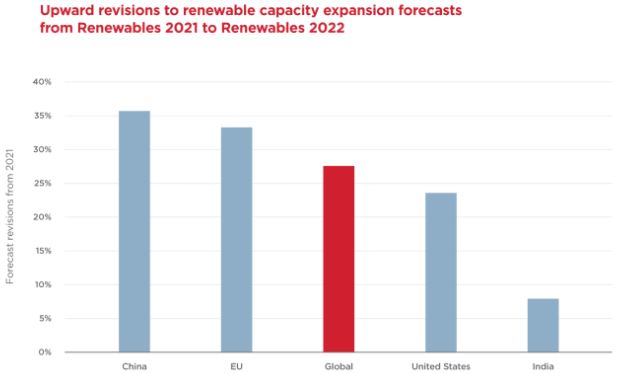

Driven by conflict, subsidization, innovation, and a desire to reduce global carbon emissions, renewable energy's growth and integration into the global power generation paradigm has also accelerated at the fastest pace in history. According to the IEA, this has translated into significant upward revisions in renewable capacity, globally, from 2021 to 2022, as indicated below:

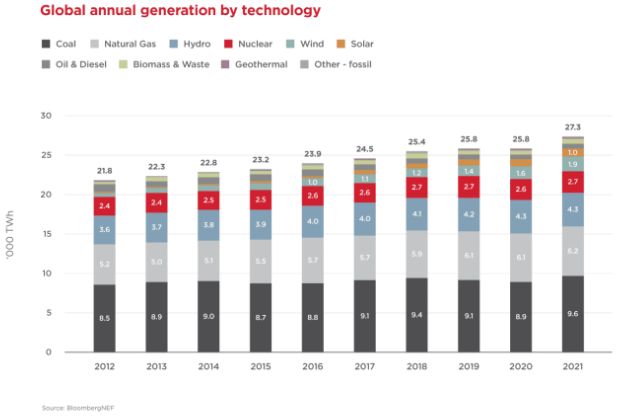

Much of this growth is occurring in the wind and solar sectors, overtaking (combined) hydro in 2021. It is important to note though that developing nations are forecasted to account for half the total greenhouse gas emissions by 2030 and this will translate into oil & diesel being utilized globally at levels never seen before in history.

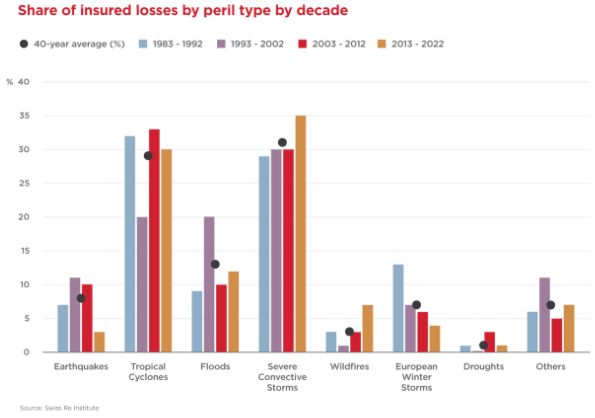

It seems much of the discussion pertaining to global large loss experience does not even contemplate renewables. Natural catastrophes continue to dominate the landscape of insurable losses. Since 2017, average annual insured losses from natural catastrophes have been greater than $110B, more than double the average of the prior five-year period.

Yet the shift to renewable energy is resulting in an evolving adjustment process in global insurance markets as new and evolving technologies can result in unexpected losses (as well as new players within the market). Renewable energy sources, by their nature, can also be bellwethers in the evaluation of global climate change as they are generally exposed to the elements and experience losses on the front lines of change. In the 2nd quarter of 2022, hailstorms caused losses in excess of $50M in the solar industry. According to Willis Towers Watson, renewable energy insurance claims exceeded $650M in 2022. These extreme weather patterns continue to impact solar farms today.

For all the reasons noted at the onset of this discussion, the future of power generation will include expansions of wind and solar as well as traditional hydrogen and geothermal sources. Artificial intelligence, more efficient solar cells, and larger wind turbines combined with increasing storage alternatives will allow renewable energy to be deployed at faster rates than at any other time in history. Growth in this sector has been staggering. In 2010, renewable energy accounted for approximately 3.8% (305 GW) of global power generation (a growth factor of 28 from 2000). Currently, renewable energy sources are projected to contribute approximately 3,371 GW of global energy production in 2023. Currently, this represents approximately 12% of global energy production. Renewable energy (wind & solar) is generally projected to increase to one-third by 2030 (as a percentage of the global power generative capacity).

From an insurer's perspective, evolving technologies create underwriting challenges as do evolving threats both natural and manmade. Though the IEA indicates that 90% of all power generation expansion will occur in renewables, many of the risks covered today will be the risks covered tomorrow, although on a larger scale. Carbon-based fuels will also remain a necessary component of the global power generation paradigm.

With regard to business interruption, extra expense, and the analysis of property damage-related costs, forensic accountants will continue to rely on much of the same data typically relied upon for the evaluation of claims in the industry today. However, weather forecasts, AI evaluations of demand, supply chain evaluations, and specific reinstatement experts will likely become an even larger component of our processes.

As technology advances and evolves so will our conversations within the paradigm of emerging renewable energy sources and related losses. With that, I leave one final thought, is it still called a gas pedal on an electric car?

- Brooklyn Daily Eagle/newspapers.com

- https://www.insurancebusinessmag.com/us/news/environmental/new-insurance-exposures-stemming-from-renewable-energy-initiatives-412671.aspx

- https://www.reuters.com/legal/legalindustry/renewable-energy-project-insurance-claims-renewed-attention-suit-limitations-2023-05-26/#:~:text=As%20the%20renewables%20industry%20has,incurred%20losses%20exceeded%20%24800%20million

- https://www.reuters.com/sustainability/climate-energy/wind-solar-produce-over-third-global-power-by-2030-report-2023-07-13/

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.